Similar readings from Germany showed annual CPI growth of 2.6% and a monthly decline of 0.5%. Inflation risks in the region remain largely predictable and contained, so the European Central Bank (ECB) is not considering additional easing for now, although deteriorating economic prospects could still push the regulator toward further stimulus. On Monday, Germany released upbeat industrial output data: October production increased from 1.1% to 1.8% m/m versus expectations of –0.4%, while the annual rate improved from –1.4% to 0.8%.

Meanwhile, U.S. investors and FX traders remain focused on the outcome of the Federal Reserve’s two-day meeting. As expected, the Fed cut the key rate by 25 basis points to 3.75% and also upgraded its economic projections. The Fed now sees 2026 GDP growth at 2.3% versus 1.8% previously, while inflation is projected at 2.5% in 2025 and 2.4% in 2026.

GBP/USD

The pound is gaining against the dollar and is on track to finish the week moderately higher: yesterday, GBP/USD managed to print fresh local highs last seen on October 20. However, as Thursday’s U.S. session opened, the dollar recovered most of its earlier losses, even though the labor-market data were mixed: initial jobless claims for the week ending December 5 rose from 192.0K to 236.0K versus expectations of 220.0K, while continuing claims fell from 1.937M to 1.838M (markets had looked for 1.950M).

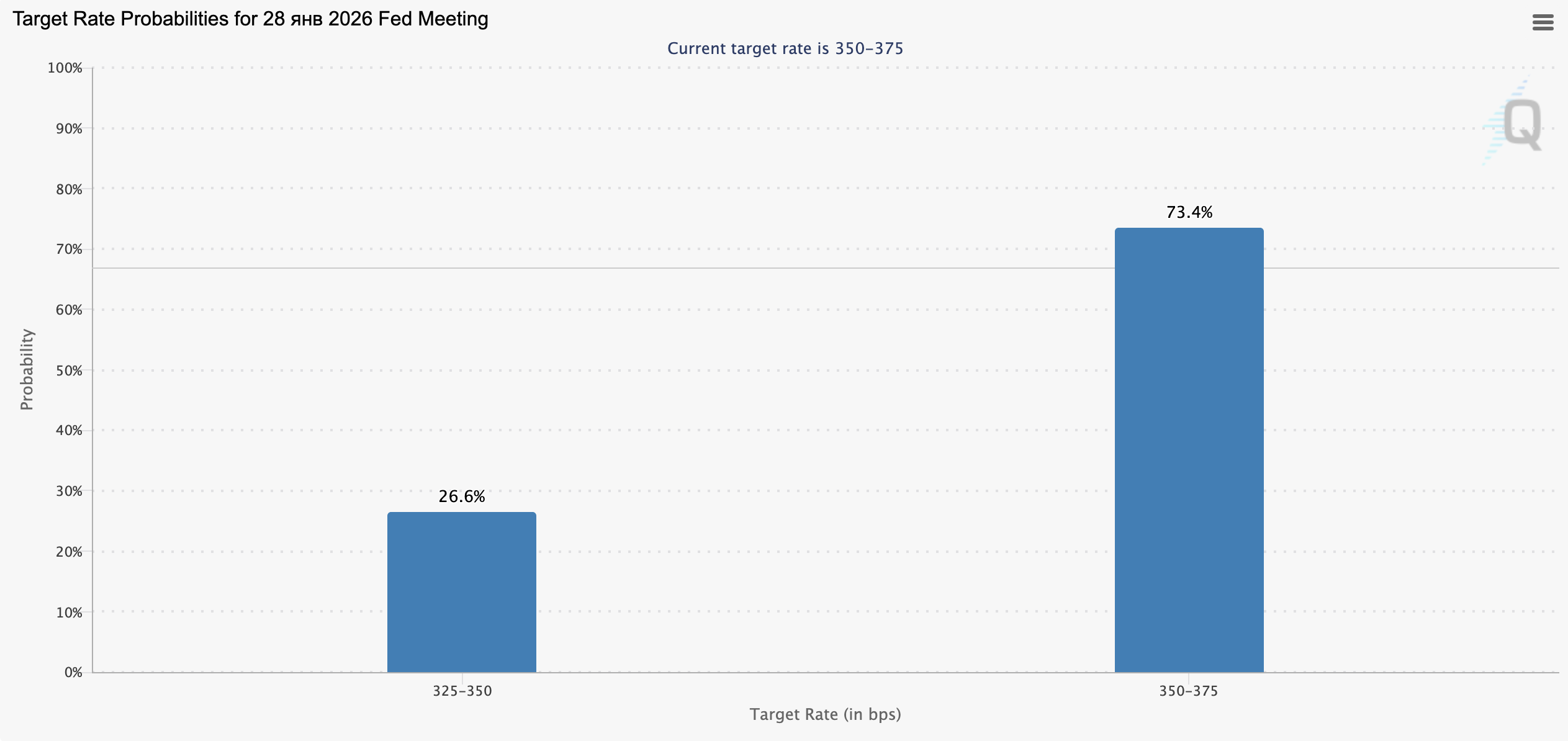

Next week, the market will receive the November report from the U.S. Department of Labor, which may reshape expectations for the Fed’s next steps. At the moment, most analysts assume policymakers will pause the dovish cycle in January. In the UK, investors and FX traders are focused on October GDP and industrial output figures: the economy contracted by 0.1% versus forecasts for +0.1%, services activity posted zero growth after +0.2% in the prior quarter (vs a 0.1% forecast), while industrial production accelerated to +1.1% m/m, beating expectations of 0.7%; on an annual basis it fell only 0.8% after –2.5% previously. The pound reacted neutrally, but analysts may increase the probability of Bank of England easing at the December 18 meeting. Also today at 11:30 (GMT+2), the BoE will publish consumer inflation expectations; the prior 12-month projection stood at 3.6%.

NZD/USD

The New Zealand dollar is trading mixed against the U.S. dollar, consolidating near 0.5800. Into the end of the week, investors are watching November retail spending data: electronic card transactions rose from 0.8% to 1.6% y/y and from 0.2% to 1.2% m/m. In addition, the Business NZ manufacturing activity index printed at 51.4 points.

