Decentralized Finance (DeFi) has fundamentally disrupted the global financial system, offering borderless, censorship-resistant alternatives to traditional banking and fintech.

Built on public blockchains like Ethereum, DeFi enables users to access a range of financial services—from lending and asset management to insurance and derivatives—without intermediaries, paperwork, or centralized oversight. In this in-depth guide, we’ll explore what makes DeFi unique, how it compares to fintech, its primary applications, leading protocols, and the operational and systemic risks that come with decentralization.

DeFi: Reshaping global finance with blockchain. Source: The Block

DeFi: Reshaping global finance with blockchain. Source: The BlockHow DeFi Works: Smart Contracts and Permissionless Access

At the core of DeFi are smart contracts—self-executing programs that automate agreements, enforce terms, and move assets transparently. Unlike legacy finance, where banks, brokers, or clearinghouses process transactions, DeFi relies on open-source protocols that are accessible to anyone, anywhere. As a result, users can lend, borrow, trade, or insure assets with nothing more than a wallet and an internet connection. There are no account managers, credit checks, or centralized points of control; trust is established mathematically and transparently.

The evolution of DeFi marks a paradigm shift: the infrastructure for complex financial operations is now programmable, interoperable, and open 24/7. Platforms built on Ethereum, Binance Smart Chain, Solana, and other L1s have fueled explosive growth, with total value locked (TVL) in DeFi protocols surpassing $900M and counting.

DeFi vs. Fintech: Beyond Digital Banking

While both DeFi and fintech leverage the internet to modernize finance, they embody fundamentally different philosophies and architectures. Fintech projects like Block (formerly Square) digitize existing financial workflows, but remain subject to licensing, regulatory oversight, and centralized risk controls. Fintech firms act as trusted intermediaries, holding custody over client assets and processing payments under KYC/AML mandates. For example, to use Block’s international payment rails, users must verify their identity and transact within the walled garden of the platform.

DeFi, by contrast, breaks this mold entirely. On decentralized platforms, such as MakerDAO or Uniswap, users interact directly with smart contracts. Ownership and custody always remain with the user. For instance, transferring Dai stablecoin (pegged 1:1 to the US dollar and running on Ethereum) requires no bank, no ID, and no reliance on a trusted third party. All transactions are validated by independent miners or validators, and the system remains accessible to anyone regardless of nationality, economic status, or political constraints. DeFi offers an open alternative—one that empowers users, not institutions.

Key DeFi Use Cases: From Lending to Derivatives and Insurance

The range of DeFi applications grows almost daily, with protocols now supporting lending and borrowing, asset management, decentralized exchanges (DEX), synthetic assets, prediction markets, and peer-to-peer insurance. Let’s break down the most critical areas:

Lending and Borrowing: The Backbone of DeFi

Lending and borrowing platforms remain DeFi’s flagship application. Unlike traditional banking—where loan approval may take days, require extensive documentation, and favor the well-connected—DeFi lending is instant, open, and algorithmically managed. Borrowers pledge crypto assets as collateral (typically over-collateralized to offset volatility risk) and receive stablecoins or other tokens in return, while lenders earn yield for supplying liquidity.

- Compound revolutionized money markets on Ethereum, introducing algorithmically-adjusted interest rates based on supply and demand. Collateral assets—like BAT, DAI, ETH, USDC, REP, and ZRX—are wrapped as cTokens for lending and borrowing, with rates dynamically fluctuating. No fixed contracts: everything is permissionless and transparent.

- Dharma offers a semi-centralized P2P lending experience, supporting DAI, ETH, and USDC. Borrowing rates are set by the project’s management team, and the protocol bridges user experience between DeFi and legacy finance.

- MakerDAO lets users lock up ETH and other assets to mint Dai. Unlike purely peer-to-peer models, Maker issues Dai from system-managed reserves and enables users to manage collateral ratios in real time. Recently, Maker added support for multi-collateral Dai, giving borrowers more options to hedge risk.

These platforms have catalyzed the emergence of liquidity mining and yield farming, further incentivizing participation and making DeFi lending one of the most dynamic corners of the digital asset space.

Asset Management: Non-Custodial Portfolios and Automation

DeFi asset management tools function as digital depositories and portfolio managers—without banks or centralized funds. Investors use smart wallets, aggregators, and on-chain analytics to monitor holdings, diversify across protocols, and automate complex strategies. This addresses a long-standing pain point for newcomers: navigating fragmented platforms, optimizing returns, and staying in control.

