In recent months, industrial activity in the region has shown moderate improvement, supported by higher government defense spending and Germany’s infrastructure modernization programs. However, analysts remain skeptical that these initiatives will help restore the EU’s budget surplus, as the bloc continues to face competitive pressure from Chinese manufacturers — especially after the shift away from cheap Russian energy — along with trade restrictions introduced by US President Donald Trump.

Meanwhile, Friday’s inflation data from Germany showed annual CPI holding at 2.3%, while markets expected a mild uptick to 2.4%. On a monthly basis, CPI declined from 0.3% to –0.2% versus expectations of –0.3%. The harmonized consumer price index (HICP) rose from 2.3% to 2.6%, slightly above preliminary estimates of 2.4%. Traders also assessed German labor-market data for October: the number of unemployed rose by 1,000 after a similar decline the previous month, while economists had forecast a rise of 5,000. The unemployment rate remained unchanged at 6.3%.

In the US today, investor attention will turn to November business activity data from S&P Global at 16:45 (GMT+2) and from the ISM at 17:00 (GMT+2). Forecasts call for the S&P Global manufacturing PMI to stay at 51.9, while the ISM index may edge down from 48.7 to 48.6. At 15:00 (GMT+2), Federal Reserve Chair Jerome Powell is scheduled to speak, possibly attempting once again to calm markets that expect the Fed to cut rates at the December meeting.

