The initiative is aimed at addressing a systemic issue long faced by crypto-native companies. Traditional banking payment rails often fail to meet the speed and constant availability required by the digital economy. Delays in international settlements remain commonplace. Ripple Payments offers a different model — continuous settlement without dependence on banking operating windows.

For Ripple, this marks the deployment of licensed blockchain infrastructure directly within the operational processes of a European bank. For AMINA, it represents an expansion of payment capabilities while remaining fully within regulatory boundaries. Both parties emphasize that this is a production-grade infrastructure solution rather than a pilot experiment.

Connecting Fiat and Blockchain in a Unified System

AMINA Bank plans to use Ripple Payments to process both fiat transfers and stablecoin transactions through a single platform. The solution supports regulated stablecoins, including Ripple USD (RLUSD), alongside traditional currencies. This approach bridges the infrastructure gap between legacy payment systems and on-chain settlement.

According to AMINA Bank’s Chief Product Officer, Myles Harrison, Web3 companies frequently encounter limitations when operating through outdated banking mechanisms. He noted that cross-border stablecoin transactions remain difficult largely due to insufficient support from banks. In his view, the integration of Ripple Payments removes a significant portion of these barriers.

Harrison also highlighted that the transition to a 24/7 settlement model reduces delays and eliminates time constraints typical of correspondent banking. As a result, clients gain more stable and predictable settlement cycles.

Regulatory Framework and Ripple’s Network Scale

Cassie Craddock, Ripple’s Managing Director for the UK and Europe, stated that the partnership with AMINA positions the bank as an entry point for digital asset companies seeking to operate within the traditional financial system. According to her, Ripple’s payment technology connects fiat infrastructure and blockchain networks within a fully compliant framework.

AMINA Bank is headquartered in Zug and operates under the supervision of the Swiss Financial Market Supervisory Authority (FINMA). The bank has also expanded its regulatory presence into Abu Dhabi and Hong Kong, enabling it to serve clients across multiple jurisdictions.

Ripple notes that its payments network covers more than 90% of global foreign exchange markets operating on a 24-hour basis. The total volume of processed transactions exceeds $95 billion, while the company’s licensed payment services are active in the United States, Switzerland, Singapore, Brazil, Mexico, Australia, and Dubai.

The integration of Ripple’s solution into AMINA’s infrastructure has drawn attention from institutional observers assessing the prospects of blockchain-based settlement within the regulated banking sector. For many banks, this case has become a practical reference point.

XRP Declines Amid Market Pressure

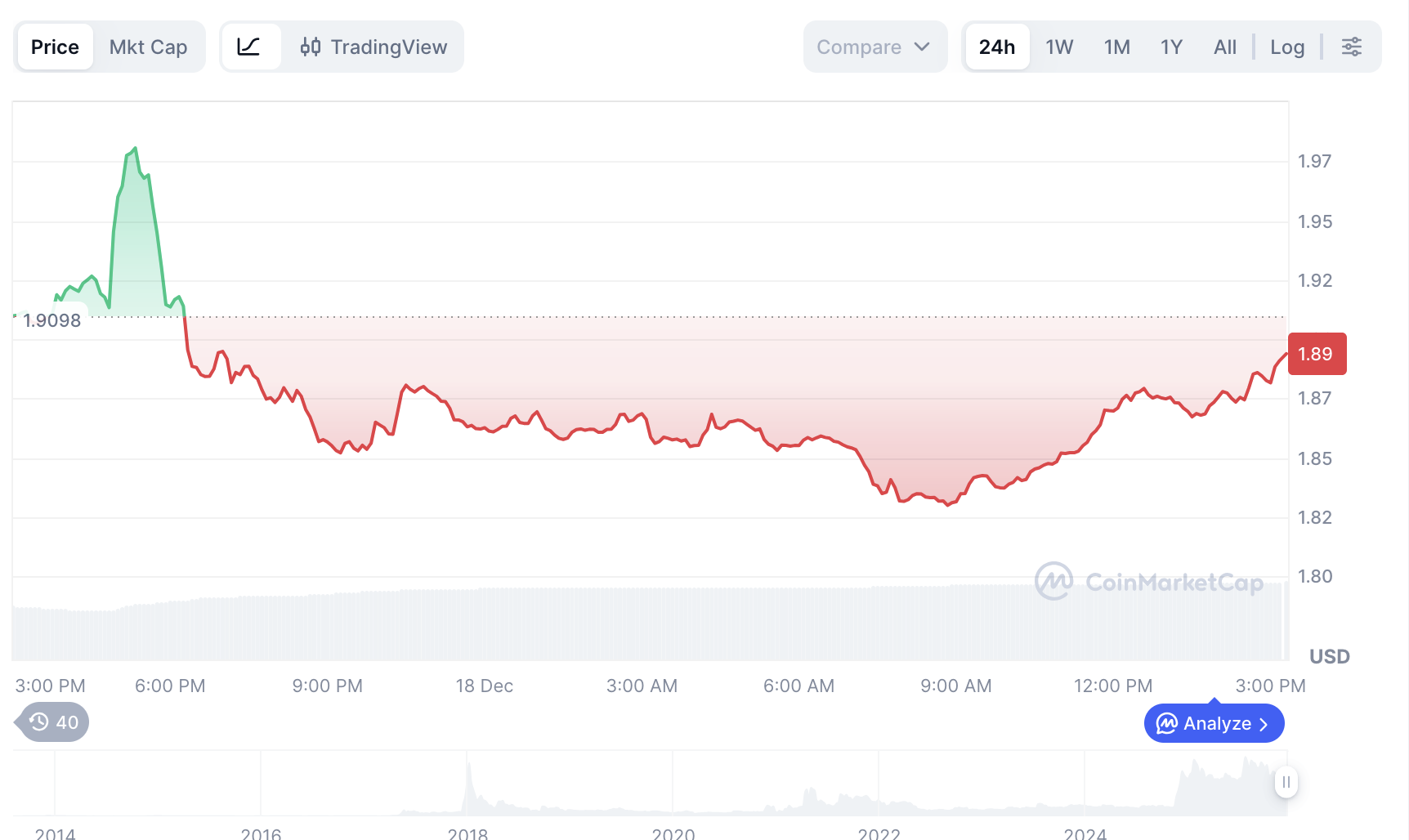

Despite Ripple’s expanding institutional footprint, the XRP token came under selling pressure over the past 24 hours. According to CoinMarketCap data, the price fell to $1.89, down approximately 4.0% on the day. During the session, the price briefly rose toward $1.97 but failed to hold those levels. Subsequently, the chart formed a series of lower highs, particularly evident during the Asian trading session.

XRP’s market capitalization declined to approximately $111.5 billion, while 24-hour trading volume reached $3.57 billion, indicating active position turnover. Market participants noted that the $1.90 level failed to hold, shifting focus to the $1.80 area as the nearest technical support.