The crypto world is facing a perverse paradox. The technology works. The ecosystem is growing. Yet most tokens — the primary vehicle through which people invest in the industry — are systematically failing. A number of leading industry analysts now openly state that even Bitcoin, Ethereum, Solana, and XRP are uninvestable over the long term. What is behind this? We break down why most tokens are structurally built against their holders, what warning signs to watch for, and how to select assets with genuine potential.

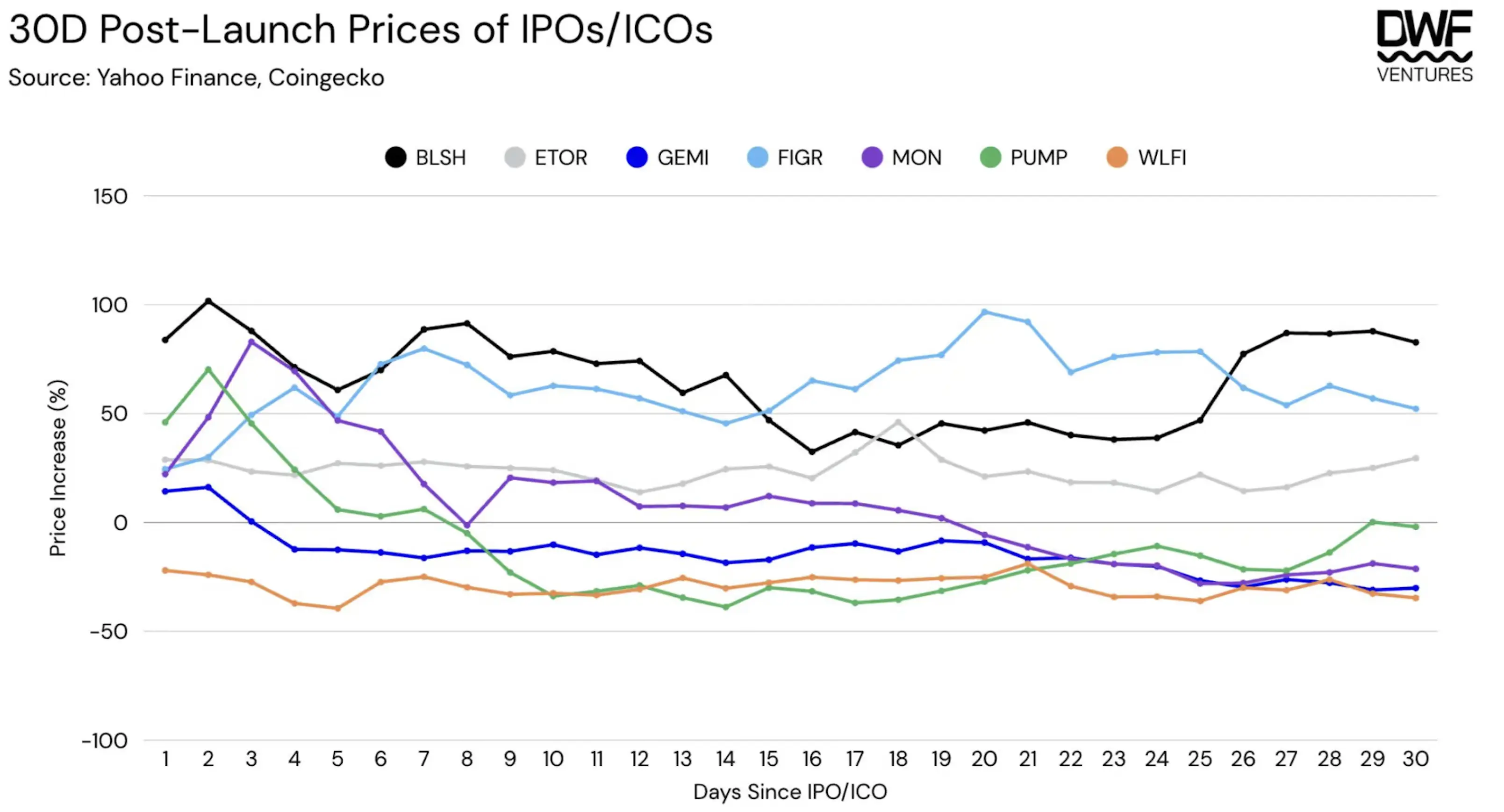

The Crypto Graveyard: Numbers That Hurt

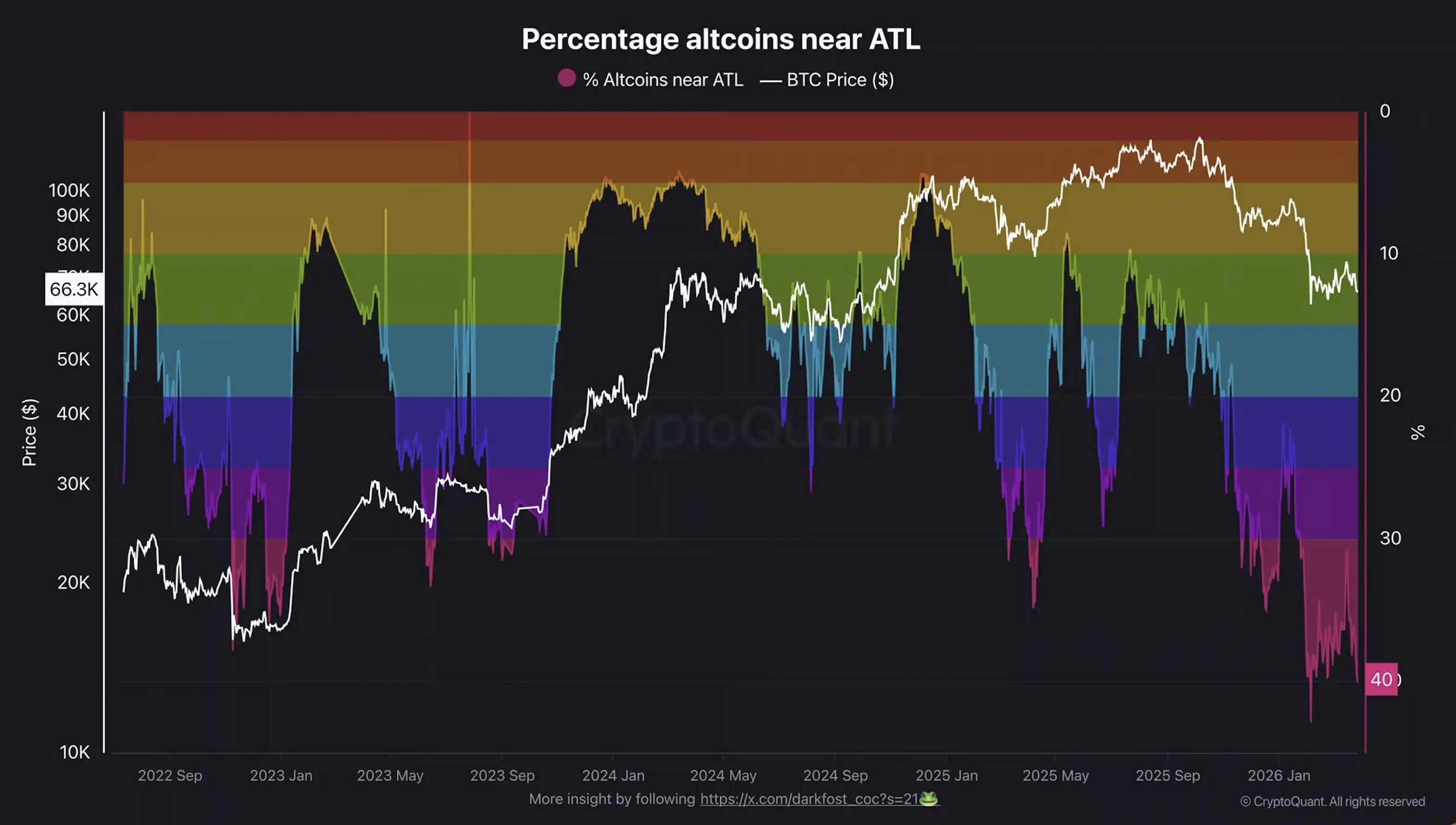

The hard truth for crypto investors: the easy-money era is over. 40% of all altcoins are trading near all-time lows. According to Blockworks, tokens — excluding Bitcoin, Ethereum, and stablecoins — have delivered a median return of minus 80% since 2021.

