Yesterday’s macro data showed Germany’s ZEW current conditions index falling in October from –76.4 to –80.0 (consensus –75.0), while the economic sentiment index rose from 37.3 to 39.3 (vs. 40.5 expected). For the euro area as a whole, the ZEW economic sentiment index slipped from 26.1 to 22.7 (vs. 30.2 expected). In the U.S., NFIB small business optimism for September eased from 100.8 to 98.8 (vs. 100.5 preliminary).

Also in focus was Fed Chair Jerome Powell’s speech, in which he acknowledged that current macro readings suggest economic activity is not fully aligned with the Fed’s projections. He did not directly address the federal government shutdown, noting instead the lack of a complete data set for full analysis. Even so, the remarks strengthened market conviction that borrowing costs will be cut at least twice more before year-end. Meanwhile, the euro drew some support from signs of progress in France’s political stalemate.

Recall that President Emmanuel Macron reappointed Sébastien Lecornu as prime minister. Lecornu finalized the cabinet and held its first meeting yesterday with the president present. Macron again urged lawmakers to rally around the country’s economic challenges and hinted he could dissolve the National Assembly if another no-confidence vote is brought. Lecornu emphasized that the controversial 2023 pension reform (raising the retirement age to 64)—a trigger for mass protests—will be paused until January 2028. The government will instead aim to reduce the budget deficit by raising taxes on wealthier citizens. Socialist group leader Boris Vallaud supported revisiting pension reform but warned that budget decisions will still be difficult, with his party seeking further compromises and concessions.

GBP/USD

The pound is flat in GBP/USD, holding near yesterday’s close. The pair initially fell on a weak labor report but later recovered most losses. Employment growth slowed in August from 232.0k to 91.0k, September jobless claims rose from 17.4k to 25.8k, and the unemployment rate ticked up to 4.8% from 4.7% (vs. forecasts for no change). This adds pressure on the Bank of England to continue cutting borrowing costs. MPC member Alan Taylor even raised the prospect of a “harder landing” than previously expected, suggesting the BoE may need to ease more quickly without waiting for inflation to hit the 2.0% target. Additional headwinds could come from new tariff measures not only from the U.S., but also the EU and China. Notably, EU officials recently doubled steel tariffs to 50.0% and cut import quotas by 47.0% versus 2024—negative for the UK’s steel industry given ~80.0% of its exports go to the EU, while other markets may be crowded by cheaper Chinese imports. Meanwhile, the U.S. dollar remains pressured by rising expectations of imminent Fed rate cuts and the ongoing shutdown. The Republican administration has begun seeking alternative funding sources for key federal programs.

AUD/USD

The Australian dollar is firmer in AUD/USD, continuing a short-term range and testing 0.6515 to the upside as traders parse China data. September CPI fell 0.3% y/y after –0.4% (consensus –0.1%) and rose 0.1% m/m after 0.0% (vs. 0.2% expected). PPI deflation eased to –2.3% y/y from –2.9%. Yesterday, Australian NAB surveys supported the AUD: business confidence rose from 4 to 7, and business conditions from 7 to 8. The pair also gained after September RBA minutes showed the cash rate held at 3.60%, with the Bank in no rush to ease further. Officials noted the economy appears to be recovering faster than expected, though inflation and external risks remain. In particular, they flagged the White House’s aggressive tariff stance and renewed U.S.–China trade tensions. The U.S. president earlier signaled 100.0% tariffs in response to China’s rare-earth export limits, and “port fees” came into force yesterday, lifting seaborne freight charges: China’s levy is $56 per ton now, rising to $89 from April 17 next year. U.S. data also weighed on the dollar, with September NFIB optimism dipping to 98.8 from 100.8 (vs. 100.5 preliminary).

USD/JPY

The U.S. dollar is sliding in USD/JPY, testing 152.00 to the downside and printing new lows since October 7, pressured by political uncertainty as the shutdown enters its third week. The Senate has now rejected the Republican temporary funding bill for the eighth time: 49 against, 45 in favor, short of the 60 votes needed. The administration is seeking alternative funding to maintain key federal programs. Yen sentiment, however, is capped by domestic data: industrial production fell 1.6% y/y in August after –1.3% and 1.5% m/m after –1.2%; capacity utilization dropped from –1.1% to –2.3%. Markets are also watching LDP leadership developments after Sanae Takaichi’s victory. A parliamentary vote for prime minister is likely on October 21. Concern lingers over the Komieto party’s exit from its long-standing coalition with the LDP, after disagreements on tighter rules for political donations from businesses and civic groups.

