The global forex market is preparing for a pivotal year in 2025, with the EUR/USD currency pair positioned at the center of macroeconomic, political, and policy crosscurrents. The divergence between the United States and the eurozone has never been more pronounced—whether in growth, inflation, central bank priorities, or political risk. Traders, corporates, and global investors alike are recalibrating their expectations as the euro appears increasingly vulnerable to a move toward parity with the US dollar.

This outlook combines in-depth macroeconomic forecasts, central bank policy analysis, political event risk, and technical analysis to deliver a holistic EUR/USD forecast for 2025. We highlight why the fundamental and technical landscape favors further US dollar strength—and why the euro is likely to struggle amid slow growth, shifting inflation dynamics, and mounting geopolitical uncertainty.

1. The Macro Backdrop: Growth Divergence at the Forefront

Growth and inflation are returning as the dominant drivers of currency markets, superseding even central bank inflation targets as the top theme for 2025. The United States economy proved resilient in 2024, with GDP growth above 3% annualized in the third quarter and private consumption remaining strong. Unemployment trended near historic lows, wage growth kept pace with inflation, and corporate earnings delivered upside surprises—propelling US equity markets to record highs.

By contrast, the eurozone ended 2024 teetering on the edge of recession. The initial optimism around post-pandemic recovery faded fast: by Q3, GDP growth in the euro area slowed to just 0.9% YoY. Manufacturing PMI readings consistently printed below the 50-mark, signaling contraction, while even services—long the backbone of eurozone resilience—showed signs of stalling. Harmonized inflation rates (HICP) fell sharply from double-digit peaks, landing near 2% by year-end, but at the cost of flatlining demand and persistently weak consumption.

The upshot: US-EU growth divergence is now the dominant force shaping forex expectations. As we enter 2025, consensus among analysts is that the US economy will again outperform, with the Federal Reserve projecting 2.5% GDP growth (up from 2% in its prior forecast), while the European Central Bank’s own estimates point to eurozone growth of just 1.1%. This differential is the bedrock for dollar strength in all major forex forecasts for 2025.

US-EU GDP growth divergence as primary forex driver

US-EU GDP growth divergence as primary forex driver2. Central Bank Policy: The Fed vs ECB — A Study in Contrasts

Federal Reserve: Gradual Easing, Focus on Sticky Inflation

Following three interest rate cuts in late 2024, the Federal Reserve enters 2025 with the federal funds target range at 4.25%–4.50%. Fed policymakers continue to stress a “data-dependent” approach—projecting only two further cuts in 2025. While headline inflation receded from post-pandemic highs, core inflation remains stubbornly above target: the November 2024 CPI registered 2.7% YoY, and core CPI was at 3.3%.

Crucially, the Fed’s “dot plot” reveals caution. Officials are unwilling to accelerate easing in the face of robust domestic demand, strong labor markets, and the possibility of renewed inflation pressure should new trade tariffs materialize under President Trump’s administration. In the current environment, the US dollar enjoys continued support from relatively high real yields, deep capital markets, and the country’s ongoing status as the world’s premier safe-haven currency.

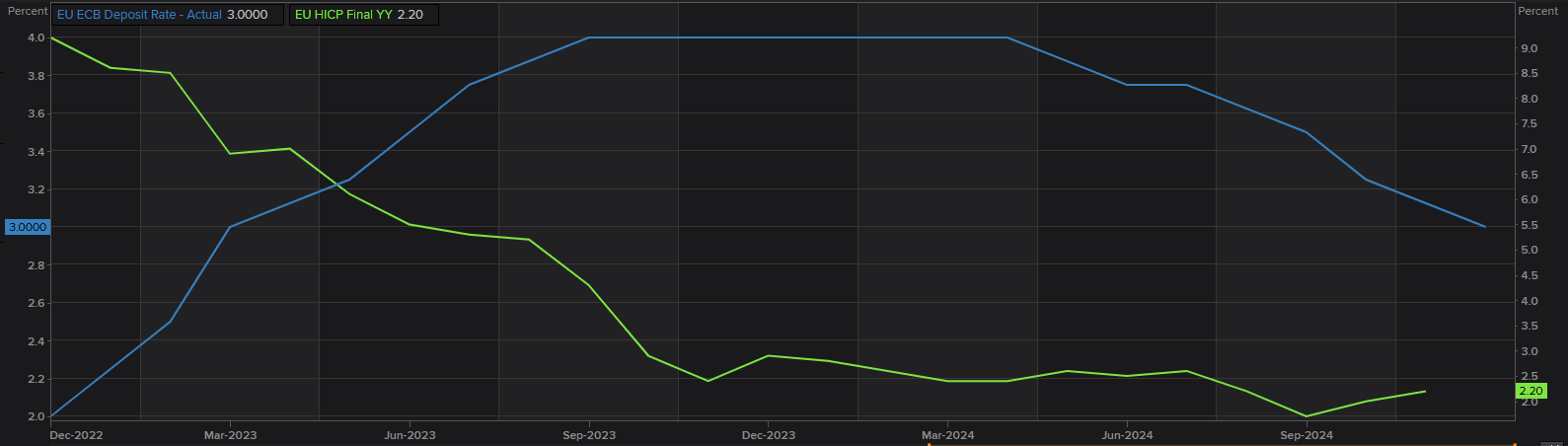

European Central Bank: Early Dovish Turn, Structural Headwinds

The ECB was the first major central bank to reverse course in 2024, announcing a series of rate cuts beginning in June and totaling 100 basis points by December. The main refinancing rate now stands at 3.15%, the marginal lending facility at 3.4%, and the deposit facility at 3%. These moves were not driven by inflation relief, but by mounting recession risk and severe political uncertainty—particularly in France and Germany.