CoinGecko counted nearly 20 million cryptocurrencies at the end of 2025. More than half ceased to exist in 2025 alone — accounting for over 80% of all crypto "deaths" in a single calendar year.

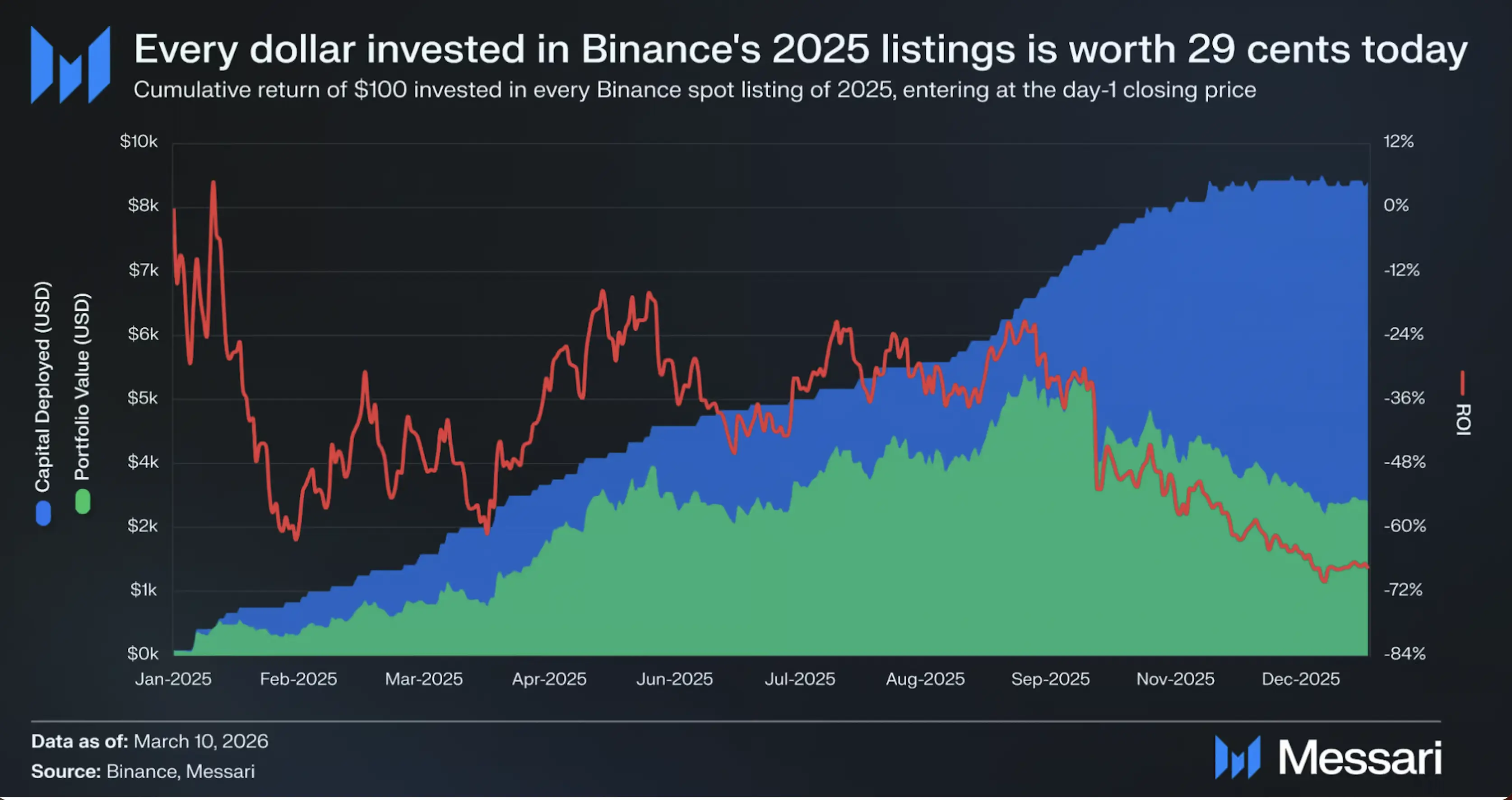

The biggest token launches of the year also disappointed. The seven largest ICOs of 2025 raised a combined $3 billion, launched with roughly $10 billion in market cap, and have lost an average of 51% since then. Five of the seven are down more than 80%.

The key point for crypto investors: this problem has become structural, not cyclical. What is happening runs deeper than an ordinary bear market.

Bitcoin and the Rest "Are the Problem"

Jeff Dorman, CEO of one of the most respected crypto investment firms, published a thesis that sparked widespread debate. In his view, the systemic weakness stems from a structural loss of trust — caused by the flawed framing of the four largest assets.

BTC, ETH, SOL, and XRP are "uninvestable": their investment theses have failed, and the assets are structurally incapable of capturing the economic value generated by real adoption. Dorman is effectively passing judgment on the industry's most beloved blue chips.

Bitcoin. Over 17 years, Bitcoin has discarded nearly every narrative it was built on, argues Dorman. Not digital gold, not an inflation hedge, not a payment system. 21 million coins sounds like hard scarcity — but through derivatives and ETFs, what trades today is largely just a shadow of the real asset.

Ethereum and Solana. Both are considered winners among Layer-1 blockchains, but Dorman is convinced this is largely an illusion. 99% of the world's assets are not yet on-chain — and even if both networks continue to grow, their tokens don't necessarily have to benefit.

XRP. Perhaps the clearest example of how far a token's design can drift from the interests of its holders. The token does nothing, has almost no real connection to Ripple Labs, and Ripple itself sells $3–4 billion worth of XRP every year to fund its own share buybacks.

