Yet that growth has caught the eye of regulators — particularly in the U.S., where most stablecoins are pegged to the dollar. In 2025, U.S. authorities passed the first federal law that defines a regulatory framework for the sector. With national debt climbing and broader economic pressures mounting, one question looms: could the White House eventually move to nationalize stablecoin issuers?

Scale That Tempts Washington: Profits, Supply, and Treasury Exposure

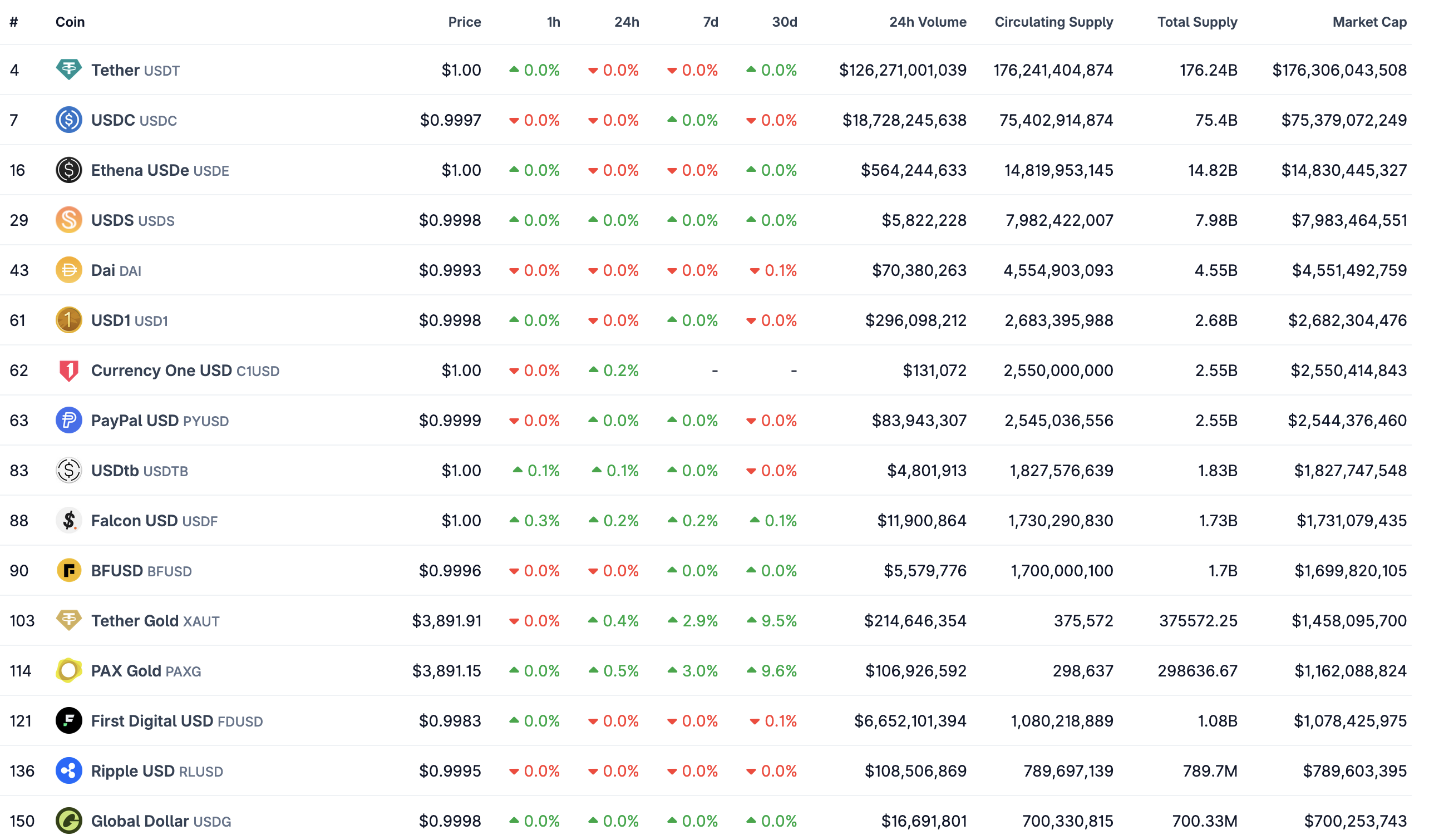

As of October 1, the market capitalization of the market’s dominant player — Tether’s USDT — stood at nearly $175 billion, according to CoinGecko. Trading volume was about $104 billion, while runner-up Circle’s USDC recorded around $9 billion.

