Analysts expect the European regulator to leave monetary policy parameters unchanged but may hint at potential future easing amid continued economic slowdown in the bloc. Particular attention is on Germany and France: France is currently engulfed in protests tied to its political crisis and the change of prime minister. The new head of government will need to reach consensus on the 2026 budget. Former prime minister François Bayrou had previously pushed for sharp spending cuts, especially in social programs, which drew heavy criticism from right-wing parties. The new prime minister, appointed by Emmanuel Macron, will be Defense Minister Sébastien Lecornu, who is expected to favor higher taxes for corporations and wealthy citizens. Meanwhile, at 14:30 (GMT+2) the U.S. will publish inflation data: the core Consumer Price Index (CPI) for August is forecast at 0.3% month-on-month and 3.1% year-on-year, while the broader CPI is expected to rise from 0.2% to 0.3% and from 2.7% to 2.9%, respectively. At 20:00 (GMT+2), the U.S. Treasury will release its August budget report, projected to show a modest deficit decline from –$291.0 billion to –$281.0 billion. Already available to traders are yesterday’s U.S. Producer Price Index (PPI) figures: the core PPI slowed in August from 3.4% to 2.8% YoY against expectations of 3.5%, while the broader index fell from 3.1% to 2.6% (forecast: 3.3%); on a monthly basis, PPI dropped 0.1% after a 0.7% increase the prior month (consensus: +0.3%).

GBP/USD

The pound is weakening against the U.S. dollar in the GBP/USD pair during the morning session, extending a mild corrective pullback formed on Tuesday after retreating from local highs of August 14. Quotes are testing 1.3520 to the downside as the market awaits the U.S. inflation release at 14:30 (GMT+2). Expectations point to an acceleration of annual inflation from 2.7% to 2.9%, which could influence Federal Reserve officials ahead of the September 17 meeting. Investors are also digesting yesterday’s U.S. PPI data, which reflected a less concerning picture than initially feared: the annual PPI slowed from 3.1% to 2.6% (vs. forecasts of 3.3%), while the monthly index fell 0.1% after a 0.7% July increase. The core PPI excluding food and energy also dropped from 3.4% to 2.8% (forecast: 3.5%). Tomorrow at 08:00 (GMT+2), the U.K. will release July GDP and industrial production data. Analysts expect monthly GDP growth to slow from 0.4% to 0.1%, while industrial production is forecast to accelerate from 0.2% to 1.1%. The Bank of England has previously signaled its willingness to maintain accommodative policy despite inflation targets not yet being achieved.

AUD/USD

The Australian dollar is showing slight declines in the AUD/USD pair during the Asian session, unwinding short-term gains and retreating from November 2024 highs. The instrument is testing the 0.6600 level to the downside as investors await the U.S. inflation release at 14:30 (GMT+2). Forecasts suggest CPI could accelerate toward 3.0%, while the core index is expected at 3.1%. However, recent PPI data prompted analysts to revise expectations: the annual PPI slowed unexpectedly from 3.1% to 2.6% (vs. forecasts of 3.3%), while the monthly reading dropped 0.1% after July’s +0.7%. The core PPI slipped from 3.4% to 2.8% (forecast: 3.5%). Additionally, data from China weighed on AUD yesterday: CPI in August fell 0.4% YoY after flat growth in July (vs. forecast –0.2%) and slowed from 0.4% to 0.0% MoM, while PPI improved from –3.6% to –2.9%.

USD/JPY

During the Asian session, USD/JPY quotes are testing 147.70 to the upside as traders digest Japanese inflation data. The Producer Price Index (PPI) rose from 2.5% to 2.7% YoY in August, while MoM the index fell 0.2% after a +0.2% increase in July (forecast: –0.1%). Market sentiment was also supported by the BSI Large Manufacturing Conditions Index, which rebounded from –4.8 points to 3.8 in Q3 (forecast: –3.3). U.S. CPI figures due at 14:30 (GMT+2) are in focus today: core CPI is expected at 0.3% MoM and 3.1% YoY, while the broader index should rise from 0.2% to 0.3% MoM and from 2.7% to 2.9% YoY. At 20:00 (GMT+2), the U.S. Treasury budget report is due, with a projected deficit decline from –$291.0 billion to –$281.0 billion. Traders already have yesterday’s U.S. PPI data, which showed the core slowed from 3.4% to 2.8% YoY (forecast: 3.5%), while the broader index fell from 3.1% to 2.6% (forecast: 3.3%); MoM the index dropped 0.1% after July’s +0.7% (forecast: +0.3%). In Japan, political tensions remain high as Prime Minister Shigeru Ishiba prepares to resign, triggering a leadership contest within the Liberal Democratic Party next month ahead of new government formation.

