Building a unified infrastructure for tokenized money

Both financial institutions already use their own private blockchain systems that enable instant transfers, but these networks remain isolated. The new protocol will allow clients to send funds directly between banks while preserving the “singleness of money” — meaning the legal and regulatory integrity of a deposit during digital transfer.

According to Naveen Mallela, Co-Head of Kinexys at JPMorgan, the project demonstrates how major institutions can expand the use of tokenized deposits without breaching regulatory standards.

Earlier, JPMorgan issued a U.S. dollar deposit token on the Base (Coinbase) blockchain, showing how regulated assets can function within open, decentralized ecosystems. The new collaboration with DBS builds on this idea, connecting a public blockchain with a private banking network: a JPMorgan client will be able to send tokenized U.S. dollars to a DBS client, who can redeem or hold those tokens within the DBS system, completing a regulated on-chain transaction.

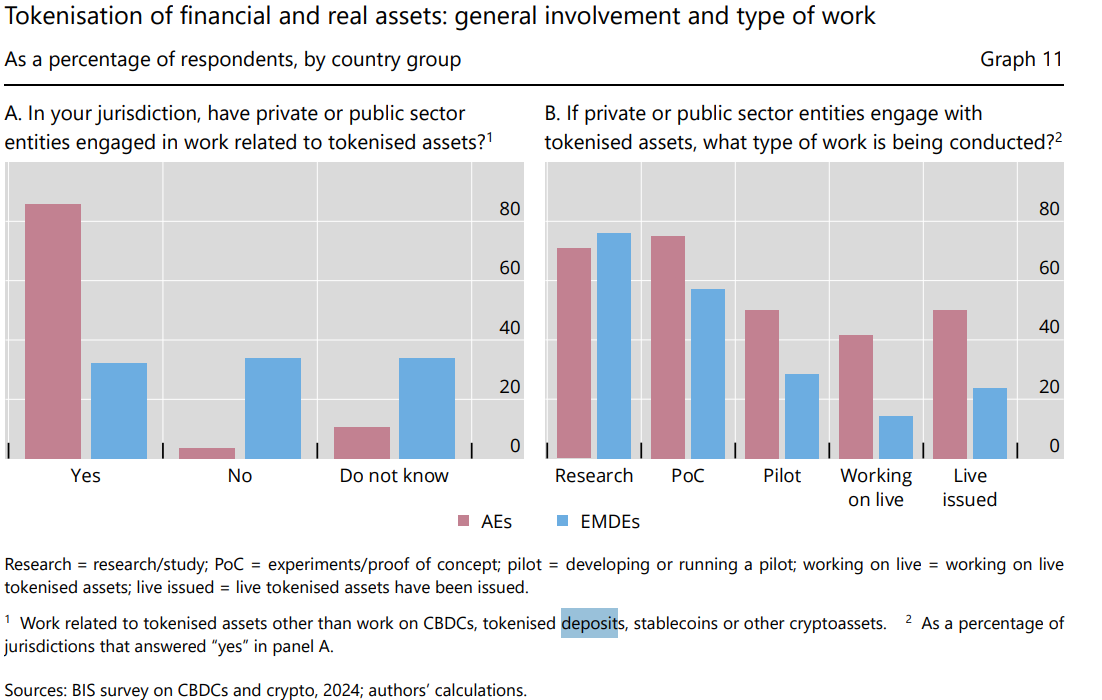

By 2024, at least one-third of surveyed commercial banks had launched, tested, or explored tokenized deposit models, according to a study by the Bank for International Settlements (BIS).

The next phase of digital money

The project reflects growing interest among banks in programmable money and in integrating blockchain settlement layers with traditional financial infrastructure. JPMorgan and DBS believe that tokenized deposits could serve as a bridge between CBDCs (central bank digital currencies) and stablecoins, enabling instant cross-chain transfers without risk to clients.

Unlike stablecoins, tokenized deposits are backed by real funds held in regulated bank accounts, ensuring full compliance with financial regulations.

According to the Bank for International Settlements (BIS), about one-third of global banks are already testing such models to improve international payment efficiency and reduce transaction costs.

By linking Kinexys and DBS Token Services, the banks aim to prove that interoperability between public and private blockchains is possible, paving the way for broader cooperation among other financial institutions.

The new structure was announced two weeks after JPMorgan initiated its first transaction on the upcoming tokenization platform, Kinexys Fund Flow, as reported by FORECK.INFO on October 29.

Practical significance

The potential of this technology extends beyond retail payments. Cross-chain deposits could simplify corporate settlements, treasury operations, and international trade finance, while also providing a foundation for CBDC integration. This would allow central banks to interact directly with commercial banks in a digital format.

For JPMorgan and DBS, this marks a major step toward bringing blockchain technology into the core of the global financial system — moving from pilot programs to a real-world infrastructure that unites digital assets and regulated money.