In Q2, Tether International Ltd. reported net income of $4.9 billion. From April to June, the USDT issuer minted $13.4 billion — $20 billion since the start of the year. Total circulating supply exceeded 157 billion USDT. The company has also become one of the largest holders of U.S. Treasuries, with $127 billion in exposure (~$105.5 billion directly and ~$21.3 billion indirectly via funds/instruments).

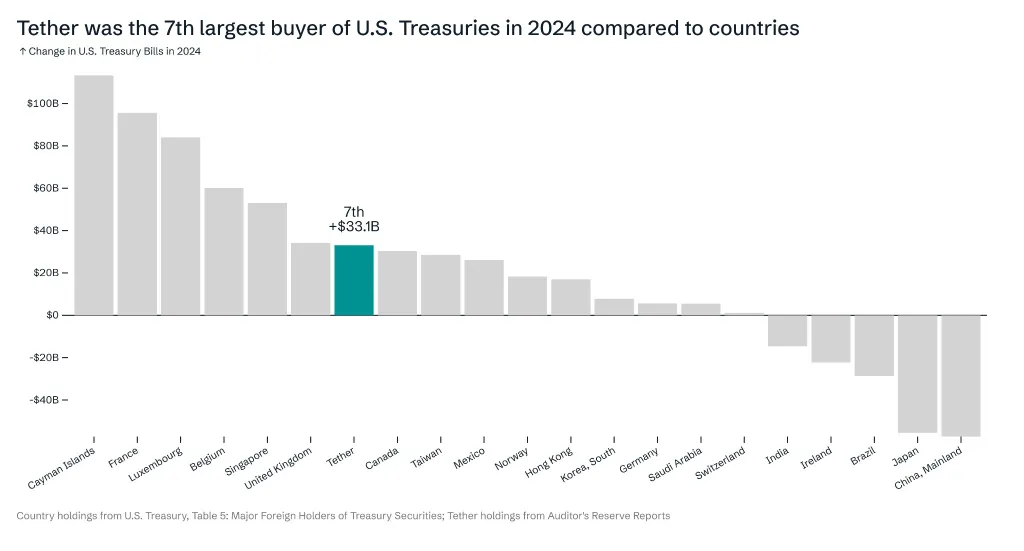

USDC issuer Circle has followed a similar path. Research from ARK Invest (May 2025) indicates that Tether and its closest competitor together would be the 18th-largest holder of U.S. debt — behind South Korea but ahead of Germany. In 2024, the USDT issuer ranked seventh among buyers of U.S. Treasuries, after the U.K. and Singapore.

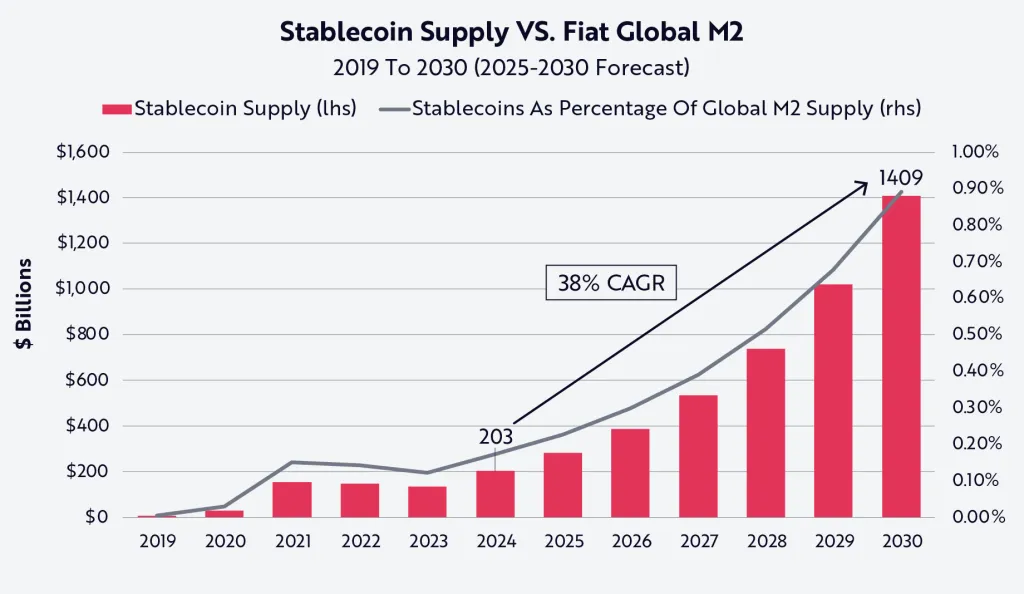

ARK analysts forecast that by 2030, total stablecoin supply could reach $1.4 trillion.