Until the investment theses for these assets fundamentally change, they will likely continue to underperform other asset classes — with the exception of brief short-term spikes.

Three Mechanisms Working Against Crypto Investors

Surviving in this market requires understanding how bad tokens are structurally built against their holders. Three patterns repeat themselves consistently.

1. Dilution: the silent tax. The standard playbook: a project mints a fixed total supply subject to an unlock schedule for insiders, venture funds, and the team. The initial float is deliberately kept low to generate hype with minimal capital. As subsequent unlocks hit, the new supply systematically dilutes early investors. The numbers speak for themselves: projects with supply expansions above 200% lost up to 99% of their value according to Tokenomist. Tokens valued at 50x their raised capital at launch fell by more than 87% on average. The rule of thumb: avoid holding assets with large upcoming unlocks.

2. No fundamentals. Tokens without revenue, without user growth, and without economic value for holders are structurally doomed. There are millions of them, and they exist almost exclusively for speculation, granting no rights to cash flows. Strong narratives and aggressive marketing cannot replace this foundation — they only delay the inevitable collapse.

3. Buybacks as PR. Token buybacks are deliberately framed to resemble stock buybacks. EtherFi bought back 2% of its tokens while simultaneously issuing 64% in new supply. Net inflation: 62%. The buyback program was more of an image exercise than genuine value for holders. Everything comes down to the funding source: treasury-funded buybacks delivered an average of minus 33.8% over 90 days, while revenue-funded buybacks returned plus 73.6%. The difference is fundamental.

