Prime Minister Keir Starmer has come under pressure following the appointment of Peter Mandelson as UK ambassador to the United States. Mandelson was later dismissed after his name appeared in materials related to the case of US financier Jeffrey Epstein. The situation led to the resignation of Downing Street Chief of Staff Morgan McSweeney and Communications Director Tim Allan, who took responsibility for approving the appointment of the key ideologue of “New Labour” to lead the UK diplomatic mission in Washington. Market participants are now assessing the likelihood of Starmer stepping down after the May elections.

At the same time, investors remain focused on macroeconomic data. In January, retail sales rose from 0.4% to 1.8% month-on-month and from 1.9% to 4.5% year-on-year, while the core indicator increased from 0.3% to 2.0% and from 2.5% to 5.5%, respectively. The February services PMI came in at 53.9 points, only slightly below the previous 54.0, while the manufacturing PMI accelerated from 51.8 to 52.0. This improvement was the main driver behind the rise in the composite index from 53.7 to 53.9.

According to Jake Finney, senior economist at PricewaterhouseCoopers, private sector activity has been expanding at a solid pace for the second consecutive month, reflecting a recovery compared with last year. However, companies remain focused on efficiency gains and cost reduction, leading to job cuts and further cooling of the labour market that began after the publication of the Autumn 2024 budget. Corporations are increasingly using artificial intelligence to replace tasks previously performed by employees, boosting productivity among remaining staff.

Overall, this aligns with official data showing a steady rise in unemployment, making a rate cut by the Bank of England from the current 3.75% next month increasingly likely. On February 5, the decision to keep rates unchanged was passed by a narrow margin of five votes to four, with the minority supporting a 25-basis-point cut.

As earnings season comes to an end and capital flows out of equities, bond markets have seen a modest decline in yields. One-year gilt yields eased from 3.574% at the end of last week to 3.556%, 10-year yields fell from 4.391% to 4.346%, 20-year yields slipped from 5.064% to 5.036%, and 30-year yields declined from 5.179% to 5.159%.

Top gainers within the index included Diageo Plc (+3.90%), Burberry Group Plc (+3.32%), Antofagasta Plc (+3.02%) and British American Tobacco Plc (+2.15%).

The weakest performers were Intchains Group Ltd (–4.17%), BP Plc (–2.38%), Associated British Foods Plc (–1.16%) and Mondi Plc (–0.92%).

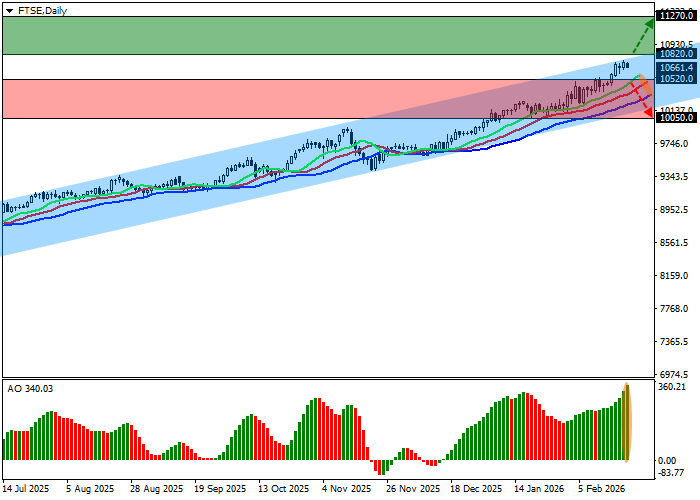

Support and resistance levels

On the four-hour chart, the index is approaching the upper boundary of an ascending channel with limits at 10,900.0–10,000.0.

Technical indicators are strengthening the buy signal: the EMA range of the Alligator indicator is expanding, while the Awesome Oscillator histogram is forming corrective bars in positive territory.

Resistance levels: 10,820.0, 11,270.0.

Support levels: 10,520.0, 10,050.0.

Trading scenarios and FTSE 100 outlook

Long positions can be opened after a breakout and consolidation above 10,820.0, targeting 11,270.0 with a stop-loss at 10,550.0. Time horizon: 7 days or longer.

Short positions can be considered after a decline and consolidation below 10,520.0, with a target at 10,050.0 and a stop-loss at 10,730.0.