President Emmanuel Macron reappointed Sébastien Lecornu as Prime Minister after he had resigned last week due to a political crisis and lack of parliamentary support. Now, the head of government has managed to finalize the formation of the Cabinet and secure backing from the Socialist Party by promising to suspend the controversial pension reform bill at least until the 2027 presidential election. The new coalition helped Lecornu avoid votes of no confidence initiated by both left- and right-wing parties. In the first vote, launched by “Unsubmissive France,” 271 deputies voted “for,” falling short of the required 289, and in the second, only 144 supported the motion. Nevertheless, public trust remains low: according to the latest data, about 64% of French citizens disapprove of Lecornu’s appointment.

The government now faces difficult budget debates for 2026, which could further strain the political climate, as the plan includes major cuts to social spending. At 11:00 (GMT+2), forex investors will focus on September inflation data in the eurozone: forecasts suggest that the core annual consumer price index will remain at 2.3%, and the broader CPI at 2.2%. Meanwhile, the U.S. dollar remains under pressure due to the ongoing government shutdown in the United States: employees of many federal agencies have been furloughed, and President Donald Trump’s administration announced mass layoffs in several departments. The National Nuclear Security Administration (NNSA), which oversees the country’s nuclear arsenal, recently reported serious disruptions.

GBP/USD

The British pound is strengthening in the GBP/USD pair, heading for a strong weekly close and updating its local highs from October 7. Traders today are watching Bank of England officials’ speeches for hints about potential monetary easing, especially as the U.S. Federal Reserve also prepares to cut borrowing costs. The Fed’s next meeting is set for October 29, and current projections largely point to a 25 basis-point rate cut.

The Bank of England’s policy meeting is scheduled for December 18, and markets remain uncertain about its decision amid persistently high inflation in the UK, which could accelerate in Q4 due to worsening global market conditions. British industry continues to suffer from EU tariffs, while investors are concerned about the renewed U.S.–China trade tensions and reciprocal tariffs. UK macroeconomic data released yesterday showed GDP growth of 0.1% in August after –0.1% a month earlier.

Over the next three months, experts from the National Institute of Economic and Social Research (NIESR) expect growth to accelerate to 0.3%. Meanwhile, industrial production fell by 0.7% year-on-year in August after –0.1% previously (vs forecast –0.6%), while monthly output increased by 0.4% (forecast 0.2%). U.S. data released Thursday showed a sharp decline in the Philadelphia Fed manufacturing index from 23.2 to –12.8 in October, while analysts expected 10.0 points.

AUD/USD

The Australian dollar is showing slight weakness in the AUD/USD pair, holding near 0.6470. The pressure continues after the disappointing September labor market report released yesterday. Seasonally adjusted unemployment rose from 4.3% to 4.5%, the highest since November 2021. Total employment increased by 14.9K after a decline of 11.8K the previous month (forecast +20.5K). Full-time employment rose by 8.7K, part-time by 6.3K, while the labor force participation rate edged up from 66.9% to 67.0% (forecast 66.8%).

The AUD/USD pair remains under pressure due to renewed trade tensions between China and the United States. Yesterday, President Donald Trump said Washington is in a “trade war” with Beijing. On October 11, Trump announced new 100% tariffs on imports starting November 1, adding to the existing 30% rate, while China maintains 10% tariffs on U.S. goods. His rhetoric reflects concerns about China’s dominance in rare earth exports, which make up 70% of global supply. Additionally, mutual “port sanctions” introduced on October 14 threaten to disrupt maritime trade, particularly in oil products. Investors also remain focused on the U.S. government shutdown, now in its third week, with no progress in Congress and yet another delay in passing a temporary funding bill, marking the ninth postponement this week.

USD/JPY

The U.S. dollar is losing ground in the USD/JPY pair, testing 149.80 to the downside. The instrument is set to close the week lower, updating its October 6 lows. Demand for the yen has increased amid rising U.S.–China trade tensions. President Trump announced new 100% tariffs on Chinese goods starting November 1, adding to the existing 30% rate, in response to Beijing’s export restrictions on rare earth metals. Trump also floated the idea of increasing tariffs to 300% and using the proceeds to fund military and humanitarian aid for Ukraine. However, Japan’s political uncertainty limits further yen gains. Last week, Sanae Takaichi became the new leader of the Liberal Democratic Party (LDP). If she becomes Prime Minister, analysts expect the Bank of Japan to slow the pace of monetary tightening or even abandon its hawkish stance. Elections are scheduled for October 21, but could be postponed after the Komeito Party withdrew from the coalition.

