Forex Today: The Dollar Loses Ground

Investors and forex traders are closely watching the recent U.S. Supreme Court hearing on the legality of the “retaliatory” trade tariffs imposed by the Republican White House administration. The justices appear inclined to rule that President Donald Trump lacked sufficient authority to raise tariffs. Officials noted that such duties effectively act as a new form of taxation, which U.S. companies ultimately pass on to consumers. The Court also highlighted that the tariff hikes, introduced under the 1977 International Emergency Economic Powers Act (IEEPA), represent a unilateral expansion of executive power at the expense of Congress. While the final decision has not yet been announced, Treasury Secretary Scott Bessent stated that if the ruling goes against the administration, the White House will seek alternative ways to impose new protectionist measures.

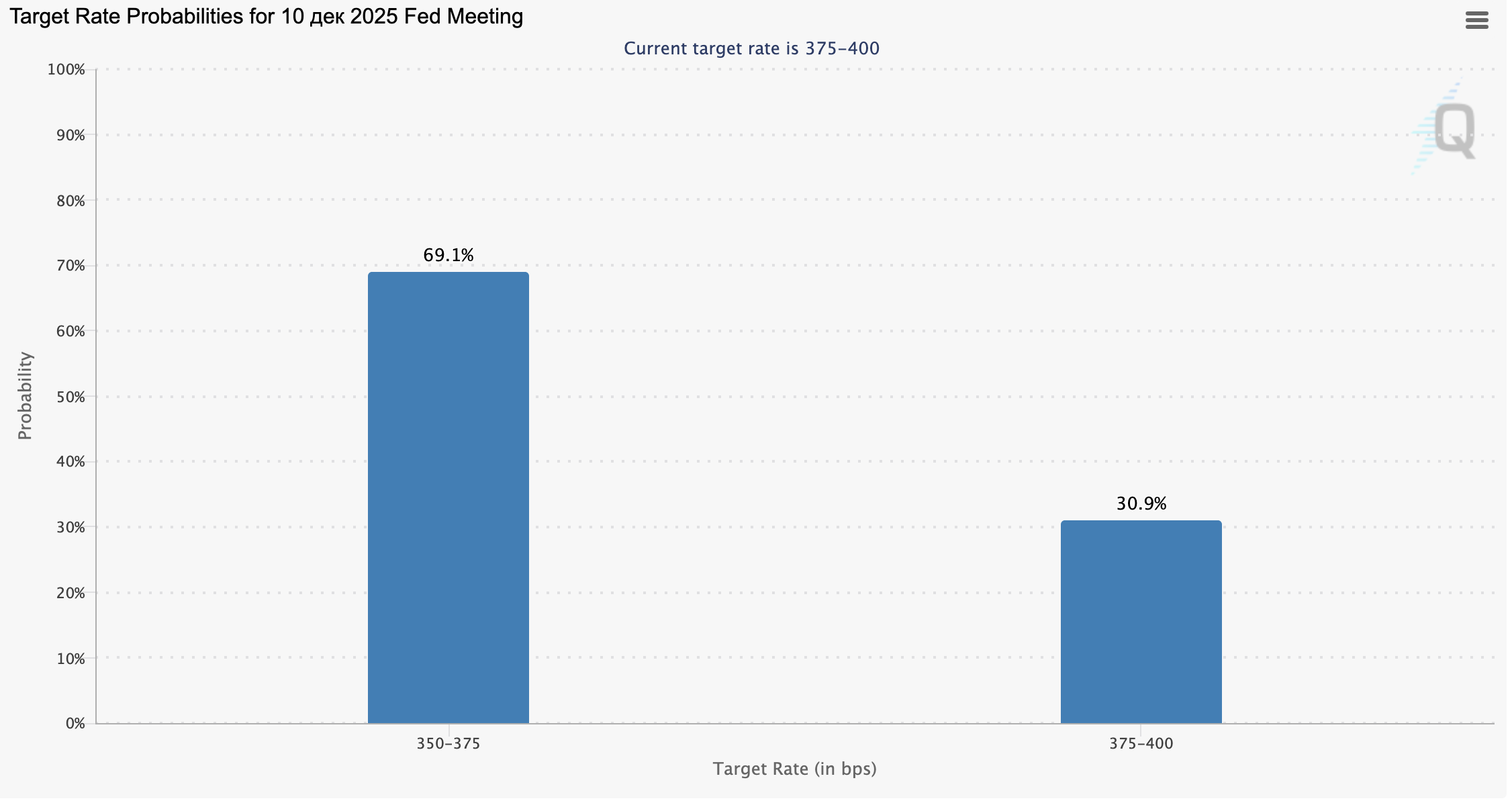

- Current target range: 3.75–4.00%

- Base scenario — a rate cut by 25 bps to 3.50–3.75%, with a probability of 69.1%.

- Alternative scenario — maintaining the current level of 3.75–4.00%, with a probability of 30.9%.

Interpretation:

The majority of market participants expect a monetary policy easing at the December Fed meeting, signaling that investors are pricing in the first rate cut after a long period of tight conditions. Such expectations typically weigh on the U.S. dollar by reducing yields on U.S. assets while supporting equities and alternative assets such as gold and cryptocurrencies.

Eurozone

The euro is gaining against the U.S. dollar but shows mixed performance versus the yen and the pound.

September retail sales data showed a 0.1% monthly decline against forecasts for a 0.2% rise, while annual growth slowed from 1.6% to 1.0%, in line with expectations. Sales increased in Germany (+0.2%) and Spain (+0.4%) but fell in Italy, France, and the Netherlands — a worrying sign that weaker household spending could slow economic growth. European Central Bank (ECB) Vice President Luis de Guindos said today that the regulator is satisfied with the current interest rate level and expects any drop in inflation below the 2.0% target to be temporary. He added that ECB policymakers have become more optimistic about GDP growth, expecting it to reach at least 1.0% by year-end.

United Kingdom

