Today at 12:00 (GMT+2), the eurozone will release its November inflation data. Forecasts suggest that the core Harmonized Index of Consumer Prices will rise from 2.4% to 2.5%, while the broader indicator is expected to remain at 2.1%. However, analysts note that these figures are unlikely to pressure the euro meaningfully, as a rate cut by the European Central Bank (ECB) is not currently being discussed.

The most analysts expect is a single 25-basis-point reduction sometime in the first half of 2026. Investors are far more focused on the region’s economic outlook, which continues to hover near stagnation. Yesterday’s PMI data highlighted a decline in Germany’s manufacturing index from S&P Global and Hamburg Commercial Bank (HCOB), sliding from 48.4 to 48.2 in November. Spain’s figure fell from 52.1 to 51.5, while France registered 47.8. Across the eurozone as a whole, the index dipped from 49.7 to 49.6. In the US, comparable data was mixed: the ISM manufacturing index slipped from 48.7 to 48.2 (below expectations of 48.6), while S&P Global’s reading edged up from 51.9 to 52.2. Meanwhile, the US dollar remains under pressure as markets increasingly expect the Federal Reserve to ease monetary policy at its December 10 meeting.

GBP/USD

The British pound is losing ground against the US dollar, extending yesterday’s correction and testing the 1.3215 level on a downside breakout. Monday’s macroeconomic data from the UK was mixed: net consumer credit slowed from GBP 6.6 billion to GBP 5.4 billion in October (vs. forecast 6.4 billion), mortgage approvals slipped slightly from 65,647 to 65,018 (vs. forecast 64,400), while the S&P Global manufacturing PMI held at 50.2.

