Last week, the report was not published due to the impact of the government shutdown, meaning Federal Reserve officials had to base their interest-rate decision on indirect indicators. A sharp slowdown in nonfarm payroll growth is expected, from 119,000 previously, as widespread layoffs were recorded in November amid the shutdown. Wage growth in October and November is projected to remain broadly unchanged at around 0.2% month-on-month and 3.8% year-on-year, while the unemployment rate may rise again to 4.4%.

Strong labor market data could significantly alter expectations regarding potential monetary easing in January 2026, while weaker figures would reinforce the case for policy adjustments.

Strong labor market data could significantly alter expectations regarding potential monetary easing in January 2026, while weaker figures would reinforce the case for policy adjustments.

At 12:00 (GMT+2) today, investors will focus on October industrial production data from the euro area. European manufacturers have been facing increasing challenges amid the halt in cheap energy imports from Russia, high import tariffs, and intensifying competition from China. Preliminary estimates suggest production growth will slow from 0.2% to 0.1% month-on-month and remain at 1.2% year-on-year.

Tomorrow at 11:00 (GMT+2), December business activity data from S&P Global will be released. The manufacturing PMI is expected to rise from 49.6 to 49.9 points, which could provide modest support for the euro. On Thursday at 15:15 (GMT+2), the European Central Bank (ECB) will announce its policy decision. Markets are almost fully convinced that the ECB will keep interest rates unchanged at 2.15% and signal that subdued inflation does not warrant a shift in monetary policy in the near term.

GBP/USD

The British pound is losing ground against the US dollar, extending the previous day’s corrective move. The GBP/USD pair is testing the 1.3355 level to the downside as investors prepare for the UK labor market report due tomorrow at 09:00 (GMT+2).

Forecasts suggest that unemployment benefit claims in November will decline from 29,000 to 22,300. Employment is expected to fall again in October after a sharp drop of 22,000 in September. Average earnings excluding bonuses are projected to slow from 4.6% to 4.5%, while earnings including bonuses may ease from 4.8% to 4.4%.

A pronounced slowdown in wage growth could weaken the Bank of England’s case for keeping monetary policy unchanged, as it would signal easing inflationary pressures.

Tomorrow at 11:30 (GMT+2), December PMI data will also be released, with activity remaining comfortably above the 50.0 threshold that separates expansion from contraction.

Meanwhile, expectations for the US labor market report due tomorrow at 15:30 (GMT+2) point to a sharp slowdown in nonfarm job creation from 119,000, reflecting mass layoffs during the government shutdown. Wage growth is expected to remain steady at around 0.2% month-on-month and 3.8% year-on-year, while unemployment may again reach 4.4%.

On Thursday at 14:00 (GMT+2), the Bank of England will hold its policy meeting. Markets currently lean toward a 25 basis point rate cut to 3.75%, despite inflation remaining relatively elevated.

AUD/USD

The Australian dollar is gaining ground against the US dollar, offsetting the bearish correction seen over the past two days. The AUD/USD pair is testing the 0.6640 level to the upside as traders assess macroeconomic data from China.

Industrial production growth in China slowed from 4.9% to 4.8% in November, missing the 5.0% forecast, while retail sales growth dropped sharply from 2.9% to 1.3%. These figures may prompt Chinese authorities to introduce additional stimulus measures.

In the US, the New York Fed manufacturing activity index will be released today at 15:30 (GMT+2). It is expected to decline significantly from 18.7 to 10.6 points, which could weigh on the US dollar.

At 17:00 (GMT+2), investors will also review December housing market data from the NAHB, with the index expected to edge up from 38.0 to 39.0 points.

Tomorrow at 00:00 (GMT+2), Australia will publish December PMI data from S&P Global. In the previous month, the manufacturing PMI stood at 51.6 points, while the services PMI was recorded at 52.8 points.

