Today at 11:00 (GMT+2), the focus of forex traders and investors will be on the Eurozone’s October consumer credit data, with forecasts suggesting the indicator will remain at 2.6%. At 12:00 (GMT+2), data on business sentiment will be released: the services sentiment index in November is expected to rise from 4.0 to 4.4 points, while the overall economic sentiment index is projected to increase from 96.8 to 97.0 points. On Friday at 09:00 (GMT+2), market participants will analyse Germany’s October retail sales data, where annual growth is expected to add another 0.2%. In addition, labour market data will be released at 10:55 (GMT+2), with the number of unemployed expected to rise by 5.0 thousand after a decline of 1.0 thousand in the previous month, while the unemployment rate is forecast to remain unchanged at 6.3%. On the same day, at 09:45 (GMT+2), November inflation data from France will be published, where analysts expect the CPI to rise from 0.8% to 1.0%, followed by German inflation data at 15:00 (GMT+2), which are projected to increase from 2.3% to 2.4%. These figures are unlikely to become a signal for the European Central Bank to revise its current monetary policy.

GBP/USD

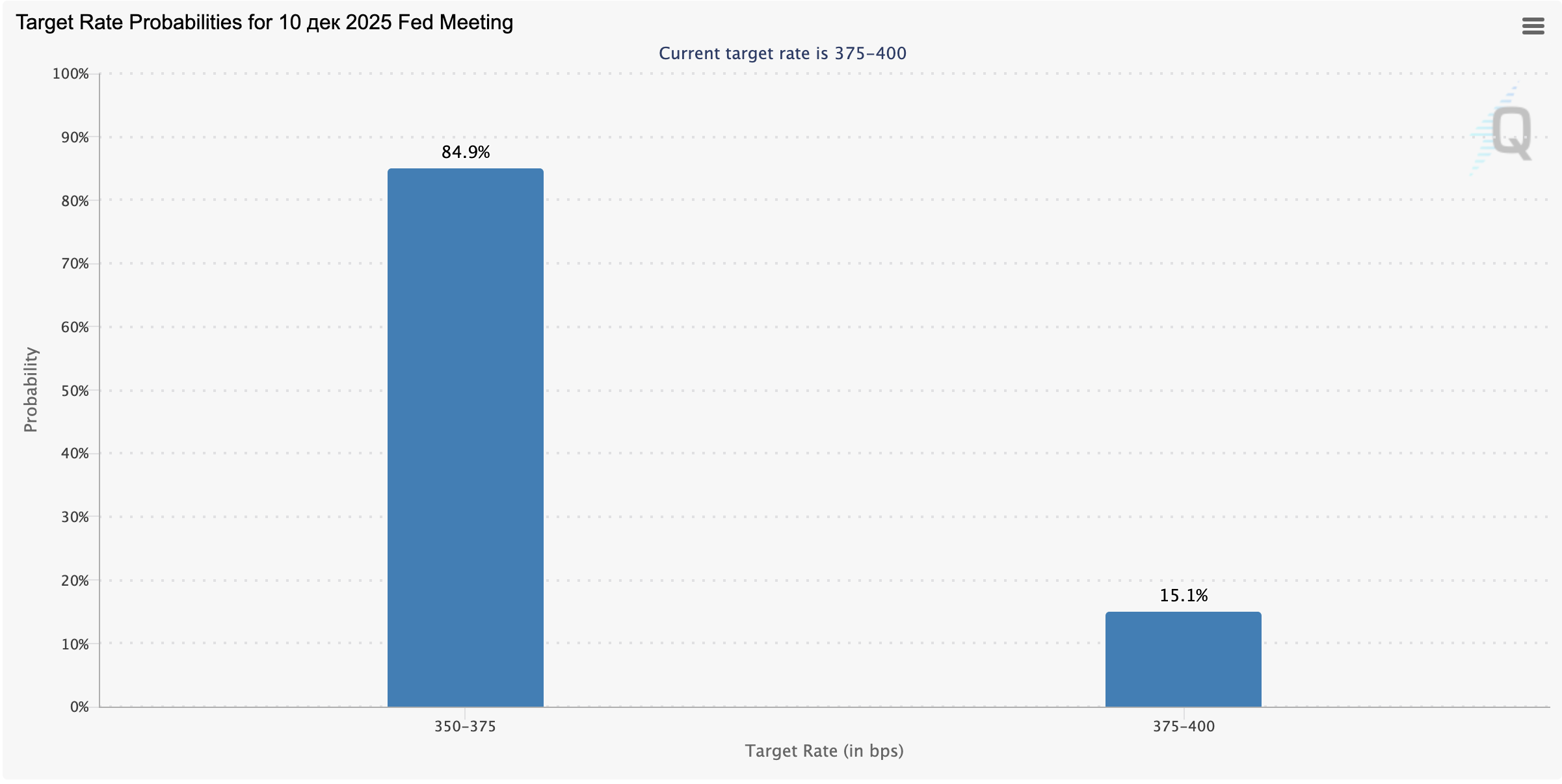

The pound is strengthening against the US dollar, extending a solid upward move and updating local highs from October 29. The pair is testing the 1.3260 level to the upside, while overall market activity remains subdued due to the Thanksgiving holiday in the United States. Meanwhile, the US dollar continues to feel pressure ahead of the Federal Reserve’s December meeting, where borrowing costs are expected to be reduced by 25 basis points. According to the CME Group FedWatch Tool, the probability of such a move now stands at 85.0%, compared to just 50.0% at the beginning of last week.

