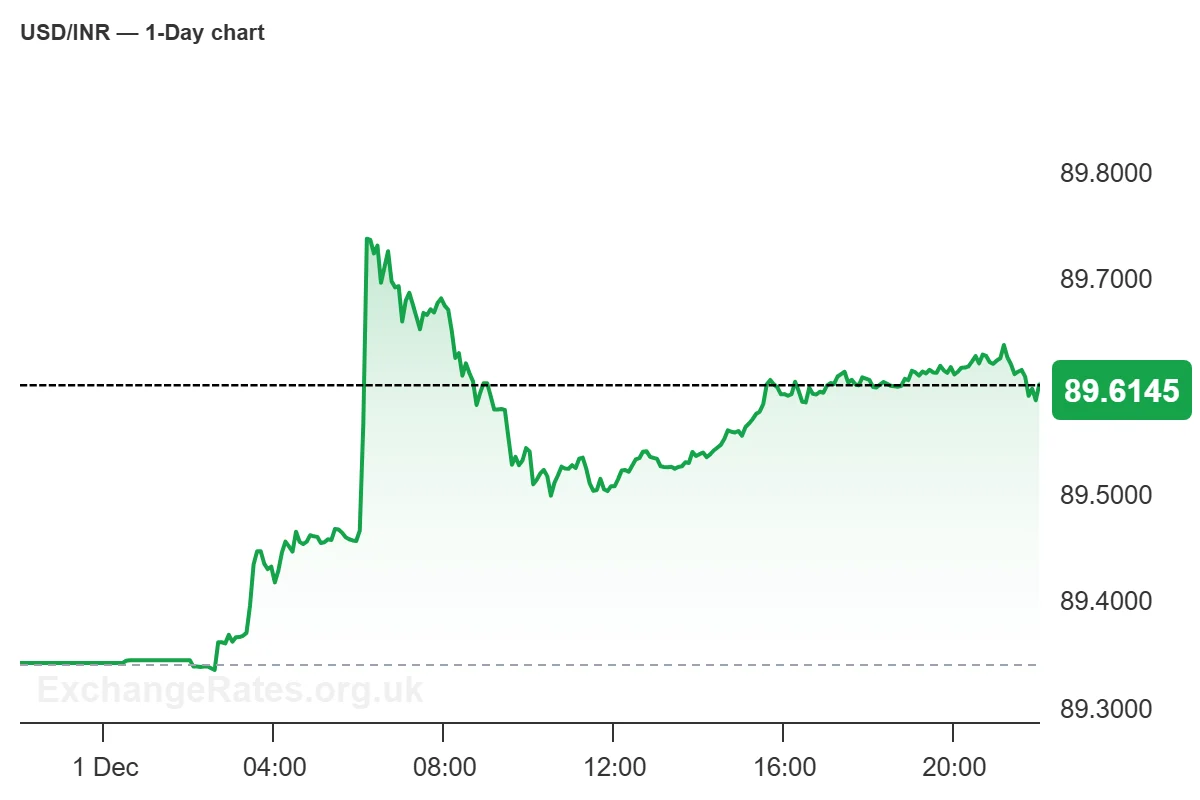

Last week’s move from 89.15 to 89.35 highlighted a market adjusting to a new FX environment in which the Reserve Bank of India allows wider day-to-day fluctuations instead of tightly smoothing every swing.

According to Goldman Sachs, this shift aligns with the IMF’s latest Article IV review, which reclassified India’s de facto exchange-rate regime from “stabilized” to “crawl-like.”

Analysts stress that this does not signal a loss of control. Rather, it reflects an RBI more willing to tolerate moderate volatility while still stepping in to calm extreme moves.

Goldman maintains a more constructive view on India’s fundamentals than the currency’s recent behavior might suggest. The country’s 8.2% GDP growth in Q3 and record-low October inflation indicate a significantly stronger macro backdrop.

Analysts expect this strength to appear more clearly in Indian equities than in the exchange rate. Undervaluation, solid growth momentum and subdued inflation make the equity market attractive after a challenging year.

As for the rupee itself, Goldman describes the outlook as “crawling, not falling.” The bank expects the RBI to rebuild FX reserves on USD/INR dips, keeping the currency within a broad range rather than in a sustained directional trend.

In this view, a meaningful appreciation of the rupee is unlikely — but a prolonged depreciation is also not the base case as long as India’s macro fundamentals remain stable.