The British pound is strengthening against the U.S. dollar but showing mixed moves against the yen and the euro.

The Bank of England kept its benchmark interest rate unchanged at 4.00%, with five votes in favor and four against. Policymakers noted that inflation has peaked and may begin to slow in the coming months as weaker growth and labor market deterioration weigh on demand. Governor Andrew Bailey said rates are likely to continue falling in the near term, raising market expectations for rate cuts to around 60%. Meanwhile, the October manufacturing PMI fell from 46.2 to 44.1 points, below the forecast of 46.7, reflecting a deeper contraction in the sector.

Japan

The Japanese yen is gaining against the U.S. dollar but remains mixed against the euro and the pound.

Japan’s October services PMI edged down from 53.3 to 53.1 points but still beat expectations of 52.4, pointing to a steady recovery in the non-manufacturing sector driven by domestic demand. However, external new orders continue to decline. Businesses remain cautious due to labor shortages and ongoing global trade uncertainty.

Australia

The Australian dollar is weakening against the euro, pound, and yen but trades mixed versus the U.S. dollar.

September trade data showed exports rising by 7.9% after an 8.7% drop in the previous month, while imports slowed from 3.3% to 1.1%. As a result, the trade surplus widened from 1.111 billion to 3.938 billion Australian dollars, reflecting economic stability despite global trade headwinds and reinforcing expectations that the Reserve Bank of Australia (RBA) will maintain its current monetary policy at least until early next year.

Oil

Oil prices show mixed dynamics: early gains gave way to losses later in the session.

According to the latest weekly report from the U.S. Energy Information Administration (EIA), crude oil inventories jumped by 5.202 million barrels versus a forecast decline of 2.5 million barrels. Gasoline and distillate stocks fell by 4.729 million and 0.643 million barrels, respectively. Meanwhile, the U.S. dollar strengthened on expectations that the Federal Reserve will keep its current monetary stance, pressuring commodities and alternative assets. Reuters sources also reported that Kazakhstan’s crude oil output fell by 10% last month to 1.69 million barrels per day, though this still exceeds the quota agreed with OPEC+.