XAU/USD

XAU/USD is advancing, extending a short- and medium-term bullish trend that keeps driving fresh records. The pair is approaching 4200.00 while the U.S. shutdown persists, forcing the administration to seek new funding sources for federal projects and agencies. Markets also expect further Fed rate cuts.

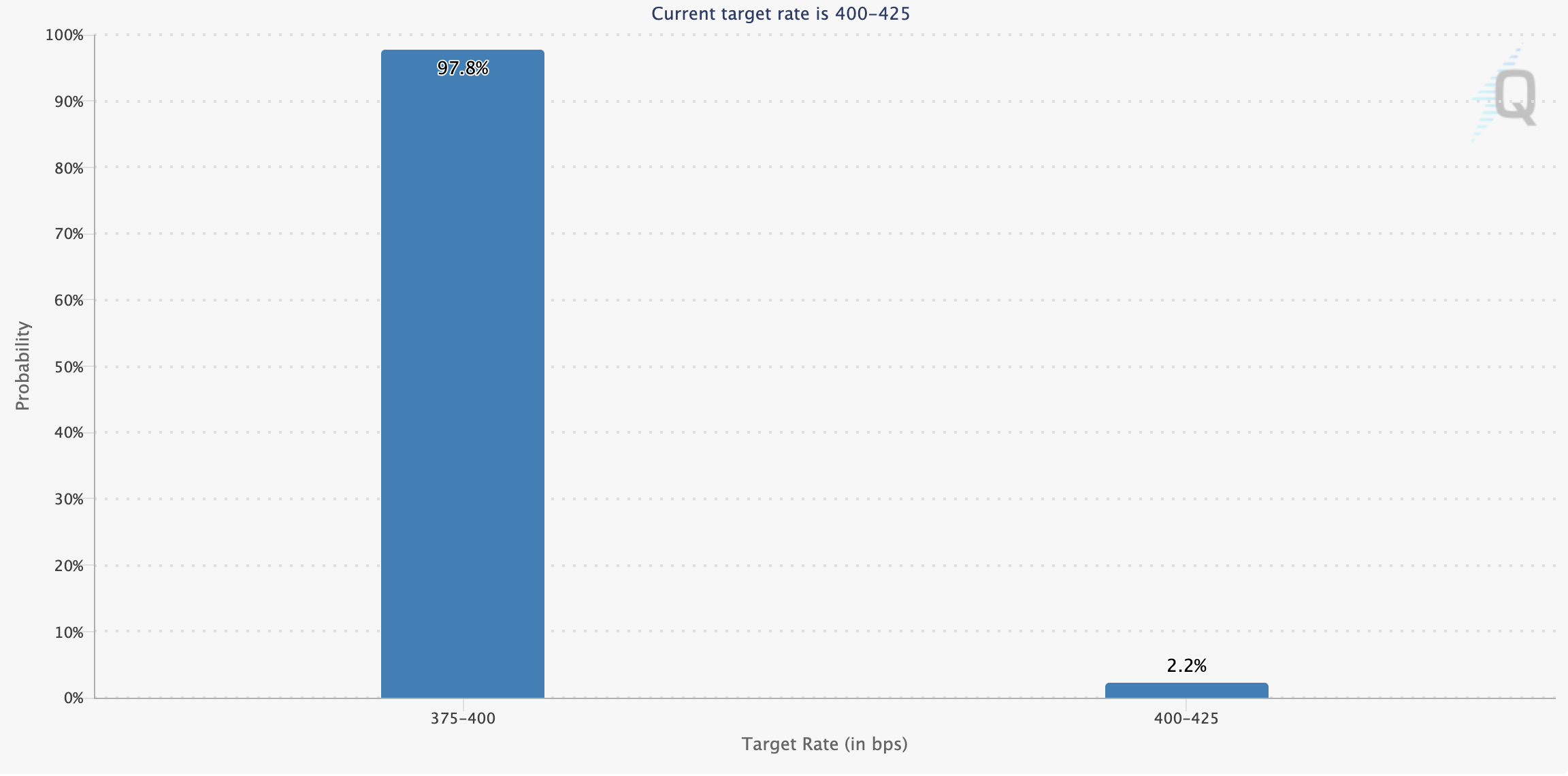

According to CME Group’s FedWatch Tool, the probability of an October rate cut is currently above 95.0%. Additional easing in December is also seen as likely. Gold demand is further supported by escalating U.S.–China trade tensions. The U.S. president has floated 100.0% tariffs in response to China’s rare-earth export restrictions, and reciprocal “port fees” that raised ocean-freight charges came into effect yesterday. China’s levy is $56 per ton now, potentially rising to $89 per ton from April 17 next year.