Unlike the Fed, the ECB faces little margin for error. Deteriorating PMIs, sluggish consumption, and repeated government crises have left the eurozone highly exposed. ECB projections see inflation stabilizing near 2.1% in 2025, with GDP growth far below trend. For EUR/USD, this means the interest rate differential will likely widen in favor of the dollar—fueling capital outflows and further euro weakness.

ECB–Fed rate divergence to drive EUR/USD

ECB–Fed rate divergence to drive EUR/USD3. Political Risk and Policy Uncertainty: Trump’s Return Changes the Game

Nowhere is the impact of political risk more evident than in the US, where Donald Trump’s return to the White House and unified Republican control of Congress signal a shift in the economic and trade policy landscape. Traders are watching closely for new tariffs, stricter immigration controls, and the prospect of large-scale fiscal stimulus—a potent mix for markets already wary of “higher-for-longer” inflation.

In previous cycles, Republican victories were greeted with market optimism, as promises of deregulation, tax cuts, and business-friendly reforms fueled risk-on sentiment. However, the 2025 scenario is different. This time, the risks of a trade war, protectionism, and dollar appreciation are front and center. If the Trump administration imposes sweeping tariffs, not only would US consumer prices likely rise, but retaliatory moves from Europe and Asia could further squeeze global trade and growth.

Meanwhile, in the eurozone, political risk is rising. Both France and Germany are grappling with domestic crises, including government collapses, snap elections, and the rise of anti-EU populist parties. Investors fear that policy paralysis, combined with weak macro data, will further undermine the euro’s global standing.

US election and EU instability weigh on euro

US election and EU instability weigh on euro4. Technical Analysis: EUR/USD Bearish Momentum Strengthens

The technical picture for EUR/USD has deteriorated markedly since late 2024. The pair finished three straight months in the red, slipping below the critical 20-month moving average—a signal not seen since the early days of the pandemic. The 100-day SMA has acted as an impassable resistance zone, while the recent breach of 1.0330 leaves little in the way of support until the psychologically important parity level ($1.00).

Technical indicators: Momentum oscillators are solidly in bearish territory. The MACD is well below its signal line, RSI readings remain under 40, and weekly stochastic oscillators point toward further downside. The 20-week SMA is on the verge of crossing below the 100-week SMA—a classic confirmation of sustained bearish trend. If parity is broken, the next major support zone sits at 0.9850–0.9900.

Upside risks exist: Should US macro data unexpectedly weaken, or if the eurozone were to surprise on the upside (for example, through fiscal stimulus or a sharp rebound in global trade), EUR/USD could attempt a correction toward the 1.06–1.10 region. However, such a move would likely require a combination of US dollar underperformance and renewed investor confidence in the European project—neither of which are baseline assumptions for 2025.

5. Forward-Looking Scenarios and High-Impact Catalysts

- Fed surprises: Faster or deeper US rate cuts than currently projected could spark a USD correction, offering a window for EUR/USD recovery—especially if accompanied by softer inflation and improving labor market slack.

- ECB action: A “bazooka” move—such as coordinated fiscal stimulus, new asset purchase programs, or radical reforms—could support the euro, though political gridlock makes this a low-probability event.

- Geopolitics: A major risk-off shock (conflict escalation, supply chain disruption, or energy price surge) would likely boost the dollar, given its unrivaled liquidity and safe-haven appeal. Conversely, a breakthrough in global trade relations could buoy risk appetite and help the euro recover some ground.

- Trump administration policy: New US tariffs or fiscal expansion could both raise inflation and spark volatility, but are more likely to strengthen the dollar unless they trigger a market confidence crisis.

6. Conclusions: Baseline Outlook for EUR/USD in 2025

In summary, all major macro, policy, and technical indicators currently point to continued US dollar outperformance and a persistent bearish bias for the euro. The divergence between US and eurozone growth, compounded by opposing central bank trajectories and heightened political risk in both regions, sets the stage for a likely move toward parity in the EUR/USD exchange rate by mid-2025.

While upside surprises remain possible, the base case is for the EUR/USD pair to grind lower over the next several quarters, testing parity and potentially overshooting on sustained negative momentum. Investors and corporates with euro exposure should hedge accordingly, while traders should monitor high-frequency catalysts, including inflation prints, labor market data, and key policy meetings from both the Fed and the ECB.

As always, currency markets can turn on a dime in response to new information. But in the current environment, EUR/USD forecasts for 2025 remain tilted decisively in favor of further dollar gains and sustained pressure on the euro.