At the same time, the regulator’s options are currently very limited: another rate cut is possible, but it is unlikely to produce the desired effect amid structural crises and a sharp shift in global market conditions. So far, EU leaders are trying to stimulate the economy through increased defense spending and infrastructure projects, but this may only have a temporary impact against the backdrop of rising living costs and shrinking social guarantees.

Data released on Monday from Germany showed a decline in the IFO Business Climate Index in November from 88.4 to 88.1 points, against a forecast of 88.5, as well as a drop in the Economic Expectations Index from 91.6 to 90.6 points, while the Current Assessment Indicator strengthened from 85.3 to 85.6 points. Today at 15:30 (GMT+2), the focus of U.S. investors and forex traders will be on producer inflation data for September: forecasts suggest a slight acceleration in annual growth from 2.6% to 2.7%, and on a monthly basis from –0.1% to 0.3%. At the same time, the core indicator excluding food and energy could ease from 2.8% to 2.7%. An acceleration in producer inflation could put pressure on the Fed regarding a potential rate cut at the December meeting.

GBP/USD

The pound is trading with near-zero dynamics in the GBP/USD pair, holding near the 1.3100 level, as market activity remains subdued while participants await new catalysts. In particular, today at 15:30 (GMT+2), U.S. retail sales data for September will be published, which may reflect a slowdown from 0.6% to 0.4%, while sales excluding autos are likely to fall from 0.7% to 0.4%, pointing to a sharp slowdown in consumer activity and indirectly signaling a weakening of inflationary risks. As a result, this could lead to a revision of the Fed’s interest rate at the December meeting.

In addition, producer inflation data will be released today: according to forecasts, the annual indicator will rise from 2.6% to 2.8%, while the core index excluding food and energy is expected to slow from 2.8% to 2.7%. Tomorrow at 21:00 (GMT+2), the Federal Reserve’s monthly economic report, the Beige Book, will be released, reflecting business activity across various regions of the country. It should be noted that the report may be incomplete, as statistical data for October is still likely insufficient. UK investors and forex traders are also guided by business activity data published last Friday: the November services index from S&P Global fell from 52.3 to 50.5 points versus a forecast of 52.1, while the manufacturing index rose from 49.7 to 50.2 points, compared to expectations of 49.3.

NZD/USD

The New Zealand dollar is losing value in the NZD/USD pair, testing the 0.5595 level for an upside breakout, supported by forecasts for the development of the national economy, which continues to recover after the recession. At the same time, in the second quarter GDP showed a downward trend and, adjusted for inflation, its real volume was even lower than in 2022. However, domestic demand remains stable, allowing the Reserve Bank of New Zealand to adjust monetary policy if necessary, as the potential for reducing borrowing costs has not yet been exhausted. The regulator’s next meeting will take place tomorrow at 03:00 (GMT+2): according to preliminary estimates, officials will cut the interest rate by 25 basis points to 2.25% and signal possible further changes in the future. Forecasts suggest the rate will lose another 50 basis points in the first half of 2026.

For now, traders have at their disposal New Zealand’s foreign trade data released late last week: exports in October increased from 5.78 billion NZD to 6.50 billion NZD, while imports grew from 7.17 billion NZD to 8.04 billion NZD. As a result, the trade deficit adjusted from –2.39 billion NZD to –2.28 billion NZD. Meanwhile, the U.S. dollar is weakening ahead of the December Fed meeting, which could result in an additional rate cut. Officials currently have the September labor market report available, while November data will be released after the decision is made. Signals in favor of possible monetary easing also came from the University of Michigan’s inflation expectations data published on Friday: one-year expectations fell in November from 4.7% to 4.5%, and five-year expectations from 3.6% to 3.4%. The U.S. dollar was also pressured by the S&P Global manufacturing PMI, which slowed in November from 52.5 to 51.9 points, while analysts expected 52.0.

USD/JPY

The U.S. dollar is showing mixed dynamics in the USD/JPY pair, consolidating near the 156.80 mark and the record highs from mid-January, which were updated last week. Market participants are not rushing to open new positions ahead of U.S. macroeconomic data releases. At 15:30 (GMT+2), producer price index data for September will be published, which may adjust from 2.6% to 2.7%, while the core figure may slow from 2.8% to 2.7%. The retail sales control group for September is expected to ease from 0.7% to 0.3%, while the broader measure may decline from 0.6% to 0.4%. These figures could indicate further easing of inflationary risks in the country, strengthening expectations of monetary easing by the Fed at the December meeting.

In Japan, November inflation data for the Tokyo region will be released on Friday at 01:30 (GMT+2): the annual consumer price index is expected to slow from 2.8% to 2.7%, which obviously will not support the yen, as it will strengthen expectations that the Bank of Japan will keep its monetary policy unchanged. In addition, data on unemployment, retail sales, and industrial production for October will be published, with production potentially falling from 2.6% to –0.6% amid deteriorating global market conditions due to higher import tariffs initiated by the U.S. and rapidly increasing competition from China.

