The market is gradually pricing in the likelihood that the Bank of Japan may still move to adjust borrowing costs at its 18–19 December meeting. The shift in expectations was driven by comments from several BOJ and government officials, which many participants interpret as preparation for tighter monetary conditions, even though no explicit signals have been given yet. At the same time, Prime Minister Sanae Takaichi’s stance remains ambiguous: on the one hand, she publicly calls for expanded fiscal stimulus and the preservation of accommodative monetary policy to support domestic demand; on the other, she has not made it clear whether she is ready to support an additional rate hike this year. Against this backdrop, concerns are growing that the government may put pressure on the central bank, which, in the view of some investors, would only accelerate the yen’s depreciation path. Speaking before the House of Representatives’ Committee on Financial Affairs on 21 November, BOJ Governor Kazuo Ueda effectively acknowledged that further weakening of the national currency increases the risk of faster consumer price growth, especially in imported goods. Meanwhile, inflation has been running above the 2.0% target for several quarters. A number of analysts believe that if the Bank of Japan again refrains from raising rates in December, the market could test the 160.00 yen per dollar area, which would further increase the financial burden on households.

At the same time, the yen received support on Friday from October industrial production and retail sales data. Industrial output fell from 2.6% to 1.4% m/m versus a 0.6% forecast and slowed from 3.8% to 1.5% y/y, while retail sales growth accelerated sharply from 0.2% to 1.7%, more than double expectations of 0.8%. Sales at large retailers also rose from 3.0% to 5.0%. The unemployment rate in October held at 2.6%, whereas some experts had not ruled out a decline to 2.5%.

For US investors, today’s focus will be on November business activity data from S&P Global at 16:45 (GMT+2) and from the Institute for Supply Management (ISM) at 17:00 (GMT+2). Forecasts suggest the S&P Global index will remain at 51.9 points, while the ISM manufacturing gauge may edge down from 48.7 to 48.6 points. At 15:00 (GMT+2), Federal Reserve Chair Jerome Powell is scheduled to speak and may touch on the prospect of fresh monetary easing in December. According to the CME Group FedWatch Tool, markets currently assign close to a 90.0% probability that the Fed will cut its policy rate by 25 basis points to 3.75% at the upcoming meeting.

Support and resistance levels

On the daily chart, Bollinger Bands are turning sideways: the price range is narrowing slightly but remains wide enough for the current level of market activity. MACD is moving lower, maintaining a firm sell signal as the histogram stays below the signal line. Stochastic is showing a similar trajectory but is quickly approaching oversold territory, indicating rising risks of short-term overselling of the US dollar.

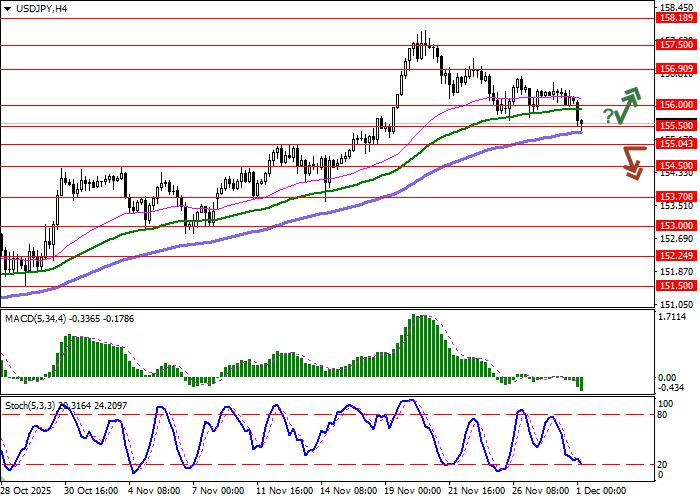

Resistance levels: 156.00, 156.90, 157.50, 158.18.

Support levels: 155.50, 155.04, 154.50, 153.70.

Trading scenarios and USD/JPY forecast

Short positions may be opened after a confident breakout below 155.04 with a target at 153.70 and a stop-loss at 156.15. Implementation period: 2–3 days.

A rebound from 155.50 as support followed by a breakout above 156.00 may serve as a signal to open new long positions with a target at 157.00 and a stop-loss at 155.50.

Base scenario

| Timeframe | Intraday |

| Recommendation | SELL STOP |

| Entry point | 155.00 |

| Take Profit | 153.70 |

| Stop Loss | 156.15 |

| Key levels | 153.70, 154.50, 155.04, 155.50, 156.00, 156.90, 157.50, 158.18 |

Alternative scenario

| Recommendation | BUY STOP |

| Entry point | 156.00 |

| Take Profit | 157.00 |

| Stop Loss | 155.50 |

| Key levels | 153.70, 154.50, 155.04, 155.50, 156.00, 156.90, 157.50, 158.18 |