Some analysts believe incoming macroeconomic data will support a policy adjustment in December, while others still point to insufficient labor market data. The September report was mixed: although it showed a noticeably stronger increase in nonfarm payrolls, it also reflected a rise in the unemployment rate from 4.3% to 4.4%. The October report will not be published due to the government shutdown, which prevented the collection of the necessary statistical data, and the November figures will only appear after the central bank’s December meeting. Another signal in favor of a more dovish stance came from September producer inflation data: the core annual Producer Price Index (excluding food and energy) fell from 2.9% to 2.6% versus a 2.7% forecast, while the monthly figure accelerated from −0.1% to 0.1% compared to expected 0.3%. The broader indicator matched preliminary estimates at 2.7% year-on-year and 0.3% month-on-month.

Investors and forex traders also focused on weak retail sales data: in September, monthly growth reached only 0.2%, slowing after a 0.6% increase the previous month, while experts had expected 0.4%. On an annual basis, the figure fell from 5.0% to 4.3%. Weak sales reflect declining domestic demand, as more Americans shy away from expensive purchases due to rising living costs. In addition, the record shutdown affected the data, as many federal employees were forced into unpaid leave and therefore cut spending. European investors turned their attention to German data: year-on-year GDP in the third quarter rose by 0.3%, while quarterly growth remained flat. Weak domestic demand, trade barriers, and slowing industrial activity have led to stagnation in the German economy. Nevertheless, the government still expects 1.3% growth in 2026 amid increased public spending on defense and infrastructure upgrades.

GBP/USD

The pound is strengthening against the U.S. dollar, developing a strong bullish impulse formed late last week. The pair is testing the 1.3190 level for a breakout, as market participants await U.S. macroeconomic data and closely monitor the peace process between Russia and Ukraine. Last week, U.S. President Donald Trump presented a peace plan and called on both sides to compromise.

UK investors are assessing retail sales data released at the end of last week: the annual figure for October fell from 1.0% to 0.2% against a 1.5% forecast, while the monthly figure dropped from 0.7% to −1.1%, versus expectations of 0.0%. The GfK consumer confidence index in November declined from −17.0 to −19.0 points, compared to a preliminary estimate of −18.0. This suggests that the national economy is slowing, which is a signal for the Bank of England to further ease monetary policy. At the same time, the regulator remains concerned about rising price pressures, as consumer inflation is still significantly above analysts’ average forecasts. Today at 15:30 (GMT+2), the U.S. will release durable goods orders for September, but their impact on the market may be limited. Nevertheless, the broader measure of capital goods orders is expected to slow from 2.8% to 0.3%. Along with weak retail sales data seen earlier, this may strengthen expectations of a U.S. Fed rate cut at the December meeting.

NZD/USD

The New Zealand dollar is strengthening against the U.S. dollar, testing the 0.5690 level for a breakout and reaching local highs since November 4. The focus of investors is on the decision of the Reserve Bank of New Zealand (RBNZ), which, as expected, cut the key interest rate by 25 basis points to 2.25%. Last month, officials reduced the rate by 50 basis points. The decision was not unanimous and the regulator remains cautious in choosing the direction of monetary policy. Nevertheless, current conditions allow for further easing to stimulate the fragile recovery of the national economy.

RBNZ forecasts still suggest that inflation will return to the midpoint of the 2.0% target range by mid-2026. Today at 23:45 (GMT+2), data on retail sales for the third quarter will be released, with the indicator expected to accelerate from 0.5% to 0.6%, providing further confirmation of a gradual recovery in domestic demand. In the U.S., investors will pay attention to durable goods orders at 15:30 (GMT+2): forecasts suggest a significant slowdown from 2.9% to 0.3% in September, while orders excluding defense are expected to remain unchanged at 1.9%. In addition, recent retail sales data showed the annual index falling from 5.0% to 4.3% and the monthly figure slipping from 0.6% to 0.2%, versus forecasts of 4.6–4.7% and 0.4%, respectively. The retail sales control group lost 0.1% after a 0.6% increase the previous month, while analysts had expected a 0.3% rise.

USD/JPY

The U.S. dollar is extending a corrective decline against the Japanese yen, pulling back from early-year record highs reached late last week. The pair is testing the 156.00 level for a downside breakout, as traders prepare for the release of U.S. durable goods orders at 15:30 (GMT+2). Forecasts suggest the indicator will slow significantly from 2.9% to 0.3% in September, while orders excluding defense are expected to hold steady at 1.9%. In addition, recent retail sales data showed the annual index falling from 5.0% to 4.3% and the monthly figure slipping from 0.6% to 0.2%, versus forecasts of 4.6–4.7% and 0.4%, respectively.

The retail sales control group declined by 0.1% after a 0.6% increase the previous month, while analysts had expected a 0.3% rise. Investors will also focus on the U.S. Federal Reserve’s monthly economic report, the so-called Beige Book, which will be released today at 21:00 (GMT+2) and reflect business activity across various U.S. regions. The data is expected to be weak, which would further reinforce expectations of additional monetary easing in December. In Japan, data on the coincident and leading indices was released earlier today: the leading index rose from 108.0 to 108.6 in September, while the coincident index remained at 114.6. On Friday at 01:30 (GMT+2), key inflation data for the Tokyo region will be released, with the annual CPI expected to slow from 2.8% to 2.7% in November. In addition, October data on the labor market, retail sales, and industrial production will be published. Investors and forex traders fear that weak macroeconomic data could strengthen expectations that the Bank of Japan will keep its monetary policy unchanged. This view is also supported by the spending plan of Prime Minister Sanae Takaichi, who is known for her dovish stance. Further weakening of the yen also raises concerns, as it could trigger new currency interventions by the Ministry of Finance and its head, Satsuki Katayama.