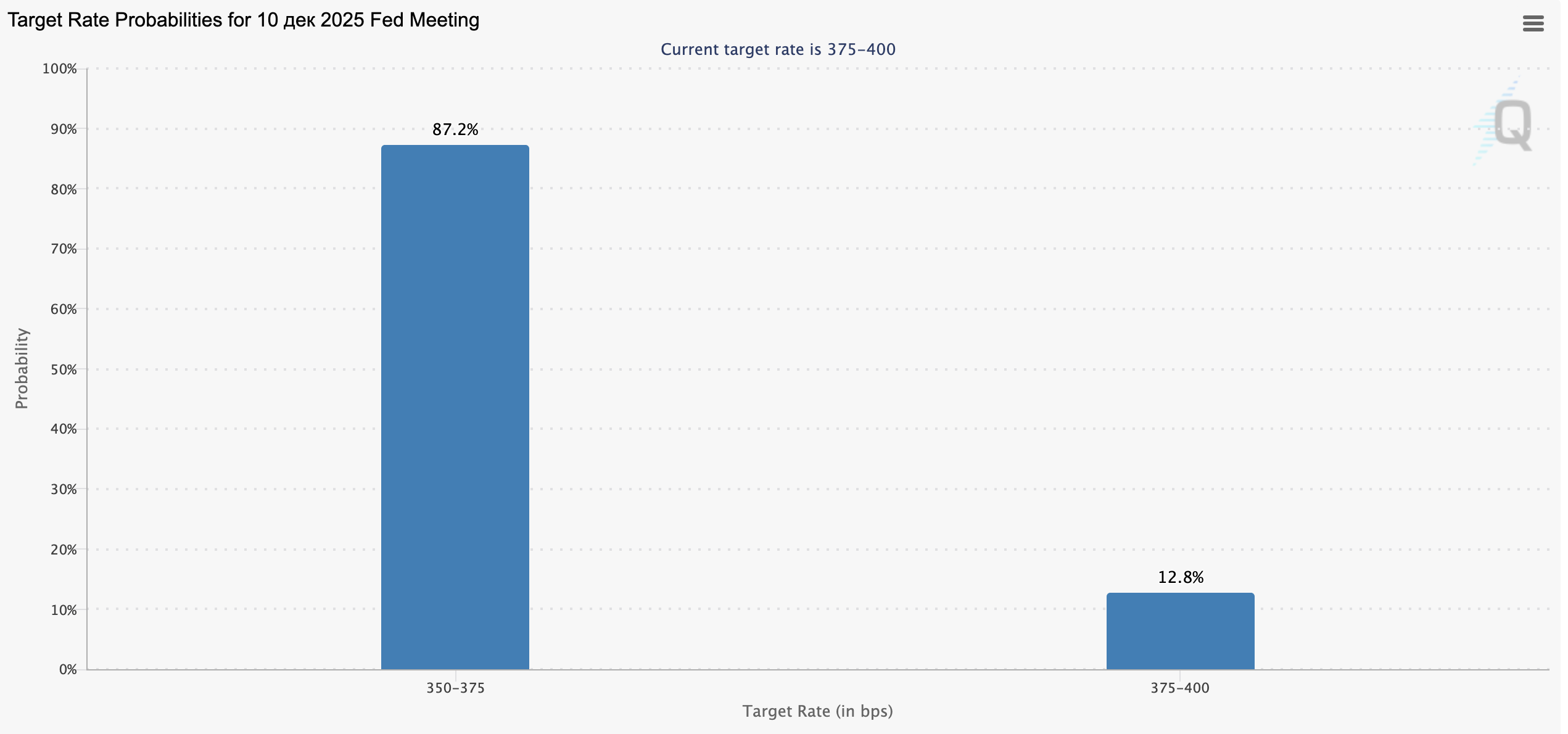

Meanwhile, traders continue to price in a high probability of a Fed rate cut in December: according to the CME Group’s FedWatch Tool, odds are approaching 90%. On Wednesday at 15:15 (GMT+2), markets will receive the ADP private employment report, with expectations of a 10,000 increase for November following a 42,000 gain previously. On Friday at 17:00 (GMT+2), the US will release Personal Consumption Expenditure (PCE) price index data — a key inflation gauge used by the Federal Reserve. The core PCE is projected to remain at 2.9% year-over-year, while the broader measure may accelerate slightly from 2.7% to 2.8%. Stronger readings would support a more cautious Fed stance.

AUD/USD

The Australian dollar is strengthening against the US dollar, holding near 0.6550 and extending a strong short-term bullish impulse. The US dollar remains under pressure as markets anticipate a Fed rate cut on December 10. The CME FedWatch Tool currently assigns roughly a 90% probability to a 25-basis-point reduction to 3.75%. Nonetheless, Fed Chair Jerome Powell may again remind investors that future cuts are not guaranteed given limited available data.

The October US labor market report was never released due to the record-long government shutdown, and the November data will arrive only after the December meeting. Meanwhile, the Reserve Bank of Australia (RBA) continues to avoid easing policy due to persistent inflation risks. Yesterday, the Melbourne Institute’s inflation reading supported the Australian dollar: annual inflation accelerated from 3.1% to 3.2%, while the monthly figure held at 0.3%. Pressure on the AUD came from China’s manufacturing PMI by Caixin and S&P Global, which fell from 50.6 to 49.9 in November. Today’s focus is on Australian building permits: October approvals fell sharply from 11.1% to –6.4% (vs. –4.5% expected), while the annual figure dropped from 14.9% to –1.8%.

USD/JPY

The US dollar is edging higher against the Japanese yen, testing 155.65 on an upside breakout as the pair attempts to recover from yesterday’s decline toward November 17 lows. Persistent expectations of a Fed rate cut continue to weigh on the USD, while the Bank of Japan has not ruled out potential policy tightening. On Monday, BOJ Governor Kazuo Ueda said he would review all arguments for and against a rate hike at the next meeting, with a particular focus on incoming inflation and labor-market data.

Late last week, markets assessed Tokyo’s November inflation data: the broad CPI eased from 2.8% to 2.7%, while the core index held at 2.8%. Retail sales in October rose sharply by 1.7% following a 0.2% increase previously (vs. 0.8% expected), supporting the yen. Today, USD/JPY is additionally buoyed by an improvement in Japan’s consumer confidence index, which climbed from 35.8 to 37.5 (vs. 35.9 expected). On the US side, investors await tomorrow’s ADP employment report and Friday’s PCE inflation release — both key inputs for assessing the Fed’s December decision.

XAU/USD

Gold is showing modest gains as XAU/USD extends its short-term and medium-term uptrend, refreshing the October 21 highs. The metal is supported by growing market expectations that the Federal Reserve will cut interest rates by 25 basis points to 3.75% in December.

Dovish comments from Fed officials — including Christopher Waller and New York Fed President John Williams — also support gold, as both signaled openness to policy easing if incoming data justifies it. Recently weak US macroeconomic data reinforces this narrative.

Last week’s retail sales rose only 0.2% in September (vs. 0.4% expected), while the November consumer confidence index fell sharply from 95.5 to 88.7. Yesterday’s manufacturing data was mixed: the ISM index slipped from 48.7 to 48.2 (below expectations), while S&P Global’s manufacturing PMI rose from 51.9 to 52.2.

On Friday at 17:00 (GMT+2), markets will receive the PCE inflation report for September — the Fed’s preferred inflation metric. Analysts expect no major change from the core monthly reading of 0.2% and the annual 2.9%. Meanwhile, the November labor report will not be released due to the recent shutdown, but investors will still receive ADP employment data and weekly jobless claims.