Good Tokens Exist — at Fair Valuations

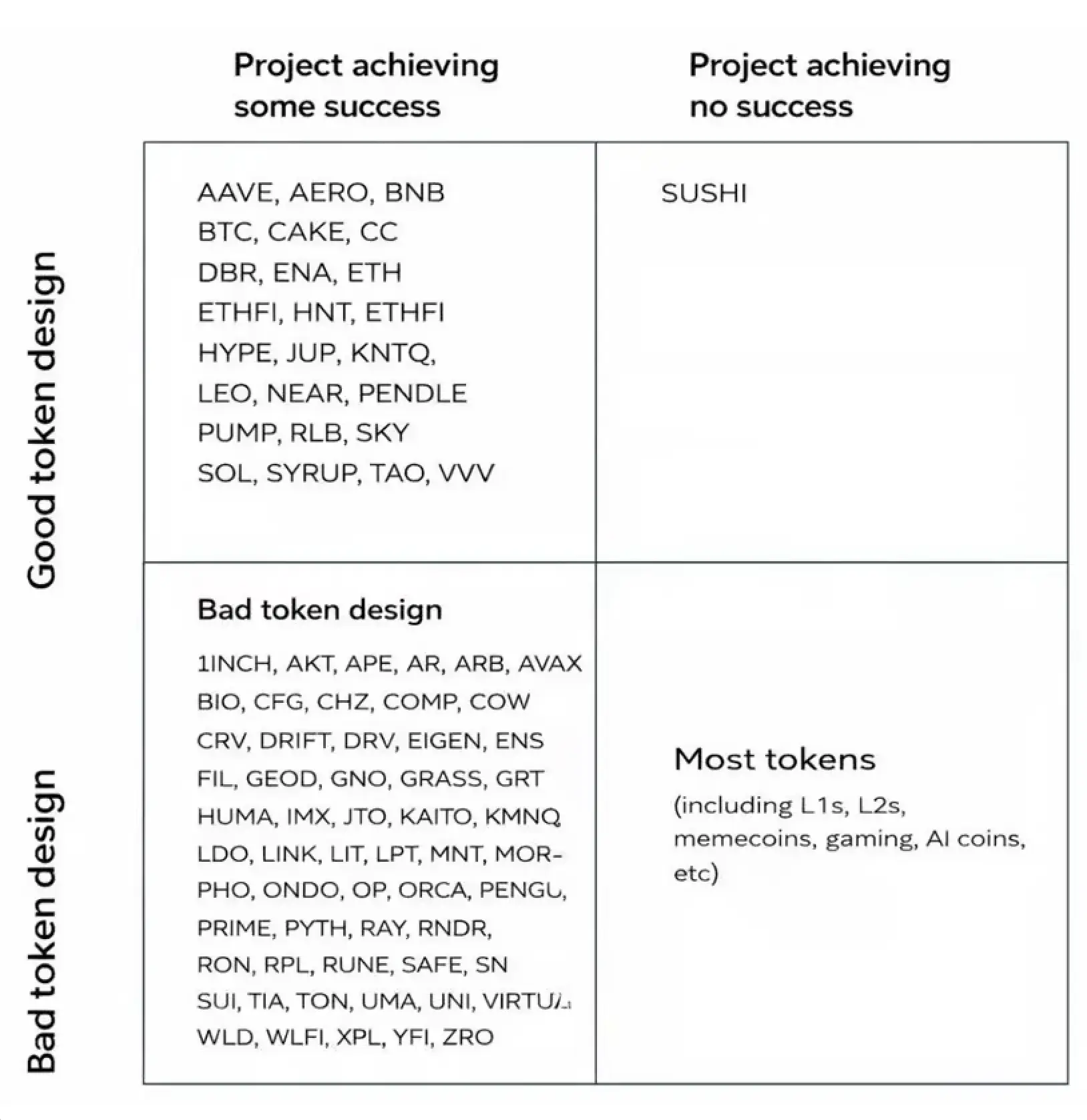

Dorman developed a four-quadrant matrix: successful projects with bad token design (the biggest trap), weak projects with weak tokens, strong projects with strong tokens, and everything in between. Following his logic, there are at most 10–20 tokens one can invest in today with a clear conscience.

Based on the mechanisms described above, every crypto investor should ask three questions.