Further support for a dovish shift came from September producer price data released on Tuesday. The core annual PPI (excluding food and energy) slowed from 2.9% to 2.6%, versus expectations of 2.7%, while the monthly figure accelerated to 0.1% after -0.1%, although forecasts had pointed to 0.3%. The broader indicator met analysts’ expectations, coming in at 2.7% year-on-year and 0.3% month-on-month. Investors also took note of weak retail sales dynamics: in September, monthly growth slowed to 0.2% from 0.6% in the previous month, against preliminary estimates of 0.4%. On an annual basis, the figure declined from 5.0% to 4.3%, reflecting weakening domestic demand as more Americans cut back on spending amid higher living costs.

AUD/USD

The Australian dollar is also gaining ground against the US dollar, developing a fairly strong short-term bullish trend. The pair posted its strongest rise in recent weeks, reacting to inflation data which showed that the annual consumer price index in October accelerated from 3.6% to 3.8%, while the monthly figure slowed from 0.5% to 0.0%. Elevated annual inflation reinforces the concerns of the Reserve Bank of Australia regarding any further easing of monetary policy. At the moment, only 6.0% of analysts expect borrowing costs to be reduced at the next meeting.

At the same time, expectations of an interest rate adjustment by the Federal Reserve have continued to strengthen, driven by mixed developments in the US labour market, in particular the rise in the unemployment rate to 4.4%. In September, however, the US economy added 119.0 thousand non-farm jobs, more than twice the preliminary estimates. Like the RBA, the Fed remains cautious about renewed inflation risks, but incoming data still point to a generally stable economic environment.

According to the CME Group FedWatch Tool, the probability that borrowing costs will be cut by 25 basis points in December is now 85.0%, up from 50.0% previously. US durable goods orders data released yesterday also delivered mixed signals: the broad measure of capital goods orders slowed sharply from 3.0% to 0.5%, versus forecasts of 0.3%, while the indicator excluding defence dropped from 1.9% to 0.1%. Meanwhile, initial jobless claims for the week ended November 21 declined from 222.0 thousand to 216.0 thousand, compared to expectations of 225.0 thousand, while continuing claims increased slightly from 1.953 million to 1.960 million, approaching the psychologically important 2.0 million mark.

USD/JPY

The US dollar is losing ground against the Japanese yen, once again testing the 156.00 level to the downside. The greenback remains under pressure as expectations grow for further monetary easing by the Federal Reserve at its December 10 meeting. According to the CME Group FedWatch Tool, the probability of a 25 basis point rate cut by year-end currently stands at 85.0%. However, due to the lack of a full set of macroeconomic data amid the government shutdown, the outlook for further policy moves remains uncertain.

Market participants are also closely monitoring President Donald Trump’s stance toward the Federal Reserve. Previously, the White House administration actively criticised the dovish approach of Fed Chair Jerome Powell, and investors are now awaiting the announcement of a candidate to replace him. US Treasury Secretary Scott Bessent told CNBC that Trump is likely to reveal his choice before the Christmas holidays. The current favourite is White House National Economic Council Director Kevin Hassett, who is known for his more dovish views. Meanwhile, on Friday at 01:30 (GMT+2), investors will turn their attention to November inflation data for the Tokyo region, which could significantly influence the Bank of Japan’s plans regarding any potential rate hikes. Forecasts suggest that the annual CPI may slow from 2.8% to 2.7%.

XAU/USD

The XAU/USD pair is moving sideways, hovering around the 4155.00 level, as market activity remains low due to the Thanksgiving holiday in the United States. Traders continue to assess expectations surrounding a potential rate cut by the Federal Reserve at its December meeting. According to the CME Group FedWatch Tool, the probability of a 25 basis point rate reduction by year-end is currently estimated at 85.0%. A more aggressive cut is not entirely ruled out, but at this stage it appears less likely.

During an upcoming press conference, Fed Chair Jerome Powell is expected to once again attempt to reassure the markets, which are pricing in a continuation of the monetary easing cycle. The focus of policymakers and forex traders will remain on incoming macroeconomic data. However, November labour market figures will only be released after the Fed meeting and therefore will not influence the upcoming decision on monetary policy.

For now, traders are relying on producer inflation data released on Tuesday: the core PPI slowed from 2.9% to 2.6% against expectations of 2.7%, while the broader indicator came in at 2.7%. Weak retail sales data also weighed on the US dollar, as the annual figure in September dropped from 5.0% to 4.3%, and the monthly figure slowed from 0.6% to 0.2%, compared to an expected 0.4% increase. At the same time, gold prices were slightly pressured by expectations that the United States may achieve a diplomatic resolution to the Russia–Ukraine conflict before the end of the year. The two sides are reportedly discussing a plan that could lead to a cessation of hostilities. On the eve, President Donald Trump stated that his special envoy, Steve Witkoff, is scheduled to meet with Russian President Vladimir Putin in Moscow as early as next week.