Vetle Lunde, head of research at K33, explained that the gap between mNAV and BTC value effectively means companies are giving away more equity than they are getting back.

Discounted share issuance has led to dilution, limiting some corporate buyers’ ability to raise additional capital for their treasuries.

Crypto firm Nakamoto — formed from the merger of KindlyMD and Nakamoto Holdings — saw its stock collapse, losing more than 95% from its peak. Its mNAV crashed from 75 to just 0.7.

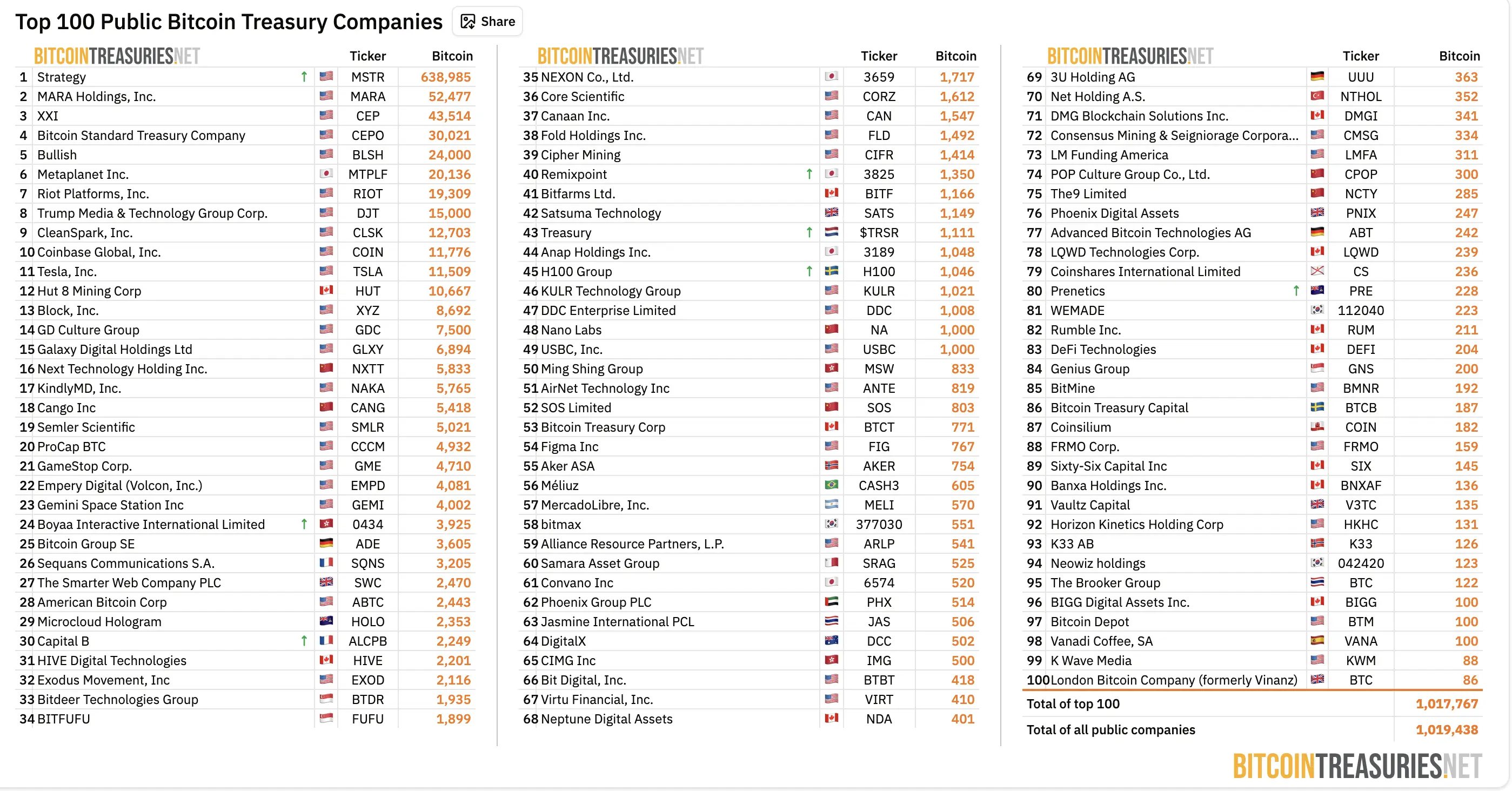

Data from Bitcoin Treasuries shows that other firms trading at heavy discounts include Twenty One, Semler Scientific, and The Smarter Web Company.