1. What is the valuation and how much more supply is coming? FDV relative to capital raised. What unlocks are scheduled? On resources like Companies Market Cap, you can benchmark FDV against the market cap of real companies.

2. Where do buybacks and yields come from? Protocol revenue or token inflation? Those who don't know the source of the yield are often the yield themselves.

3. What value actually flows to the holder? Real governance rights? A share of revenue? Does the token provide genuine benefits within the ecosystem — or is it purely a speculative vehicle?

Convincing answers to these questions lead to tokens that combine the best of equities with the innovation of crypto. The market is only just beginning to notice them — and valuations are sometimes surprisingly fair.

Hyperliquid: 97% of protocol fees go toward HYPE buybacks. Total volume exceeds $650 million — roughly 46% of all crypto buybacks industry-wide. Net emission: minus 10%. Price-to-revenue ratio: 14x.

Aave: weekly buybacks of $1 million funded from real operating surplus, annualizing to $50 million. Stakers earn 8.3% annually from real lending revenue. Price-to-revenue ratio: 3x — cheaper than Coinbase (9x), Visa (15x), or CME Group (16x).

Toward "De-Tokenization"

This discussion has sparked a new debate in the industry. Behind most crypto protocols sits a company with clearly defined ownership rights — and economic value often flows primarily to equity holders, not token holders.

The uncomfortable truth may be this: for a good crypto investment, you sometimes don't need a token at all. Stripe's new Layer-1 blockchain Tempo operates without a native token — all revenue goes to Stripe. Coinbase's Layer-2 network Base also has no token; the better bet there is the Coinbase stock itself.

Analysis by DWF Ventures shows that ICOs and IPOs often launch at comparable valuations, but IPOs deliver more consistent returns over longer time horizons. In many cases, the "crypto stock" is simply the better altcoin.

The Across Protocol example makes this trend tangible. The project is converting its DAO into a C-Corporation and its ACX token into a traditional equity share. The market's reaction says it all: investors clearly prefer equity exposure over a governance token with no value capture. Observers are calling it the first step toward "de-tokenization."

Regulation as a Catalyst for Better Token Design

How did we get here? Two factors pulled the ecosystem in the wrong direction for years: toxic incentives to design tokens superficially around narratives — and a panicked fear of being classified as a security.

That is changing right now. The joint SEC and CFTC classification framework, published on March 17, 2026, creates legal clarity for the first time — making good token design not just permissible, but necessary.

Fidelity expects a fundamental market split. On one side: "rights-rich" tokens with legally enforceable claims on revenue and governance. On the other: "rights-light" — everything that lacks those rights. The direction of travel is clear.

This opens a door that was previously shut. According to Legion, only 2–5% of the purchasing power in the traditional asset market can currently invest in tokens. Sovereign wealth funds, pension funds, insurers, and endowments are all on the sidelines for regulatory reasons. That capital may now begin flowing into the first class.

Crypto Is Growing Up

Observers believe crypto's post-dot-com era has arrived. The industry's aggregate price-to-revenue ratio has fallen from 40,400x to 170x. Governance tokens without substance are dying out, and protocols valued below Visa that actually distribute revenue to holders are becoming the Amazon of this cycle.

Two trends will define the road ahead.

Singularity: projects will have to choose a clear model — either a classic startup without a token, exiting via IPO or M&A, or a decentralized platform with the token as the sole investment vehicle. The gray zone in between — companies using tokens as a financing tool without value capture — will be squeezed out under regulatory pressure.