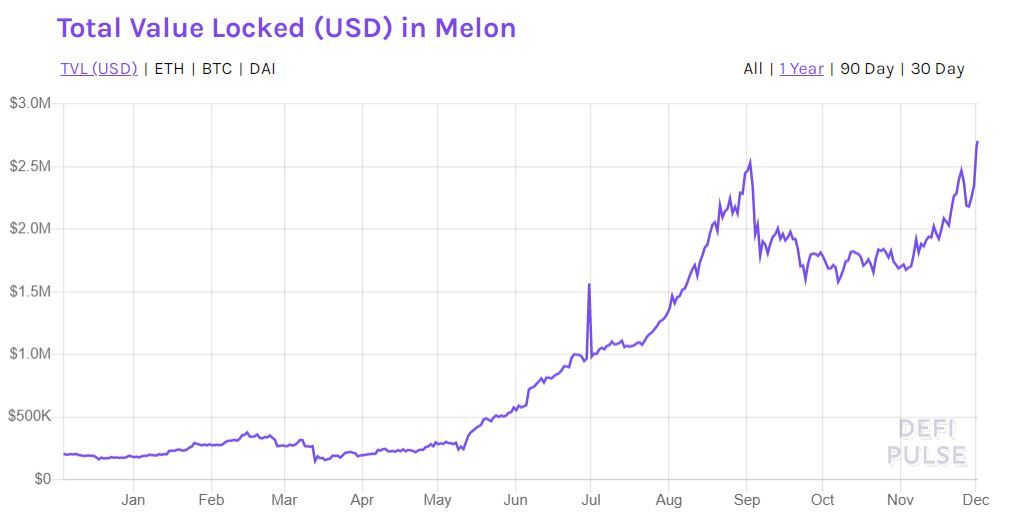

- Melon (now Enzyme Finance) offers decentralized infrastructure for building and managing investment funds on Ethereum, governed by community-run protocols and no central authority.

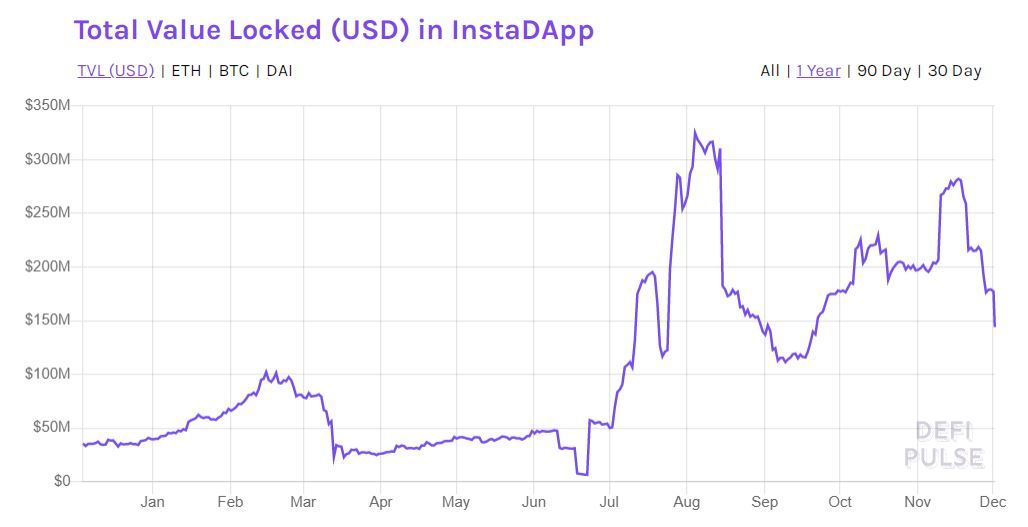

- InstaDApp is a smart wallet overlay for MakerDAO and Compound, enabling seamless management of positions, optimization of yields, and migration of assets across DeFi products—all through a single interface.

