Investors and forex traders are counting on a change in stance from Fed Chair Jerome Powell, as earlier data from the University of Michigan showed that one-year inflation expectations for December were revised down from 4.5% to 4.1%, and five-year expectations from 3.4% to 3.2%. However, key data are still missing, since the US Labor Department’s November employment report was postponed to next week due to the impact of the record-long government shutdown that ended in November. Today at 11:00 (GMT+2), investors will focus on Italian industrial production data: forecasts suggest a slowdown in monthly growth to –0.3% from 2.8% in the previous month, and in annual terms to 0.2% from 1.5%. The single currency received modest support yesterday from German foreign trade statistics, which showed that exports in October rose by 0.1% after 1.5% a month earlier, while analysts had expected –0.2%. Imports fell by 1.2% after a 3.1% increase, versus a preliminary forecast of 0.2%, pushing the trade surplus higher from EUR 15.3 billion to EUR 16.9 billion, compared with expectations of EUR 15.2 billion.

GBP/USD

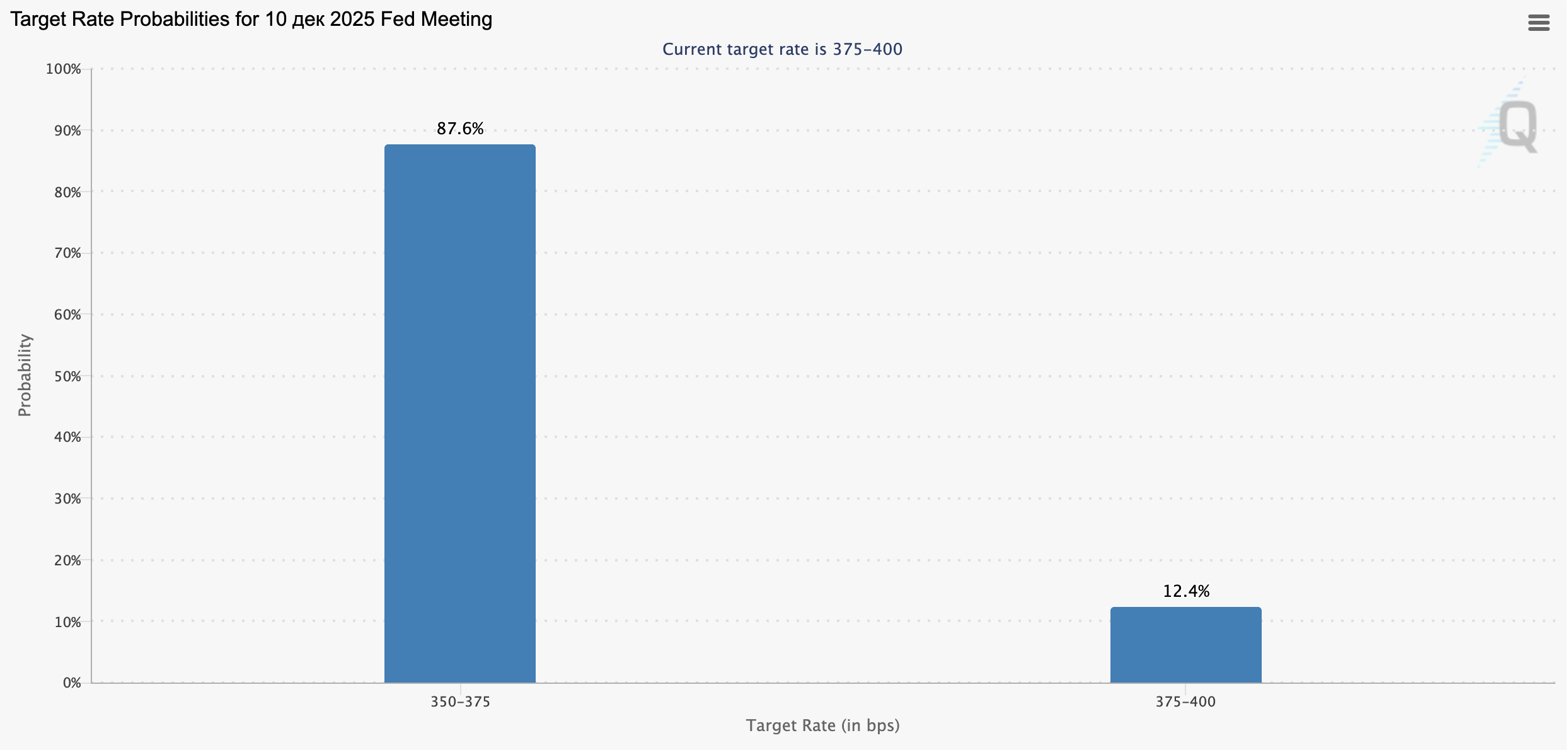

The pound is gaining against the US dollar in the GBP/USD pair, correcting after a moderate decline the day before: the instrument is testing 1.3310 for an upward breakout as market participants await the Fed’s decision, which will be released today at 21:00 (GMT+2). Analysts are confident in a 25-basis-point rate cut to 3.75%, and this scenario is largely priced into the current quotes of the US currency. At the same time, the regulator is expected to publish updated economic projections, which could form the basis for analysis of future monetary policy changes in early 2026. The US dollar received notable support yesterday from JOLTS job openings statistics: vacancies rose from 7.227 million to 7.658 million in September, and from 7.658 million to 7.670 million in October. Separately, investors focused on employment data from Automatic Data Processing (ADP): over the last four weeks, the indicator increased by 4.75 thousand after –13.5 thousand a month earlier. In turn, the pound reacted with a moderate decline yesterday to slower retail sales from the British Retail Consortium (BRC), which fell from 1.5% to 1.2% in November, while market participants had expected 2.4%. Such a sharp slowdown in sales is likely to put pressure on the Bank of England regarding a potential easing of policy at its 18 December meeting.

AUD/USD

The Australian dollar is strengthening against the US dollar in the AUD/USD pair, holding near 0.6640 as market participants await the outcome of the US Federal Reserve meeting today at 21:00 (GMT+2).

It is highly likely that officials will cut the interest rate by 25 basis points to 3.75%. Analysts also expect that Fed Chair Jerome Powell’s tone may turn more dovish as inflation risks ease. Recall that data from the University of Michigan published on Friday showed a decline in one-year inflation expectations in December from 4.5% to 4.1%, while the five-year gauge was revised from 3.4% to 3.2%. This turned out to be noticeably below average forecasts, leaving policymakers with few strong arguments in favor of keeping monetary settings unchanged. Powell may once again point to risks in global trade and the negative effects of multiple import tariffs introduced by the White House administration. Yesterday, the US currency received some support from JOLTS job openings data, which showed an increase in vacancies in September