“If Tether and Circle retained their current market shares and their allocations to U.S. Treasuries, together they could hold more than $660 billion in U.S. government debt […]. Clearly, Tether, Circle, and the broader stablecoin industry could become one of the largest sources of demand for U.S. Treasuries in the coming years, potentially replacing China and Japan as leading holders by 2030,” the report states.

By trading volume and market cap, Circle trails the leader, but it has made significant strides in the U.S. On June 5, Circle listed its shares on the NYSE under the ticker CRCL. On day one, the stock rose 168% — from $31 to $82. As of October 1 pre-market, the shares traded substantially higher.

In July, Circle applied to the U.S. Office of the Comptroller of the Currency for a national trust bank charter, while Tether only plans to obtain foreign stablecoin issuer status in the U.S. The USDT issuer has also been actively assisting U.S. law enforcement in freezing suspicious addresses: over the past year, it has blocked a total of $2.9 billion in USDT.

These two largest stablecoin issuers also supported the emergence of the GENIUS Act — a bill setting rules for the sector and the first significant piece of crypto regulation in the U.S.

GENIUS Act, Explained: The New Playbook for Stablecoin Issuers

On July 19, U.S. President Donald Trump signed the GENIUS Act. The ceremony was attended by several industry representatives, including Gemini co-founders Cameron and Tyler Winklevoss, Circle CEO Jeremy Allaire, Tether CEO Paolo Ardoino, and Robinhood CEO Vladimir Tenev.

The law requires full backing of stablecoins with liquid assets and mandates annual audits for issuers with a market cap above $50 billion. It prohibits paying interest or other income to stablecoin holders and sets guidance for foreign companies operating in the segment.

Issuers are also barred from claiming their assets are “backed by the U.S. government, federally insured, or legal tender.” The GENIUS Act takes effect six months after signing or 120 days after regulators issue implementing rules, whichever comes first.

Earlier, Bitget Research chief analyst Ryan Lee told ForkLog the bill “lays the groundwork for a regulatory framework for U.S. dollar-pegged stablecoins.” For Circle, this could mean growing trust, while Tether may face pressure due to higher disclosure requirements, more transparency, and audits.

Trader and Coen+ Telegram channel author Vladimir Coen attributed strong Democratic support to lobbying by giants like Coinbase, Circle, and Gemini, traditional sponsors of the party.

“Gemini, for instance, has its own stablecoin. It’s in their direct interest to pass and implement a law that strengthens U.S.-issued stablecoins while weakening their main competitor — USDT,” Coen added.

According to the expert, crypto-friendly laws in the U.S. will “only strengthen their position and the role of the dollar in the digital asset economy.”

This is especially notable amid rising talk of de-dollarization, also highlighted by ARK Invest. Citing Oilprice data, they note that by end-2023, 20% of global oil transactions were settled in non-dollar currencies.

“Stablecoins occupy a unique position in a changing global financial landscape. They serve as the most liquid, efficient, and convenient wrapper for short-term U.S. debt, effectively removing both obstacles to de-dollarization: preserving U.S. dollar dominance in global transactions while ensuring sustained demand for Treasuries,” the report says.

In the end, ARK Invest believes dollar-pegged stablecoins “could become one of the U.S. government’s most reliable and resilient financial allies.” Their role is most visible where demand for the U.S. currency is highest.

USDC and USDT are widely used in struggling economies: they offer fast dollar access, cheaper remittances, and inflation protection. This steady demand creates a direct link between the global market and U.S. public finances.

Every new dollar token is backed by reserves, and the primary instrument — at least for Circle and Tether — is short-term U.S. Treasuries (T-bills). The larger the stablecoin issuance, the more U.S. debt issuers must buy. Washington thus gains a new, steady source of demand for its bonds, independent of traditional investors and even capable of smoothing market swings.

Against this backdrop, a logical question arises: if stablecoins are becoming a global channel for dollarization and simultaneously influencing demand for U.S. debt, might U.S. authorities seek full control over them?

Ownership or Oversight? Why a Clampdown Beats a Takeover

Publicly, the idea of U.S. government nationalization of stablecoins has barely surfaced. A user known as The Unhedged Capitalist floated a similar notion in September 2022, but more in the context of Ethereum.

In his blog, he discussed some countries’ plans to launch CBDCs, pointing to user privacy issues and policymakers’ limited grasp of the technology.

“USDC — whether backed by reserves or unicorn dust — is battle-tested tech. Why would the government spend years building its own CBDC and another year or two testing it (if they can even build such a thing) when they could just nationalize what already exists?” he asked.