On September 16, streaming and e-commerce firm GD Culture Group (GDC) also saw its shares plunge. After announcing the purchase of 7,500 BTC from Pallas Capital Holding for $875 million, its stock fell 28% before beginning a modest recovery.

The company shifted its focus to building a diversified crypto reserve, but investors reacted cautiously, reflecting concerns about heavy dilution and the risks of a speculative treasury strategy.

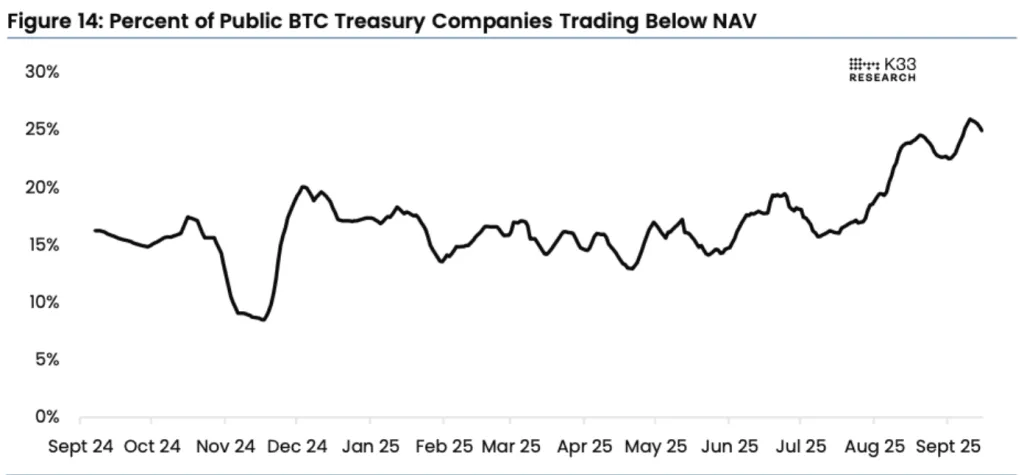

In September, the average mNAV among public treasury firms dropped to 2.8, down from 3.76 in April, K33 reported.

Lunde noted that smaller firms are increasingly falling into discount territory, while larger players still trade at a premium.

Strategy (MicroStrategy) holds about 64% of all corporate bitcoin reserves, with 638,985 BTC on its balance sheet. Yet even the sector leader shows troubling signs: MicroStrategy’s stock premium over BTC value fell to 1.26, its lowest since March 2024.

“This severely limits Strategy’s ability to buy bitcoin and signals weaker demand from one of last year’s biggest market absorbers,” Lunde explained.

