High debt levels, rising yield pressure, and technological disruption: Jamie Dimon sees warning signs that resemble the years leading up to the last major crisis. But how might Bitcoin behave in such a scenario?

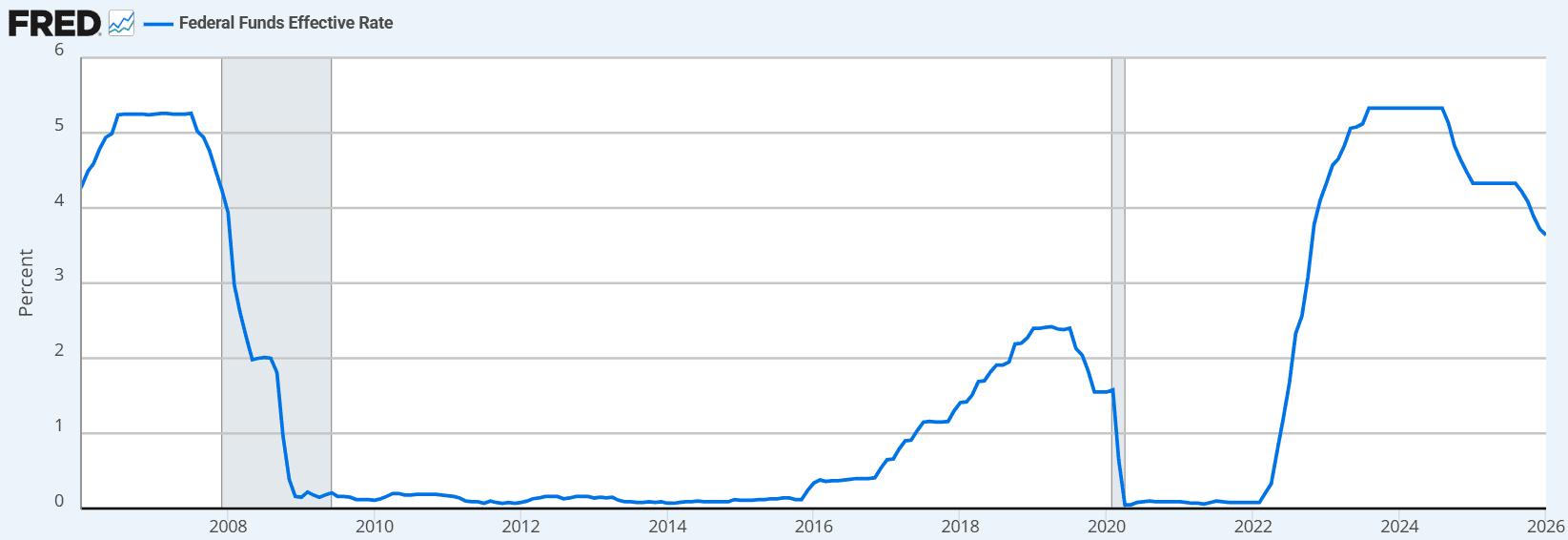

JPMorgan CEO Jamie Dimon draws parallels between today’s environment and the 2008 financial crisis. Back then, excessive risk-taking and looser lending standards triggered a global shock. Dimon now warns that some market participants are once again doing “stupid things.” Many governments—above all the United States—are burdened with trillions of dollars in debt, while artificial intelligence is creating new zones of uncertainty.

How the 2008 escalation began

The 2008 financial crisis began in the U.S. housing market. Banks issued mortgages on a massive scale to borrowers with weak credit profiles—so-called subprime loans. These claims were bundled, securitized, and sold to investors. As long as home prices kept rising, the system looked stable and profitable. But the search for yield masked growing risks.

When housing prices started to fall and many borrowers defaulted, structured products rapidly lost value. Uncertainty over the true scale of the risks triggered a massive loss of confidence. The crisis peaked with the collapse of Lehman Brothers in September 2008. Credit markets effectively froze, companies struggled to obtain financing, and the global economy slipped into a deep recession. Governments and central banks had to step in with large-scale rescue packages.

