Pressure on the pair came from Germany’s September IFO business climate survey: the expectations index fell from 91.6 to 89.7 points (vs. forecast 92.0), the business climate index slid from 89.0 to 87.7 (vs. 89.3), while the current conditions index eased from 86.4 to 85.7 points (forecast 86.5).

These figures show that German businesses remain skeptical about large-scale infrastructure modernization programs and are not encouraged by higher defense spending. Adding to the uncertainty is the worsening global outlook, with U.S. President Donald Trump refusing to revise high import tariffs and the Russia–Ukraine conflict showing no diplomatic progress.

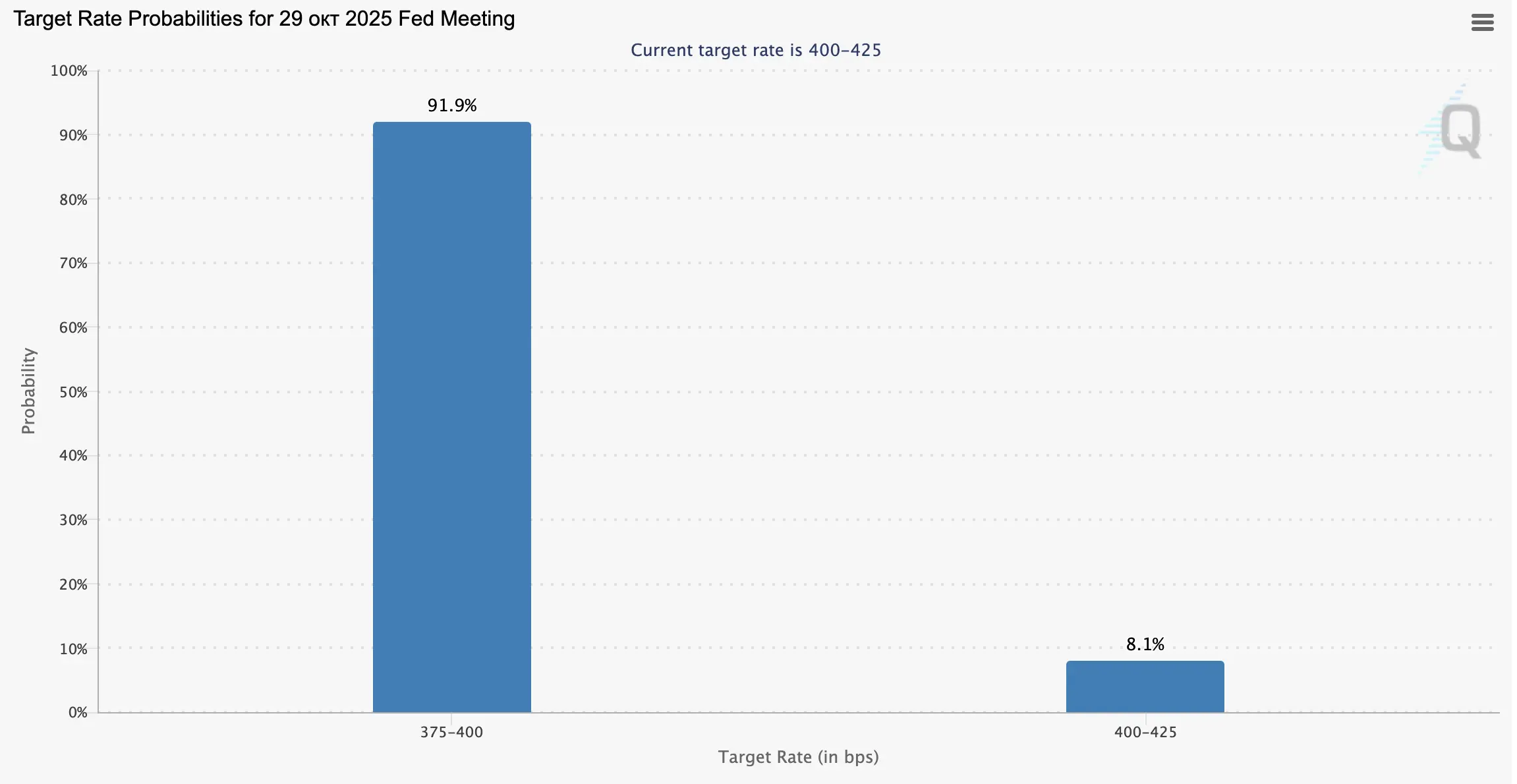

Meanwhile, the U.S. dollar is supported by comments from Fed Chair Jerome Powell, who spoke Tuesday at the Greater Providence Chamber of Commerce in Warwick, Rhode Island. He noted that the issue of further rate cuts remains open but warned that overly aggressive easing could accelerate inflation. The Fed will have to strike a fragile balance between rising prices and a cooling labor market. The latest U.S. jobs data disappointed, underscoring the limited resilience of the economy. At 14:30 (GMT+2) the U.S. will release August durable goods orders: forecasts point to a 0.5% decline after –2.8% previously, while core orders (ex-defense and aircraft) are expected to dip 0.1% after +1.1%.

GBP/USD

The pound is consolidating in GBP/USD during the morning session, slowing the short-term bearish trend. Yesterday the pair quickly reversed early-week gains as the dollar strengthened on reduced expectations of Fed easing after Powell’s cautious remarks. He rejected the idea of pre-set cuts this year, citing risks around both employment and inflation.

The dollar was further supported by strong U.S. new home sales data: the figure surged 20.5% in August after –1.8% a month earlier, rising to 0.800M vs. 0.664M (consensus 0.650M). Sterling, on the other hand, remains pressured by weak UK PMI data, highlighting economic fragility: the manufacturing PMI dropped from 47.0 to 46.2 in September, services eased from 54.2 to 51.9 (forecast 53.5), while the composite fell from 53.5 to 51.0. The Bank of England last week avoided another rate cut, wary of stubbornly high inflation above target.

AUD/USD