Market participants are also assessing the Fed decision released on Wednesday: as expected, the regulator cut rates by 25 basis points to 3.75% (a three-year low) and slightly improved its own projections for GDP growth and inflation.

Chair Jerome Powell, in his accompanying remarks, emphasized labor-market challenges—cooling activity and rising unemployment—while inflation took a back seat this time, slightly boosting market confidence that additional easing in January cannot be ruled out. At present, officials still pencil in only one rate cut in 2026, while investors are pricing in two. Yesterday’s jobless claims data were also noted: initial claims for the week ending December 5 climbed from 192.0K to 236.0K versus 220.0K expected, while continuing claims fell from 1.937M to 1.838M versus 1.950M expected.

USD/JPY

The U.S. dollar is recovering against the yen after two consecutive sessions of declines: USD/JPY is testing 155.80 for an upside breakout as traders weigh Japanese macro data. Industrial output in October rose from 1.5% to 1.6% y/y and from 1.4% to 1.5% m/m. Capacity utilization also increased notably, up 3.3% after a 2.5% gain in September. The data provided only limited support to the yen, as they are unlikely to be sufficient to justify further Bank of Japan tightening—an outcome also opposed by Prime Minister Sanae Takaichi. Meanwhile, the dollar is gradually strengthening after the Fed cut rates by 25 basis points to 3.75% and kept its near-term rate projections unchanged, while upgrading expectations for growth and inflation dynamics.

XAU/USD

Gold (XAU/USD) is consolidating near 4280.00 and close to the local highs from October 21. The metal is set to finish the week higher, although the U.S. dollar has also been recovering after the Fed’s two-day meeting, where rates were reduced by 25 basis points to 3.75% and growth/inflation forecasts were revised upward. The Fed now sees 2026 GDP growth at 2.3% versus 1.8% previously, while inflation is projected at 2.5% in 2025 and 2.4% in 2026.

Jerome Powell noted that labor-market activity is showing signs of cooling, affecting both household assessments and corporate sentiment, while CPI has retreated from the mid-2022 peak but remains above the long-term 2.0% target.

Yesterday’s jobless claims data were mixed: initial claims for the week ending December 5 rose from 192.0K to 236.0K versus 220.0K expected, while continuing claims dropped from 1.937M to 1.838M (markets had expected 1.950M). Meanwhile, safe-haven demand for gold remains steady as geopolitical tensions persist. U.S. President Donald Trump has not yet managed to move meaningfully closer to a settlement of the Russia–Ukraine conflict; moreover, a potential peace deal could further complicate relations between the U.S. and the EU.