Dragonfly investor Omar explained that Circle’s main cash flow comes from the yield generated by the U.S. Treasuries that stand behind every issued USDC token. If the Fed reduces its benchmark rate, those bonds will produce less income — directly dragging down Circle’s profitability.

This will play out in the months ahead, but interest rate cuts are horrendous for rate sensitive names like Circle

— Omar (@TheOneandOmsy) August 13, 2025

- A 100bps cut slashes run rate gross revenue by $618m (-23%), gross profit $303m (-30%), and margins 3.3%

- Valuation wise, takes an expensive stock trading at 42x… https://t.co/7lbPYUdfK3 pic.twitter.com/FspLbdUD8N

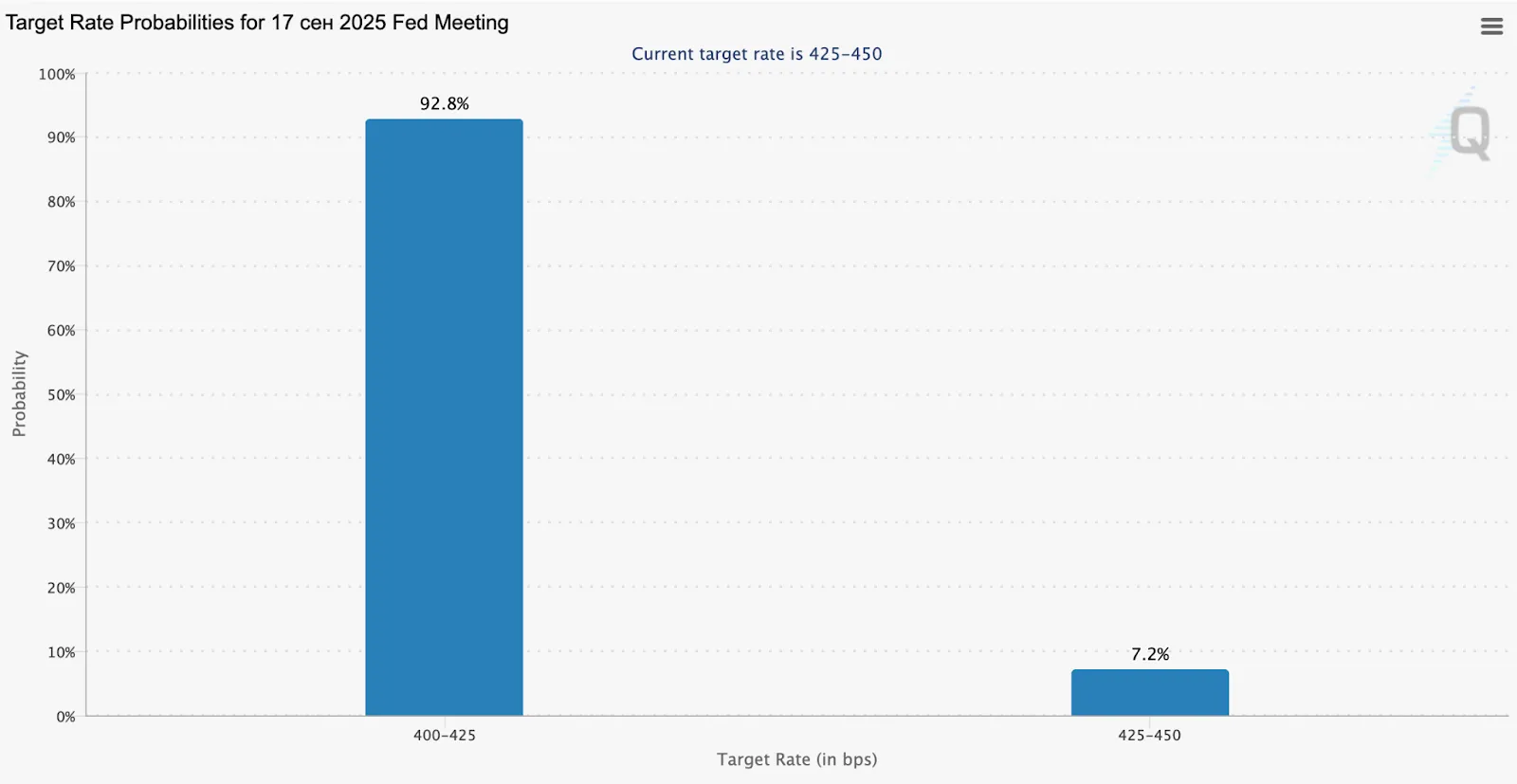

Market expectations are tilted heavily toward easing: according to the CME FedWatch Tool, almost 93% of traders believe a cut is coming in September.

Omar calculated the damage: a full 1% reduction in rates could shave $618 million off Circle’s annual revenue, cutting gross profit by more than $300 million. To make up for that loss, the company would need to mint an additional $28 billion worth of USDC — an expansion of about 44% compared to the token’s present $64 billion supply.

Almost 93% of market participants expect a softening of the regulator’s policy. Source: CME FedWatch

Other analysts argue that Circle already saw the risk coming. The well-known commentator MartyParty suggested the firm’s decision to build its own Arc blockchain is part of a long-term survival plan. Instead of letting networks like Ethereum or TRON collect all the transaction fees, Circle could start capturing some of that revenue itself by controlling the infrastructure.

To be clear - when interest rates drop @circle and @Tether_to will lose a lot of revenue - remember they hold interest bearing treasuries. When interest rates drop they will need to issue more stable coin to maintain their current revenue which equates to their valuation.

— MartyParty (@martypartymusic) August 15, 2025

This… pic.twitter.com/opoxQ0031C

The company has also rolled out the Circle Payments Network (CPN), a system designed to link businesses and consumers more directly to USDC. And in a show of investor confidence, Circle recently disclosed that it will release 10 million shares on the secondary market at $130 apiece — four times the IPO price set just two months earlier - writes CoinDesk

The timing underscores the delicate balance Circle faces: higher token adoption and new tech on one side, and shrinking income from Treasuries on the other.