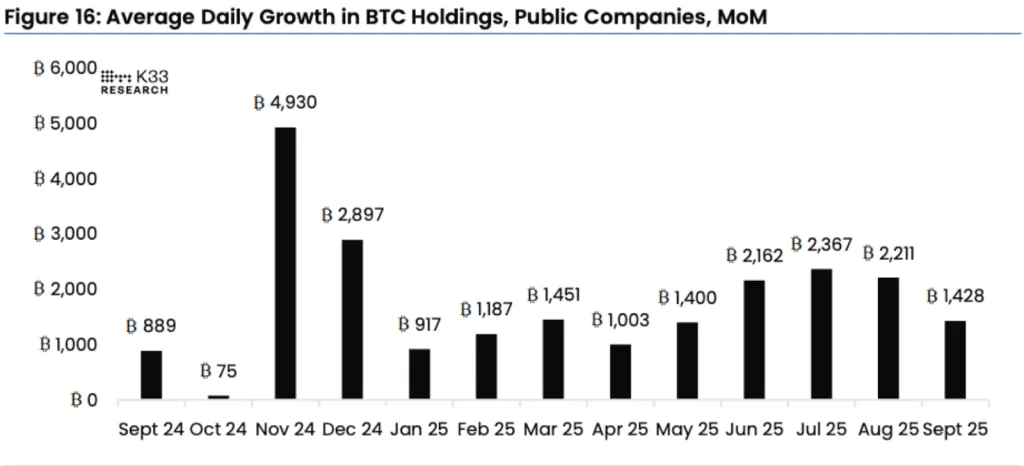

The pace of accumulation has also slowed. In September, corporate treasuries added only 1,428 BTC per day, the weakest rate since May.

Lunde called shrinking premiums “rational,” citing high advisory fees, insider incentives, and complex capital structures. Still, he expressed hope in companies that can leverage their bitcoin reserves across other business lines.

Analysts suggest spot ETFs and retail inflows are becoming the primary drivers of demand.

New Wave of Adoption Meets Technical Bottleneck

A new stage of institutional adoption is underway as major fintechs begin developing their own blockchains, Altius Labs co-founder Annabelle Huang.

The Web3 landscape has shifted beyond retail hype cycles.

— Annabelle Huang (@_annabellehuang) August 22, 2025

We're witnessing a maturing industry that's capturing institutional attention like never before.

Institutions like @Stripe and @RobinhoodApp are now building their own chains, demanding enterprise-grade infrastructure…

Huang, who started as a trader in New York before joining Amber Group in Hong Kong as a partner, now focuses on building a modular execution layer at Altius Labs. The goal is to connect directly to existing blockchains, improving throughput without forcing projects to rebuild infrastructure.

Robinhood recently announced development of its own L2 blockchain to support tokenized stocks and real-world assets, while Stripe unveiled plans for Tempo, a payments-focused network co-designed with Paradigm.

“What we’re seeing now — and what I expect to continue — is a trend of institutional players adopting stablecoins or even building their own blockchains for specific use cases,” Huang said.

She sees this as the next stage of institutional blockchain adoption. But, like many existing crypto networks, scalability remains the weak point.

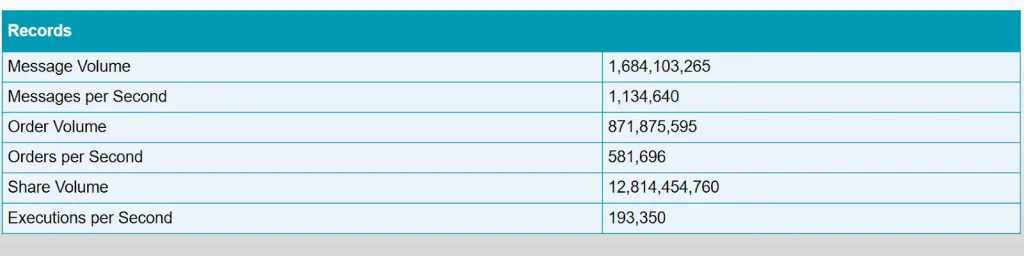

Nasdaq data highlights the gap: during peak load, the exchange can process 581,696 orders and 1,134,640 messages per second — figures that dwarf even high-performance networks like Solana.

Huang called speed “the bottleneck of execution” and said it must be solved before fintech-built chains can handle institutional-scale capital.

“The industry shouldn’t expect new ‘Ethereum killers’ or dozens of general-purpose blockchains,” she added. “Users tend to consolidate around a few dominant platforms rather than scatter across many.”

She also warned about the risks of bitcoin treasury strategies, especially for retail investors, since not all corporate approaches are equally structured. Comparing stock spikes to token launches, she argued that demand for proxy assets like ETFs and treasury strategies will persist.

While ETFs already exist for bitcoin and Ethereum, Huang noted that investors seeking altcoin exposure often turn to debt-based products.