GBP/USD

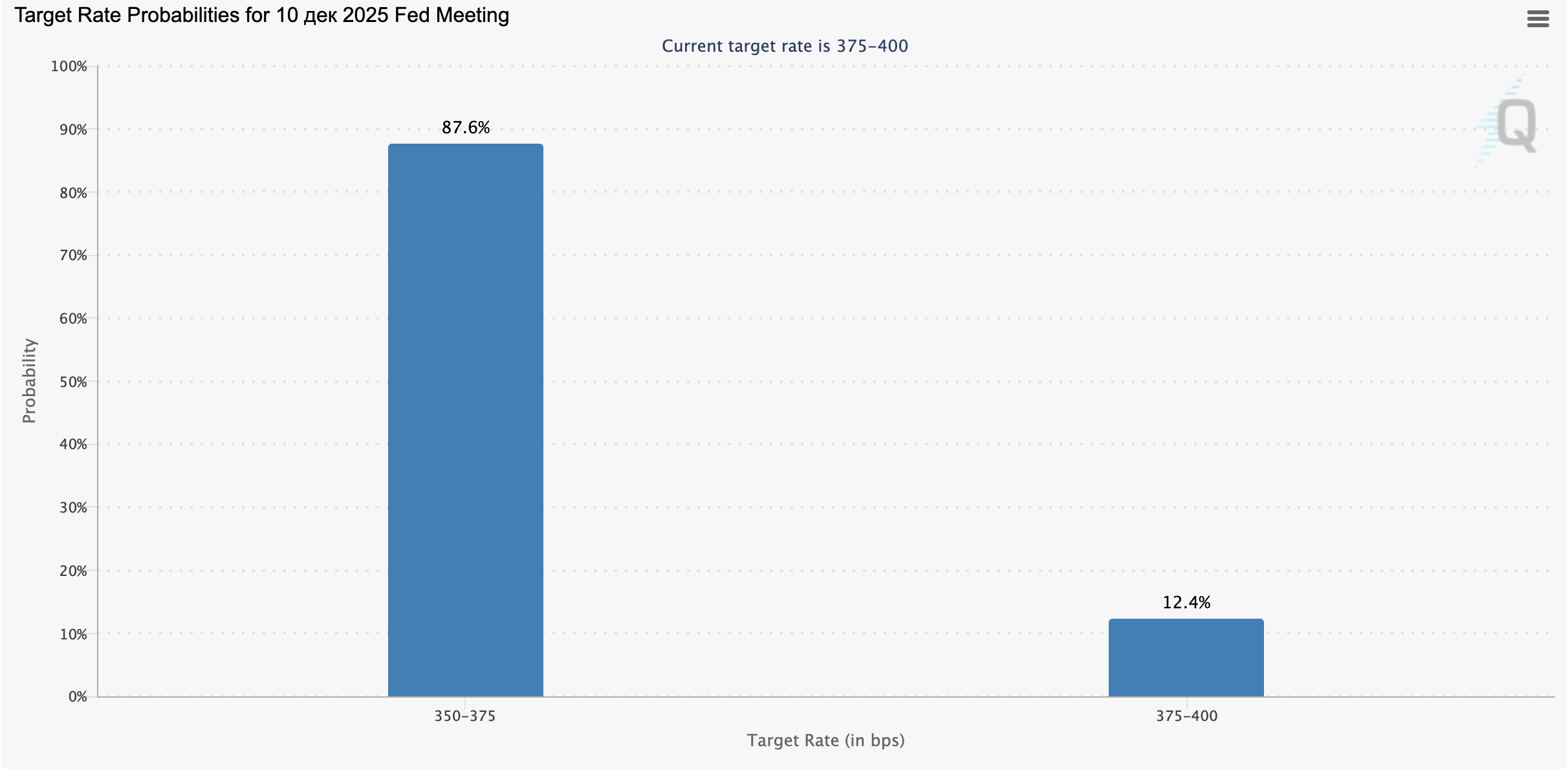

The British pound is declining against the US dollar, pulling back from the local highs of October 29 reached late last week. The pair is testing the 1.3220 level to the downside as traders wait for new catalysts. The US dollar remains under pressure on expectations that the Federal Reserve will cut rates by 25 basis points in December: according to the CME FedWatch Tool, the probability of such a move exceeds 80%.

At 15:00 (GMT+2), Jerome Powell will speak, likely reiterating the need for caution, although it will be difficult to ignore the worsening US labor-market indicators. The monthly US jobs report will not be released this week: due to the government shutdown, it will be published only after the Fed meeting. Meanwhile, markets are also pricing in potential policy easing from the Bank of England, whose meeting is scheduled for December 18, while inflation risks in the UK remain higher than in the US. At 11:30 (GMT+2), investors will review October credit data: net consumer lending is expected to slow from GBP 7.0 billion to GBP 6.4 billion, while mortgage approvals may decline from 65,944 to 64,400.

AUD/USD

The Australian dollar is strengthening in AUD/USD, extending last week’s strong bullish momentum. The pair is testing 0.6550 to the upside. Slight support came from Melbourne Institute inflation data: Australia’s TD-MI yearly inflation rose from 3.1% to 3.2%, while the monthly reading remained at 0.3%. This reinforced expectations that the Reserve Bank of Australia (RBA) will not rush into further rate cuts.

However, gains were limited by mixed manufacturing PMI data from Australia and China. Australia’s S&P Global manufacturing PMI held at 51.6 in November, while China’s Caixin/S&P Global index fell from 50.6 to 49.9, below the forecast of 50.5.

Corporate profit data for Q3 2025 was also mixed: profits showed zero growth after a –2.6% decline previously, while forecasts pointed to +1.7%. On Wednesday at 02:30 (GMT+2), updated Q3 GDP data will be released: the quarterly pace is expected to rise from 0.6% to 0.7%, while annual growth is projected at 1.8%. Meanwhile, the US dollar remains pressured by expectations of a December Fed rate cut. Key labor-market data for November will not be released this week, but on Wednesday at 15:15 (GMT+2), ADP will publish private-sector employment numbers, forecast at +20,000 after +42,000 previously.

USD/JPY

The US dollar is weakening against the Japanese yen, with the pair testing 155.50 to the downside. Traders are focused on Japan’s macroeconomic releases: capital expenditure slowed from 7.6% to 2.9% in Q3, far below expectations of 5.9%, while the Jibun Bank manufacturing PMI for November edged down from 48.8 to 48.7. Investors also assessed Tokyo inflation data: annual CPI fell from 2.8% to 2.7%, while core CPI excluding food and energy held at 2.8%, adding pressure on the Bank of Japan regarding further policy tightening.

Additional support for the yen came from stronger-than-expected industrial production and retail sales data for October. Industrial output slowed from 2.6% to 1.4% m/m, but still beat the 0.6% forecast. Retail sales surged from 0.2% to 1.7% m/m, more than double expectations of 0.8%, while large-store sales rose from 3.0% to 5.0%. Unemployment held at 2.6%, while analysts expected a decline to 2.5%.

Today, US PMI releases from S&P Global (16:45 GMT+2) and ISM (17:00 GMT+2) will again be in focus. At 15:00 (GMT+2), Fed Chair Jerome Powell will speak and may address the likelihood of further policy easing in December. According to the CME FedWatch Tool, the probability of a 25bps rate cut to 3.75% at the upcoming meeting is approaching 90%.

XAU/USD

Gold is trading flat near 4230.00 in XAU/USD. During the morning session, the instrument briefly refreshed its local highs from October 21, but investors remain cautious. At 15:00 (GMT+2), Fed Chair Jerome Powell will speak, potentially commenting on market expectations for lower borrowing costs. He is likely to strike a cautious tone once again, urging patience until more macroeconomic signals emerge.

The key November labor-market report will be released only after the Fed meeting, and the October report was not published due to the shutdown. On Wednesday at 15:15 (GMT+2), ADP will release private-sector employment data, expected at +20,000 following +42,000 previously.

On Friday at 15:30 (GMT+2), investors will assess PCE price-index data — the Fed’s preferred inflation gauge. Market expectations suggest core PCE will come in at 2.9% y/y and 0.2% m/m for September, while the broader PCE index is expected to rise from 2.7% to 2.8% y/y and remain at 0.3% m/m.