A chart showing the amount of assets locked up for Melon. Source: DeFi Pulse

A chart showing the amount of assets locked up for Melon. Source: DeFi Pulse  Number of assets locked for InstaDApp needs. Data: DeFi Pulse

Number of assets locked for InstaDApp needs. Data: DeFi Pulse Derivatives: On-Chain Synthetic Assets and Risk Management

DeFi has unlocked the possibility of tokenized derivatives—contracts whose value tracks the performance of crypto, fiat, equities, or commodities. These contracts are enforced by code, not clearinghouses, giving users direct exposure to price movements and sophisticated hedging strategies.

- UMA (Universal Market Access) allows anyone to design and deploy custom financial contracts, such as synthetic tokens, options, or perpetuals, with settlement based on decentralized price feeds (oracles).

- Synthetix serves as a protocol and decentralized exchange for minting and trading synthetic assets (Synths), giving users access to synthetic USD, gold, stocks like Apple or Tesla, and even crypto indices. All positions are over-collateralized and settled on-chain.

Unlike legacy markets, DeFi derivatives are programmable, globally accessible, and offer settlement within minutes, not days. This levels the playing field for retail and institutional traders alike.

Insurance: Mitigating On-Chain Risk

In an ecosystem prone to hacks, bugs, and protocol failures, DeFi insurance is critical. Instead of relying on centralized insurance underwriters, users pool risk and share claims directly on-chain. The leading player, Nexus Mutual, offers smart contract and exchange insurance by pooling deposited ETH and issuing NXM tokens. Policies are purchased and claims voted on by members, creating a community-driven model of decentralized risk protection.

New entrants are exploring insurance for wallet keys, DeFi protocol failures, and event-based coverage—pointing to a future where risk is democratized and governed transparently.

Nexus Mutual Cryptocurrency Chart. Data: CoinGecko

Nexus Mutual Cryptocurrency Chart. Data: CoinGecko Key Risks: Smart Contracts, Oracles, and Systemic Limits

Despite its advantages, DeFi introduces a new set of vulnerabilities that require constant vigilance:

- Smart Contract Risks: Open-source code, while transparent, can be exploited. The infamous DAO hack is a prime example, where attackers leveraged a bug to steal nearly one-third of DAO’s ETH. Even today, exploits and “rug pulls” pose a threat to users who do not audit code or understand contract logic.

- Oracle Centralization: DeFi protocols often rely on oracles to pull in external data (like asset prices). Malfunctioning or manipulated oracles can trigger massive losses—one Synthetix incident allowed a trading bot to extract over $1B due to a price feed error, highlighting the risks of relying on a single data source.

- Capital Inefficiency: Most DeFi loans require overcollateralization, which means users must lock up assets exceeding the value of the loan. While this mitigates default risk, it limits capital efficiency compared to traditional lending.

Other emerging concerns include regulatory uncertainty, user error (lost keys or funds), and the possibility of governance attacks on protocol DAOs. The permissionless nature of DeFi is empowering but demands user education and technical literacy.

DeFi’s Market Growth and the Road Ahead

DeFi’s exponential rise is reflected in the total value locked (TVL) across protocols, which regularly exceeds $900M and continues to set new records. Its rapid expansion has spurred the growth of entire new sectors within crypto: from automated market makers (AMMs) like Uniswap to prediction markets, decentralized asset management, and NFT financialization.

DeFi’s success is driving Ethereum’s dominance as the backbone of on-chain finance, but competing ecosystems on Solana, Avalanche, and Binance Smart Chain are gaining ground. Institutional adoption is on the rise, and new products like liquid staking, permissioned DeFi, and hybrid protocols are bridging the gap with traditional finance.

Still, DeFi remains a challenger to legacy finance—an experimental, rapidly evolving frontier. Mass adoption will require solving for user experience, regulatory clarity, and cross-chain interoperability. Yet as banks, fintechs, and governments explore blockchain, DeFi’s trajectory points to a future where open, programmable finance becomes a standard—not an exception.

Conclusion: DeFi as a Catalyst for Financial Paradigm Shift

Decentralized finance has redefined what’s possible in global markets, offering accessible, transparent, and trustless services previously controlled by legacy institutions. While challenges persist—from smart contract exploits to liquidity fragmentation—DeFi’s innovation curve shows little sign of slowing. As regulatory frameworks evolve and technology matures, DeFi is set to play a central role in shaping the next era of digital finance.

For users, developers, and investors alike, understanding DeFi is no longer optional—it's essential for navigating and thriving in the new world of programmable money.