The Australian dollar is holding gains in AUD/USD during the Asian session, trading near its September 8 lows. Market activity remains subdued as traders await fresh catalysts. At 14:30 (GMT+2) the U.S. will release its revised Q2 GDP (expected unchanged at 3.3%), along with durable goods and jobless claims. Initial claims are seen rising slightly to 235K from 231K, with continuing claims at 1.93M vs. 1.92M prior.

Investors will also watch Fed speakers after Powell’s highly cautious remarks, stressing risks of inflation rebound. Meanwhile, Australian CPI surprised to the upside in August, accelerating from 2.8% to 3.0% (consensus 2.9%). This may constrain the RBA from aggressive monetary easing.

USD/JPY

The U.S. dollar is retreating in USD/JPY during Asian trade, testing 148.60 on the downside and pulling back from September 3 highs. Yesterday’s surge was fueled partly by Powell’s cautious tone on further U.S. easing. Last week the Fed cut rates by 25 bps to 4.25% and left the door open for one or two more cuts this year. Officials also upgraded U.S. growth forecasts for 2025–26. At 14:30 (GMT+2) traders await the revised Q2 GDP (prior +3.3%). In Japan, Tokyo CPI is due Friday at 01:30 (GMT+2): core inflation is expected to accelerate from 2.5% to 2.8%, reinforcing speculation of tighter BoJ policy. The Bank of Japan last week kept rates at 0.50%, likely avoiding extra volatility ahead of October’s prime minister elections.

XAU/USD

Gold is under pressure in XAU/USD, retreating from record highs and testing 3730.00 on the downside. The move reflects renewed dollar strength after Powell questioned the inevitability of further rate cuts this year. While this contrasts with updated Fed projections last week, it remains consistent with Powell’s cautious stance: for months he has resisted Trump’s calls for aggressive easing, citing the need for a balanced approach.

At this stage, the two key factors remain rising inflation and labor market cooling. Still, the long-term outlook for gold is intact: geopolitical risks and global uncertainty keep investors seeking safe-haven assets. Fed easing is still likely (unless inflation spikes), to be followed by other central banks, including the BoE. Today’s U.S. durable goods report (14:30 GMT+2) is expected to show a 0.5% decline after –2.8%, with core orders seen at –0.1% after +1.1%.