He further speculated that the government’s target could be the entire Ethereum ecosystem. The U.S. Treasury, he suggested, might label Vitalik Buterin’s project and its stablecoins a “systemic threat to the United States and the sovereignty of the dollar.” Such claims do surface in various forms: Tether has been called a “money launderer’s dream,” and in January 2024 UN experts said USDT had become a popular tool among fraudsters.

“When Treasury seizes Ethereum, it won’t just control staking providers — it will bring stablecoin issuers to heel. They’ll force USDC, USDT, PAX USD, BUSD and the rest to allow redemptions only on ‘Treasury Ethereum.’ […] The craziest thing about my theory is just how easy it would be for Treasury to pull this off,” he wrote.

Such hypotheses haven’t gained mainstream traction. Experts surveyed by ForkLog lean toward the state pursuing (and already pursuing) regulation rather than outright takeovers.

Andrey Tugarin, founder of law firm GMT Legal, noted that current requirements for stablecoin issuers are being designed so that they are independent companies that, in effect, channel funds into U.S. government debt.

“From this standpoint, the practicality of nationalization looks low,” he said.

Ignat Likunov, founder of Cartesius legal agency, also called nationalization unlikely. In his view, the U.S. government has chosen a different strategy — establishing strict regulatory boundaries that achieve key policy goals without buying private companies.

He pointed out that the GENIUS Act contains no provisions on nationalization; instead, it sets clear federal operating rules for issuers.

“Moreover, Congress separately barred the Fed from issuing a state digital currency, underscoring a private-sector model under government oversight,” he noted.

Tugarin and Likunov agree that, under existing norms, there’s little rationale to nationalize the sector. According to Tugarin, if authorities wanted to centralize all control, the conversation would be about a CBDC.

“In this case, the state is leaving the technology to corporations, while obliging them to support public debt by holding a required portion of reserves in short-term Treasuries,” Tugarin said.

Likunov believes measures in the GENIUS Act effectively turn private companies into conduits of monetary and debt policy without changing ownership. In the new regime, Tether and Circle’s future looks like further adaptation to regulatory demands.

“Both companies will remain independent players, but their core business models will be tightly regulated to serve national interests — making them de facto ‘semi-public’ by function. As for structural demand for U.S. debt, stablecoins have already become a significant source. […] By decade’s end, the stablecoin market could reach $3.7 trillion, creating trillions in additional demand for Treasuries and helping reduce debt-service costs,” he emphasized.

Ani Aslanyan, founder of the Telegram channel “All about blockchain, the brain and WEB 3.0 in Russia and the world,” took an even firmer stance: direct nationalization of issuers is extremely unrealistic. In the U.S., such steps are reserved for emergencies tied to national security or systemic risk and require special legislation.

“The GENIUS Act lets issuers operate under OCC or state oversight with a focus on transparency and stability, without the need for government ownership. […] That preserves private-sector innovation, minimizes budget risks, and avoids legal battles,” Aslanyan said.

She believes that under the new framework, Tether and Circle will remain independent but with enhanced oversight — more “regulated” and akin to financial institutions.

Web3 researcher Vladimir Menaskop considers nationalization of stablecoin issuers conceivable — but adds that if realized, it would signal Washington had “definitively lost the economic war with China.”

“Nationalization has happened in U.S. history, but each time it meant abandoning foundational principles. The ‘railroad wars,’ ‘trade wars,’ and other tensions push the U.S. toward this scenario, though it’s possible rather than inevitable,” he stressed.

He argues there is a logic to nationalizing stablecoin issuers:

“First, issuers hedge by buying government debt — which is literally debt — and then that debt gets wiped out via nationalization. The U.S. gets liquidity but doesn’t retire its debt: a double saving.”

At the same time, Menaskop doubts Tether and Circle can be called non-state entities today: they hold massive dollar assets and Treasuries — a form of indirect control — while USDC’s issuer is directly tied to the jurisdiction.

Still, nationalization seems an ill-suited option. For the industry and the TradFi players connected to it, a state takeover of major issuers would trigger intense backlash and criticism. “Domestication” via regulation looks more realistic — and aligns with the new administration’s initiatives as it differentiates itself from the last.

The emerging regulatory perimeter has effectively brought stablecoins into the U.S. legal and financial system. Companies remain private, but their key decisions — providing or limiting services across countries, freezing addresses, structuring reserves — will be fully dictated by rules set in Washington.

In return, the U.S. gets a steady source of demand for Treasuries and a way to cement the dollar’s global leadership in the digital era. For the rest of the world, stablecoins will remain a convenient settlement tool — but increasingly a new form of dependence on U.S. financial policy. The real question isn’t how likely nationalization of Tether or Circle is, but how deeply the U.S. will steer this infrastructure — and what that will mean for the global economy.