XAU/USD

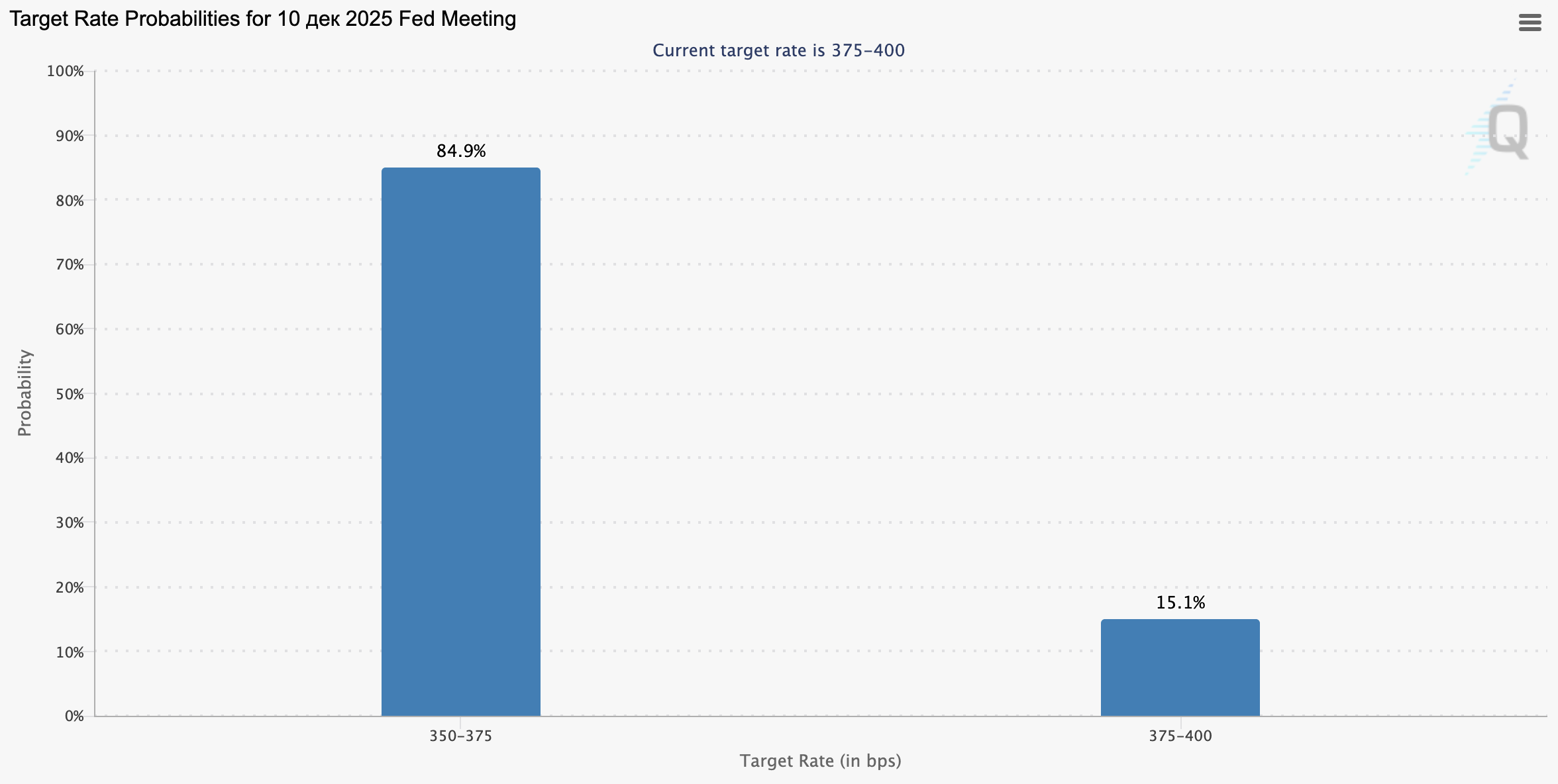

XAU/USD is rising in value, testing the 4160.00 level for a bullish breakout and reaching local highs since November 14. Demand for gold is supported by expectations that the U.S. Federal Reserve will ease monetary policy at its December meeting. According to the CME Group FedWatch Tool, around 85.0% of analysts expect an interest rate cut of 25 basis points to 3.75%.

It is also possible that Fed Chair Jerome Powell adopts a more dovish position, given the latest macroeconomic data, particularly retail sales: in September, monthly growth reached only 0.2% after a 0.6% increase, compared to a 0.4% forecast, while the annual figure fell from 5.0% to 4.3%. At the same time, investors are monitoring news about a potential peaceful resolution of the conflict between Russia and Ukraine. It is assumed that the parties are moving fairly quickly toward reaching a deal, which was presented by U.S. President Donald Trump last week.