Yield pressure and looser standards

Dimon points out that, even before 2008, many institutions weakened lending standards in order to boost net interest income. In periods of stable economic growth, market participants tend to underestimate risk more easily. Competition intensifies this effect, as market share and short-term profits take center stage. According to Dimon, this is exactly the pattern he partly sees again today. Some players are willing to take on more risk for a little more yield.

Particularly strong growth in recent years has been seen in the private credit and leveraged loan segments. Private credit refers to loans issued not by traditional banks, but by specialized funds or asset managers directly to companies. These deals often sit outside traditional bank balance sheets and are subject to different transparency requirements. Leveraged loans, meanwhile, are high-yield corporate loans extended to already heavily indebted companies, often to finance acquisitions. Both segments can be lucrative, but they also carry elevated default risks if the economy deteriorates.

The credit cycle and the inevitable surprise

Credit markets move in cycles. In good times, default rates fall, valuations rise, and risk premiums shrink. But as Dimon warns directly, “every credit cycle has a surprise.” No one knows in advance where it will appear or which sector it will hit. “This time it could be software because of AI,” he said, pointing to the rapid transformation caused by artificial intelligence. AI is seen as a disruptive technology capable of reshaping—or displacing—entire business models. Companies are being forced to reassess how automation and intelligent systems will affect revenue and cost structures.

At the same time, uncertainty is growing over which jobs will disappear and which new ones will emerge. If it turns out that expectations were overblown and investments fail to deliver the hoped-for returns, that could become the next unpleasant surprise in the credit cycle.

Bitcoin as a product of the previous crisis

Bitcoin was born in 2009, in the shadow of the financial crisis. Its genesis block famously included the line: “The Chancellor on brink of second bailout for banks.” This was a direct reference to government bank rescues and ultra-loose monetary policy. The cryptocurrency was designed as a decentralized alternative to the existing financial system. Its maximum supply is capped at 21 million coins.

That scarcity fundamentally distinguishes Bitcoin from fiat currencies. While central banks can expand liquidity in times of crisis, Bitcoin’s supply remains algorithmically fixed. For many investors, that is exactly what makes it attractive. When confidence in banks or fiat currencies weakens, the “digital gold” narrative comes to the fore. Even so, in the short and medium term Bitcoin remains dependent on market sentiment.

Liquidity is what matters

If the credit cycle begins to deteriorate materially, the first effect would likely be a market shock. In acute phases of stress, investors typically sell risky assets to raise liquidity. In such a scenario, Bitcoin could also fall at first.

Only in the next phase would it become clear where capital is likely to flow over the longer term. If central banks respond with rate cuts and bond-buying programs, the global money supply will expand. But rising liquidity alone does not guarantee a rise in Bitcoin. The key question is whether investors will actually direct that additional liquidity into alternative assets. A growing money supply merely creates the potential for higher prices. Without real capital inflows, the effect will remain limited.

At the same time, Bitcoin has a structural feature—verifiable supply scarcity—that sets it apart from fiat currencies. Over the long run, rising money supply could reinforce that narrative. But investors should remain realistic: in the acute phase of a global financial crisis, the price would most likely come under pressure first. Only after markets stabilize and new capital flows emerge could a positive correlation with looser monetary policy reassert itself.

Bitcoin amid rising systemic risks

Jamie Dimon’s remarks are not proof that a financial crisis is inevitable. Rather, they are a reminder that credit cycles tend to repeat. Parallels with the pre-2008 period usually become clearer in hindsight than they are in real time. It is always easier after the fact to see where risks were underestimated and bad incentives were ignored. That is exactly why warning signals should be taken seriously without automatically turning them into a forecast of imminent catastrophe.

For investors, the main takeaway is straightforward: it is important to consciously reassess the risk structure of one’s portfolio. Those already in the market should look not only at potential returns, but also at scenarios that could prove far less comfortable.