Total inflows for H1 now approach $17 billion, trailing only slightly behind the $18.3 billion seen in the same period last year. The resilience of investor demand, even in the face of volatile macroeconomic and geopolitical backdrops, underscores a robust appetite for digital assets.

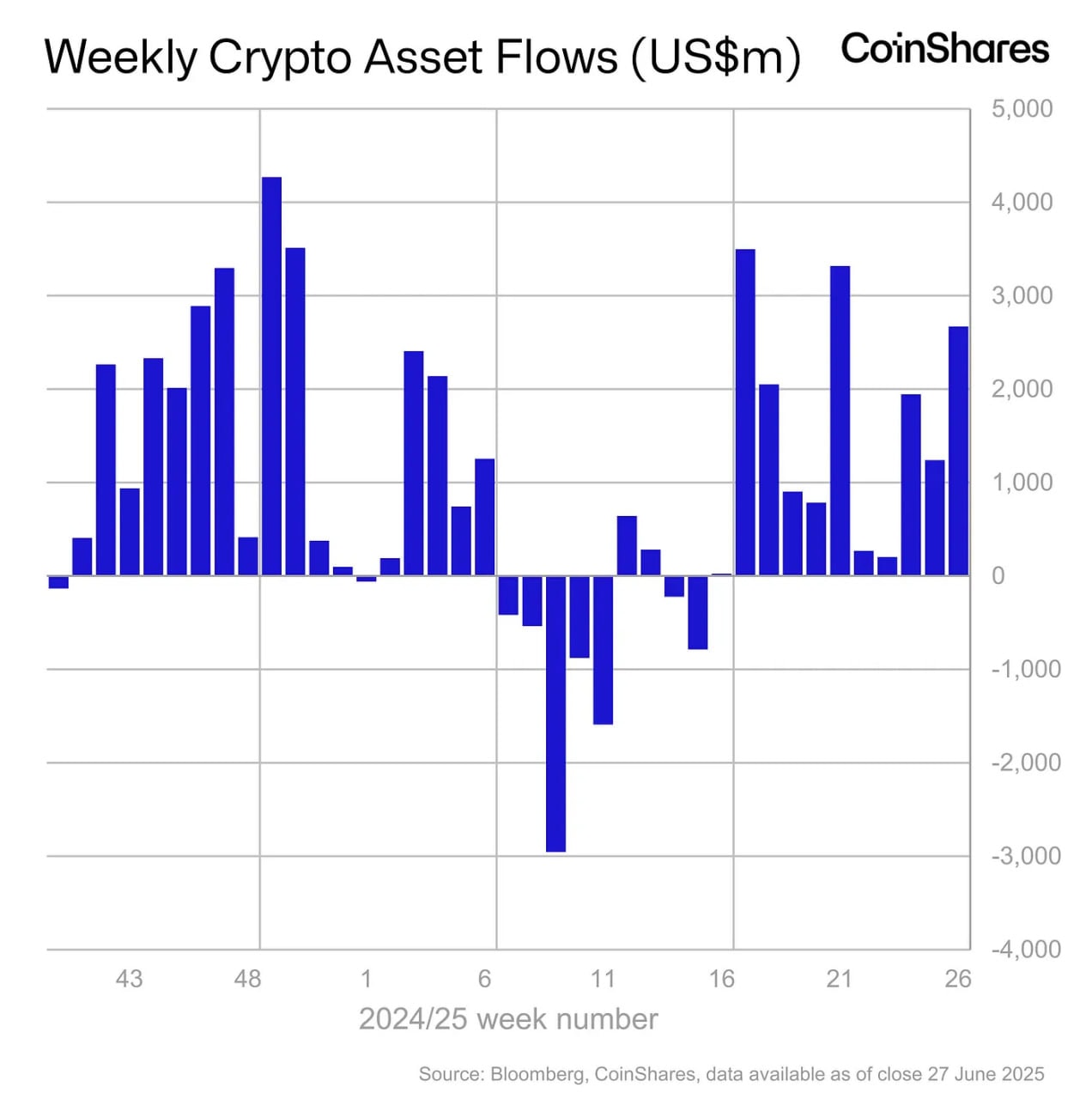

Weekly inflows to crypto funds by region and asset, according to CoinShares

Weekly inflows to crypto funds by region and asset, according to CoinSharesCoinShares attributes this sustained inflow streak to “a combination of escalating geopolitical tensions and growing uncertainty over the direction of global monetary policy.” The vast majority of new capital originated in the United States, which accounted for $2.65 billion—over 98% of total inflows. Switzerland ($23M) and Germany ($19.8M) also registered positive flows, while Hong Kong saw outflows of $132 million in June.

Bitcoin and Ethereum Dominate, Short Products See Outflows

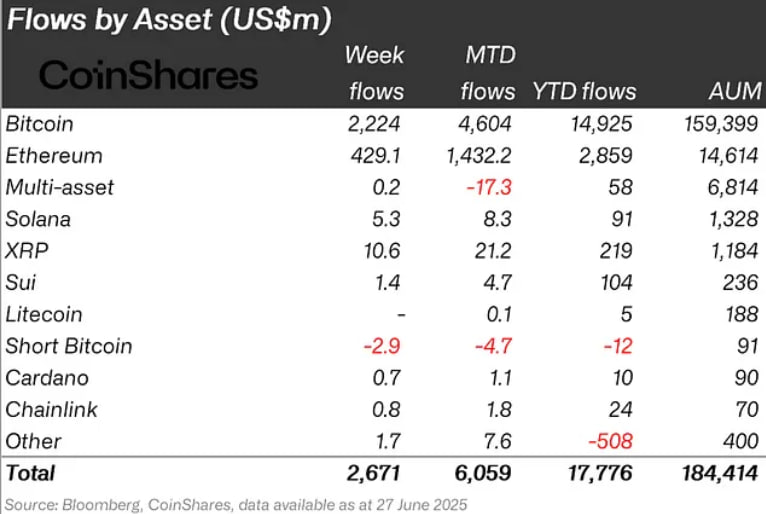

Bitcoin-focused funds remain the preferred choice for investors, capturing $2.2 billion in inflows last week—roughly 83% of the total. Meanwhile, investment products designed to profit from declining prices (short-Bitcoin funds) continued to see capital exit, registering $2.9 million in outflows for the week and $12 million year-to-date.

Ethereum funds attracted $429 million over the week, bringing annual inflows to $2.9 billion. By comparison, Solana-based products have accumulated only $91 million YTD, reflecting a significant gap in investor interest between large-cap and altcoin strategies.

Crypto fund inflows by asset class: Bitcoin, Ethereum, Solana (CoinShares)

Crypto fund inflows by asset class: Bitcoin, Ethereum, Solana (CoinShares)The robust performance comes as spot Bitcoin and Ethereum ETFs brought in more than $2.5 billion over the same period, signaling deepening institutional penetration into the digital asset space.

Market Outlook: Drivers and Implications

The persistence of positive inflows into digital asset investment products highlights the sector’s resilience amid global financial uncertainty. Investors are increasingly viewing cryptocurrencies—particularly Bitcoin and Ethereum—as both a hedge and a speculative vehicle during turbulent market cycles. The divergence in flows between leading digital assets and alternative coins such as Solana reflects a preference for established projects with greater liquidity and institutional infrastructure.

CoinShares expects that ongoing geopolitical developments and the path of central bank policy will continue to shape capital flows in the second half of 2025, with US-based funds likely to dominate market share.