The letter criticizes long-standing restrictions that effectively confine most retirement investors to stocks and bonds. Lawmakers argue that existing rules block access to regulated alternative instruments despite the evolution of financial markets. They are calling for coordinated action between the SEC and the U.S. Department of Labor to align federal oversight with changing investment demand.

Lawmakers push for regulatory alignment

In their December 11 appeal, lawmakers referenced President Trump’s August 2025 executive order directing the SEC and the Department of Labor to revise regulations that limit investment options within 401(k) plans. Congress urged the agencies to provide legal clarity that would allow retirement plan fiduciaries to offer a broader range of assets.

According to White House data, total U.S. retirement assets reached $43.4 trillion as of March 31, 2025. Despite this scale, most savers still lack access to alternative investments. Lawmakers emphasize that this gap reflects outdated policy rather than current market realities. In their view, retirement strategies should reflect the modern structure of capital markets.

Supporters of the initiative believe that modest allocations to alternative assets could improve risk-adjusted returns, while diversification could enhance long-term retirement outcomes. The letter stresses that the effort represents system modernization rather than deregulation.

Trillions of dollars in retirement capital at stake

U.S. 401(k) plans hold approximately $12.5 trillion in assets, while total retirement savings exceed $43 trillion. Analysts note that even small reallocations could have a noticeable market impact: shifting just 1–3% of assets could translate into tens of billions of dollars in inflows.

Experts suggest that such flows could affect Bitcoin’s price dynamics, given its limited supply and existing institutional demand. Although the letter does not cite specific price targets, the potential scale of inflows has drawn significant attention. The key question is whether retirement savings could become the next major source of demand for Bitcoin.

Industry representatives describe the potential changes as a turning point for digital asset adoption. Retirement plans are increasingly viewed as a bridge between crypto markets and traditional finance. The debate is shifting from access toward structure and implementation mechanisms.

Firms prepare, but safeguards remain central

Several financial firms have already begun preparing for possible regulatory changes. Some retirement plan providers are exploring partnerships with institutional crypto custodians. Such models could allow employees to allocate up to 5% of their contributions to digital assets, subject to regulatory approval.

For example, ForUsAll is partnering with Coinbase Institutional under a similar framework. This arrangement would enable plan participants to direct a limited portion of their retirement savings into crypto assets. Coinbase’s CEO has previously stated that Bitcoin and other cryptocurrencies will eventually become a standard component of “every 401(k).”

At the same time, lawmakers and experts emphasize the need for robust safeguards. Bitcoin’s volatility remains a key risk factor. Retirement plan sponsors and fiduciaries would require clear risk-management rules and investor education programs. SEC Chair Paul Atkins has not yet outlined a specific timeline but has acknowledged the agency’s role in implementing the executive order alongside other regulators.

Opposition to the use of cryptocurrencies in pension funds is growing

Resistance to allowing cryptocurrencies in U.S. pension funds continues to intensify. While supporters of digital assets argue that their inclusion in retirement portfolios expands access to modern financial instruments and helps democratize investing, labor unions have taken a sharply opposing stance.

Labor representatives warn that loosening rules for retirement programs would introduce additional risks for savers. In their view, the high volatility of cryptocurrencies makes them unsuitable for traditional pension schemes designed to prioritize stability and predictable income.

American Federation of Teachers (AFT) President Randi Weingarten sharply criticized efforts to expand the role of crypto assets in retirement savings on Thursday:

“Unregulated and high-risk currencies are not where retirement savings belong. We do not need the ‘Wild West’—whether it’s cryptocurrencies, artificial intelligence, or social media,” she said.

The AFT represents approximately 1.8 million teachers and education professionals nationwide and remains one of the largest teachers’ unions in the United States, giving its position significant political weight.

Criticism has also come from analytical organizations. The non-profit, non-partisan group Better Markets argues that cryptocurrencies are poorly suited to long-term retirement strategies due to sharp price fluctuations. Experts point to a mismatch in investment horizons: the high volatility of digital assets runs counter to the goals of pension funds focused on low volatility and predictable payouts.

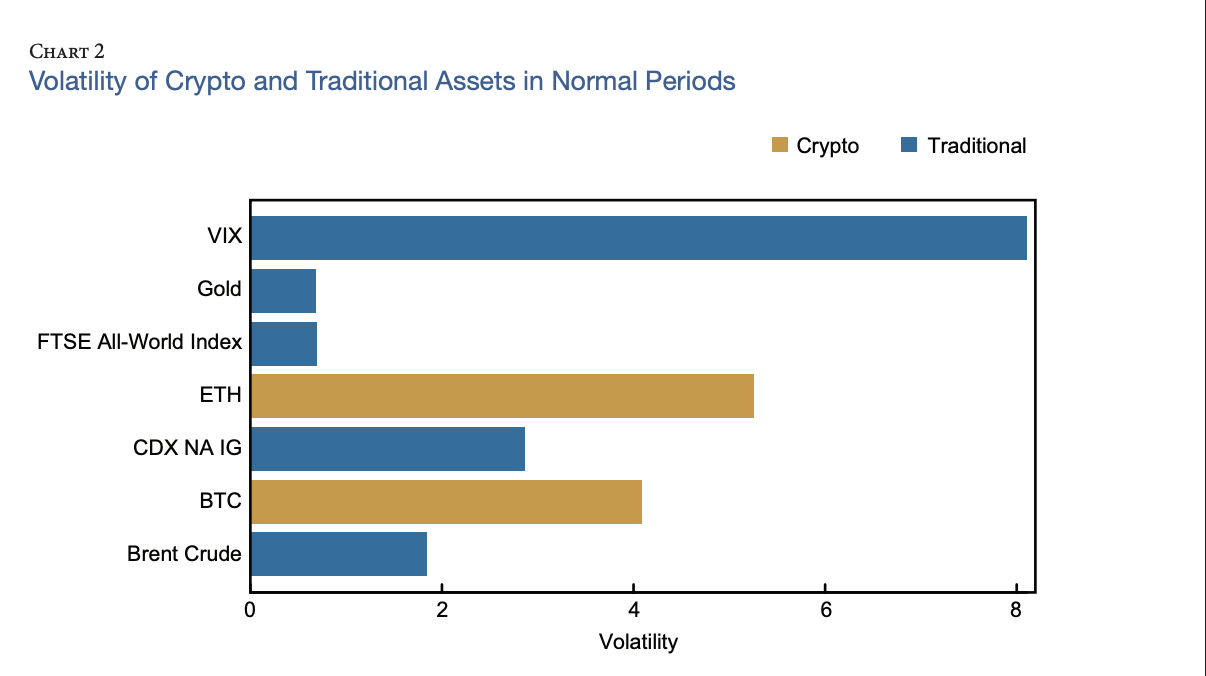

Data from the U.S. Federal Reserve further highlight the issue, showing that the volatility of Bitcoin and Ether far exceeds that of traditional asset classes and stock indices commonly used in retirement portfolios.

Earlier, in October, the American Federation of Labor and Congress of Industrial Organizations (AFL-CIO) also made its position clear by sending a letter to Congress criticizing provisions of a bill aimed at regulating the structure of the cryptocurrency market.

The largest labor federation in the United States stated that digital assets remain unstable and could pose a systemic risk to both pension funds and the broader financial system if access is expanded without strong protective safeguards.