from 7.227 million to 7.658 million and in October from 7.658 million to 7.670 million. In addition, investors continue to assess the latest Reserve Bank of Australia (RBA) meeting: as expected, the regulator unanimously decided to keep the key interest rate at 3.60%. In the accompanying statement, officials noted that economic activity continues to recover, supported by rising domestic demand and easier financial conditions since the beginning of the year. At the same time, the labor market remains tight: unemployment is rising and employment growth is slowing, which could put pressure on the RBA going forward. The regulator also noted rising inflation risks but stressed that more time is needed for definitive conclusions.

USD/JPY

The US dollar is losing ground against the Japanese yen in the USD/JPY pair, correcting after strong gains earlier in the week: the instrument is once again preparing to test 156.65 for a downward breakout, retreating from the local highs of 24 November that were updated yesterday. Market activity remains subdued as traders await the Fed’s decision at 21:00 (GMT+2) today. They are confident in a 25-basis-point rate cut but are hoping for a somewhat more dovish stance from Fed Chair Jerome Powell amid easing inflation risks. Meanwhile, last week the US November labor market report was not published due to the consequences of the government shutdown.

At the same time, the US currency received some support yesterday from JOLTS job openings data, which showed that vacancies in September rose from 7.227 million to 7.658 million and in October from 7.658 million to 7.670 million. Market participants also took note of the increase in the NFIB business optimism index in November from 98.2 to 99.0 points, compared to a forecast of 98.4. Today, Japanese investors and forex traders are focused on producer inflation data: according to November results, the producer price index stood at 2.7% year-over-year, while on a monthly basis it fell from 0.5% (revised from 0.4%) to 0.3%. Slowing inflation may hinder the Bank of Japan’s plans for further monetary tightening, which currently diverge from the economic policy of Prime Minister Sanae Takaichi, who favors a dovish stance.

XAU/USD

The XAU/USD pair is gaining value, consolidating near 4200.00, with prices still supported by expectations of lower borrowing costs from the US Federal Reserve. Recall that the meeting outcome will be released today at 21:00 (GMT+2), and investors now expect a 25-basis-point cut to 3.75%. In addition, updated projections from policymakers will be published and may clarify the prospects for further easing in the first half of 2026.

Market participants also expect Fed Chair Jerome Powell to shift his tone in light of data from the University of Michigan, which showed a decline in one-year inflation expectations from 4.5% to 4.1%, while the five-year indicator was revised from 3.4% to 3.2%. Gold receives additional support from expectations of continued dovish rhetoric from the Bank of England, which will meet on 18 December. The European Central Bank (ECB), in turn, is not yet planning to adjust its monetary stance. Moreover, given rising inflation risks, the regulator no longer rules out the possibility of tightening its position. Another factor supporting gold prices remains geopolitical risk, particularly the Russia-Ukraine conflict. In recent weeks, US President Donald Trump has been attempting to promote a peace plan that could significantly improve business sentiment in the region.