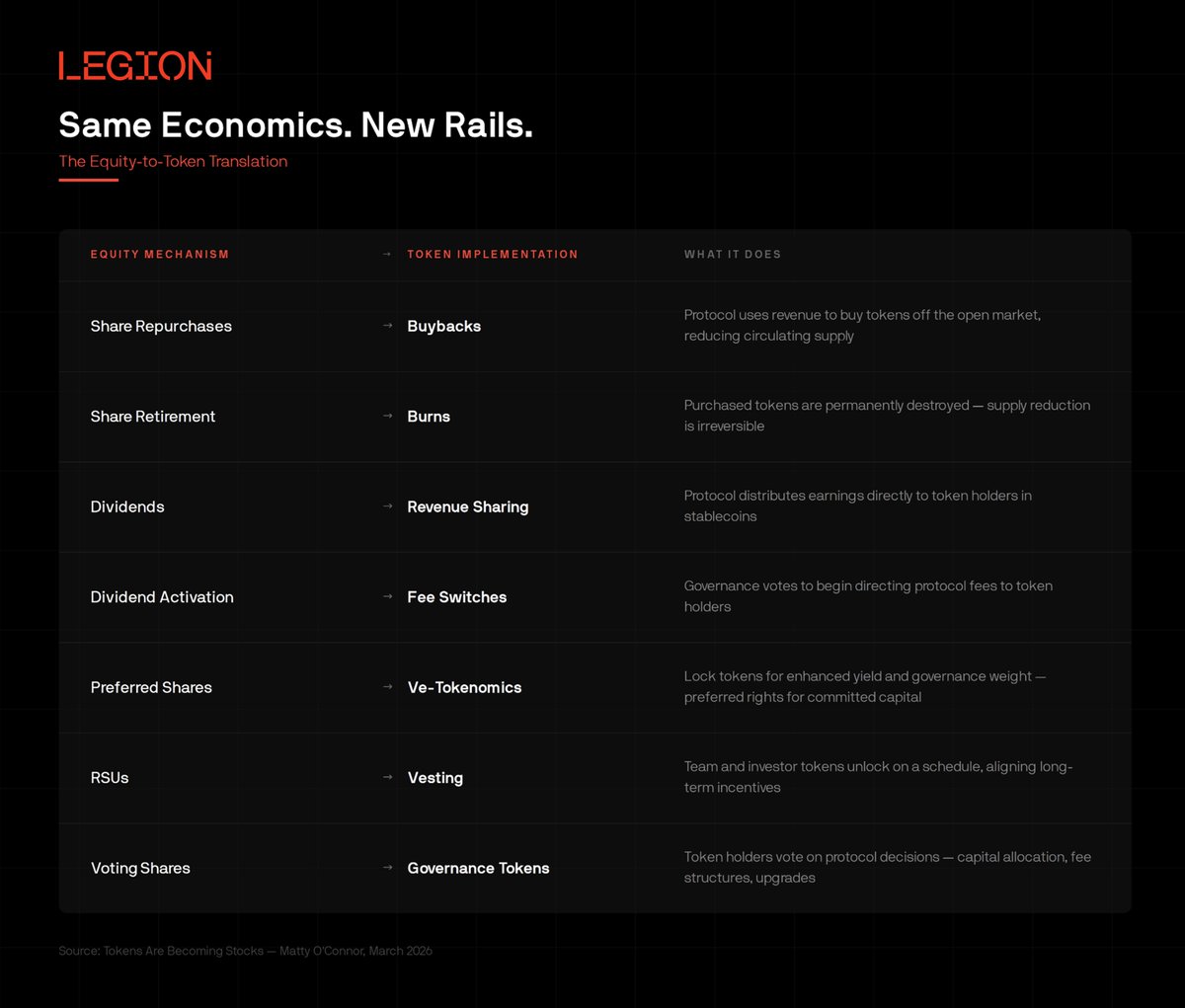

Convergence: classic equity mechanisms are moving on-chain. Backpack Exchange has introduced a staking-to-equity feature: stake the token for a year and convert it into a real ownership stake in the company. More such models will follow — stablecoin dividends, performance-linked vesting, tokenized participation rights. The difference between a stock and a token is becoming increasingly technical and decreasingly meaningful.

The crypto market is shedding its casino reputation and maturing into a fully-fledged asset class — with clear rules, real metrics, and justified valuations. Those who learn to distinguish tokens with genuine value from speculative noise will be at the forefront of the next cycle. But when will that cycle arrive — late 2026, or 2027–2028? That remains an open question.