XAU/USD

The XAU/USD pair is rising in value, developing a strong bullish impulse formed at the beginning of the current week. The instrument is once again attempting to consolidate above the 4150.00 level, updating local highs from November 14. Market activity remains subdued as investors await U.S. macroeconomic data that could clarify the prospects for monetary easing by the Fed. Today at 15:30 (GMT+2), the focus will be on September producer inflation data: forecasts suggest a slight acceleration in annual growth from 2.6% to 2.7% and on a monthly basis from –0.1% to 0.3%.

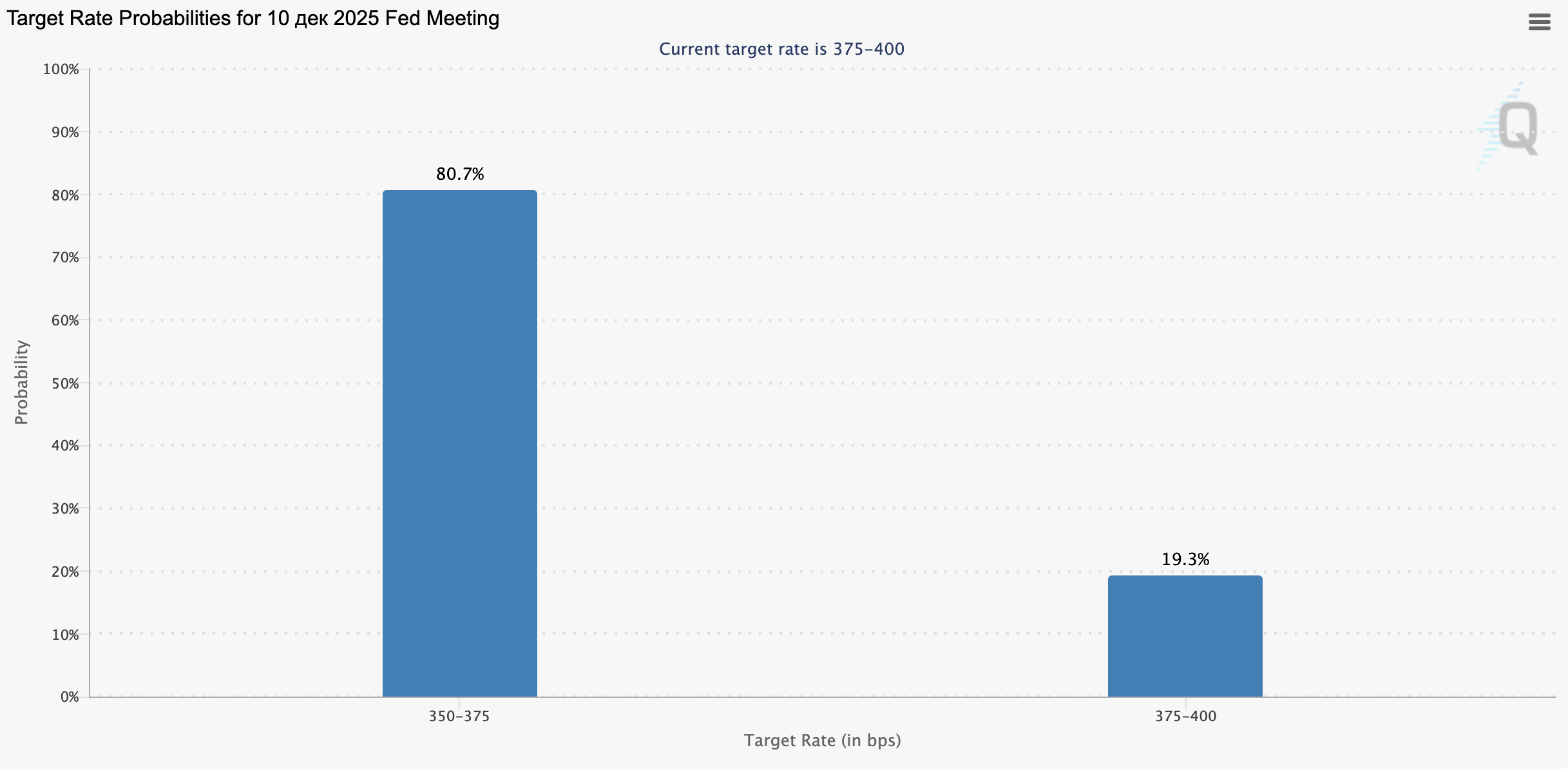

At the same time, the core producer price index excluding food and energy in September may adjust from 2.8% to 2.7%. Higher figures could increase pressure on the regulator regarding a possible rate cut at the December meeting. Currently, according to the CME Group FedWatch Tool, about 60.0% of analysts expect officials not to rush into a dovish stance. Tomorrow at 21:00 (GMT+2), the Fed’s Beige Book — its monthly economic report — will be released, reflecting business activity in various regions of the country.

It should be noted that the report may be incomplete, since October statistical data is still likely insufficient. Safe-haven gold is also being supported by expectations of lower borrowing costs from the Reserve Bank of New Zealand (RBNZ), whose meeting will take place tomorrow at 03:00 (GMT+2).