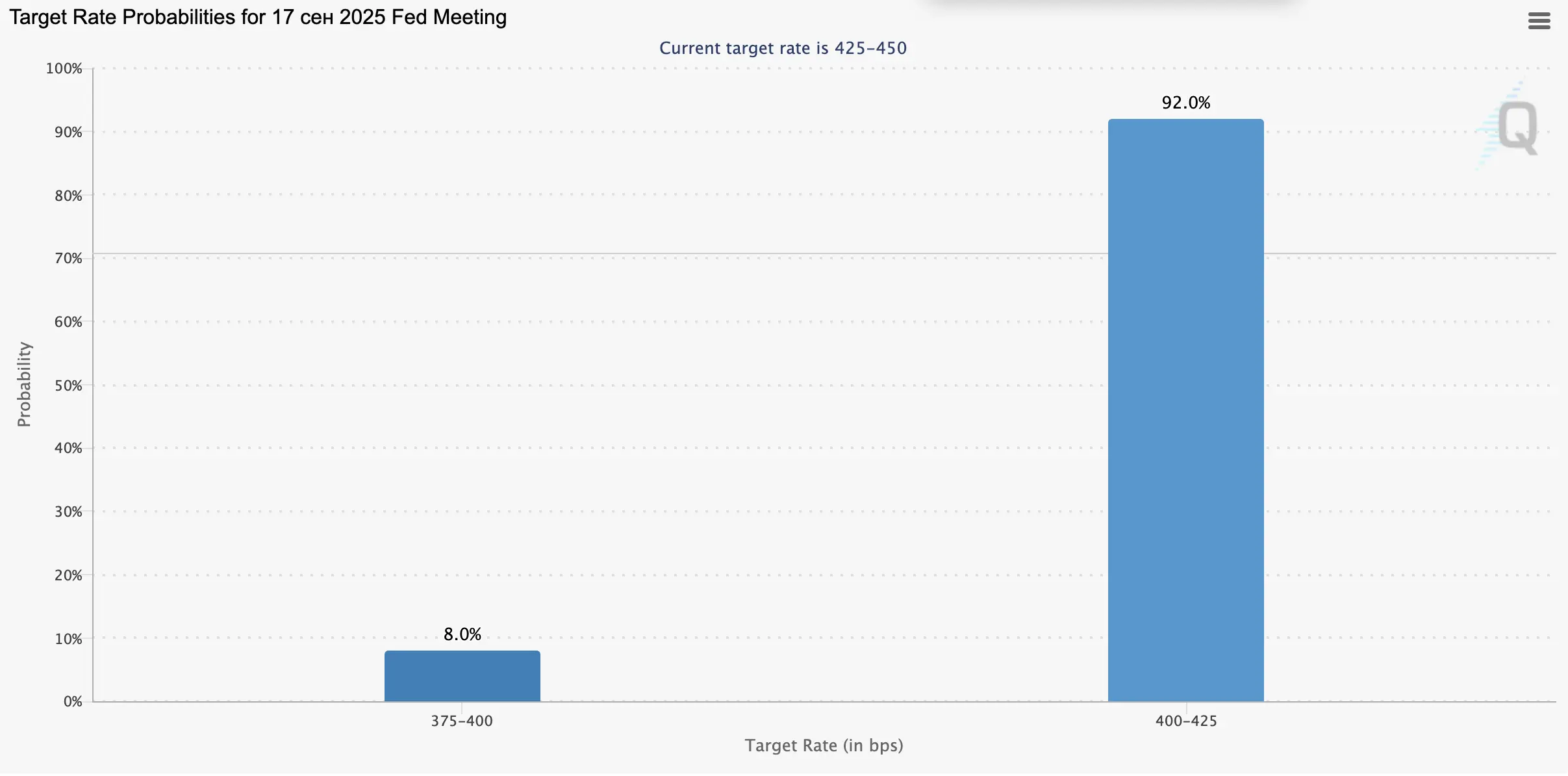

XAU/USD

The XAU/USD pair is edging lower again during the morning session, testing 3630.00 to the downside as safe-haven demand strengthens on expectations of a Federal Reserve rate cut at the September 17 meeting. According to the CME Group FedWatch Tool, there is over a 90% chance of a –25 basis point adjustment, while about 8% of analysts still see potential for a deeper –50 basis point cut.

Additional support for a dovish stance comes from Tuesday’s U.S. data: annual PPI slowed from 3.1% to 2.6% (forecast: 3.3%), monthly PPI fell 0.1% after +0.7% (forecast: +0.3%), and core PPI eased from 3.4% to 2.8% (forecast: 3.5%). At 14:30 (GMT+2) today, CPI data will be released, with forecasts for a modest acceleration, though expectations risk being missed again. Another bearish factor for the U.S. economy is the Labor Department’s revised annual employment report through March 2025, showing 911,000 fewer jobs created than initially estimated. This highlights further labor market cooling and increases pressure on the Fed. On Friday at 16:00 (GMT+2), markets will also watch for updated University of Michigan consumer inflation expectations and consumer sentiment, with forecasts pointing to a slight dip from 58.2 to 58.0.