XAU/USD

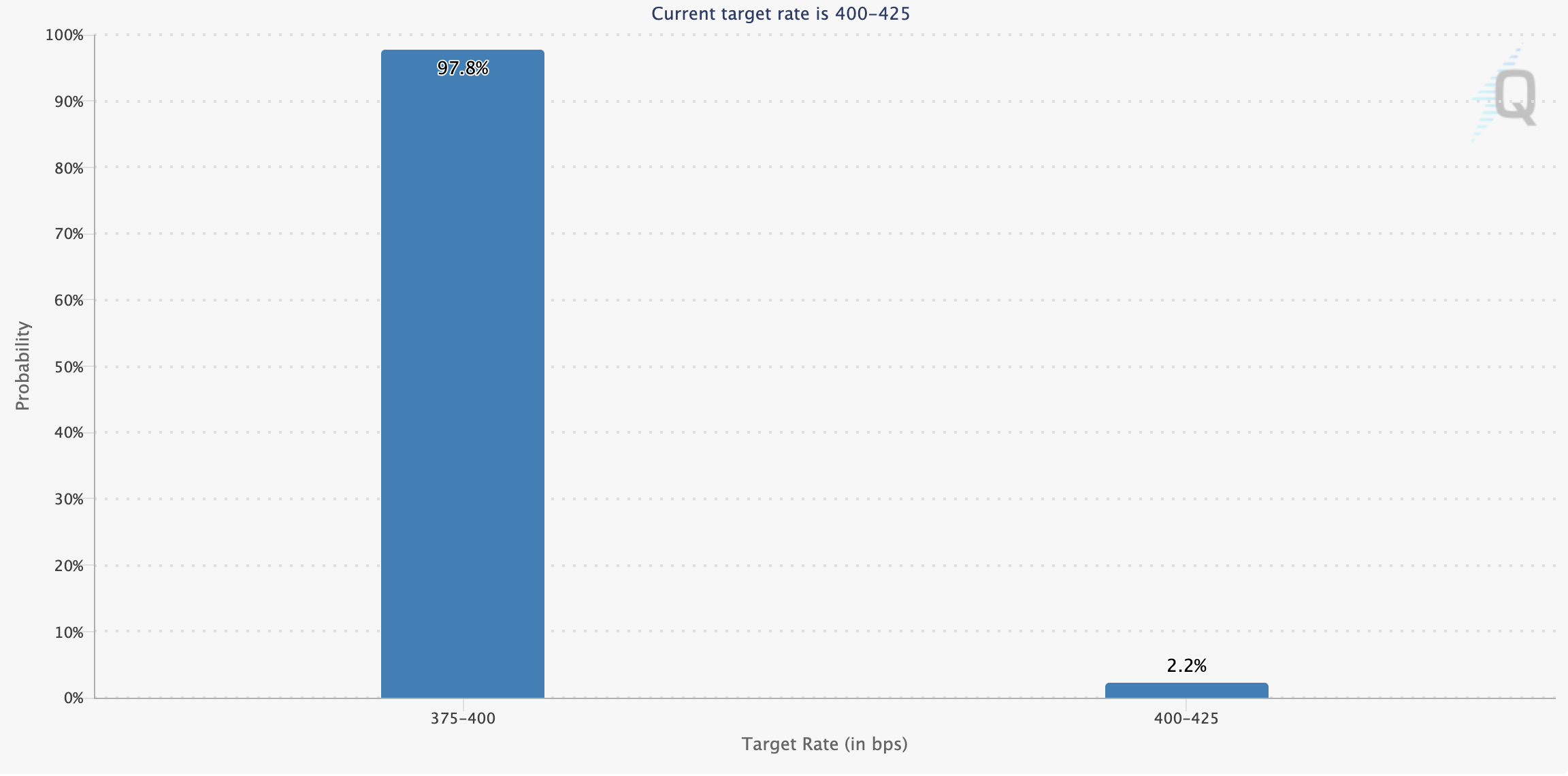

The XAU/USD pair continues to rise steadily, extending its short-term uptrend and testing the 4360.00 level to the upside, as demand for safe-haven gold remains high. This week’s rally was supported by expectations that the U.S. Federal Reserve will accelerate monetary easing. According to the CME Group’s FedWatch Tool, the Fed is expected to cut rates by 25 basis points at the October meeting, with another reduction likely in December. Meanwhile, the U.S. dollar remains under pressure amid the ongoing government shutdown.

Additionally, deteriorating U.S.–China trade relations continue to drive demand for gold. Earlier, President Trump reiterated his intention to impose additional 100% tariffs on Chinese goods starting November 1, aiming to pressure Beijing after it restricted exports of rare earth metals. China supplies about 70% of the world’s total rare earth exports, which are increasingly in demand amid rising defense budgets and Trump’s protectionist stance toward the semiconductor industry.