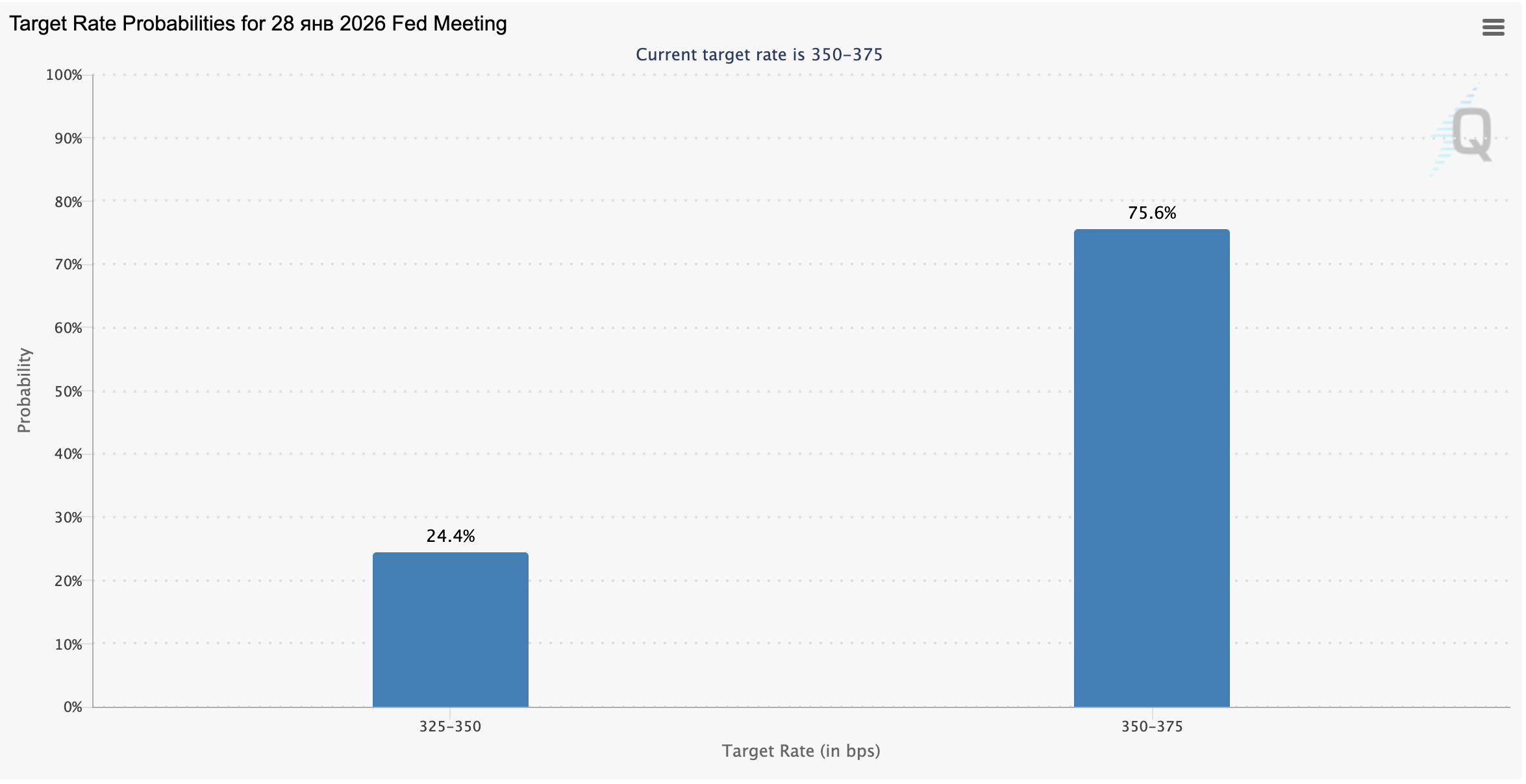

Meanwhile, the delayed US labor market report for November, due at 15:30 (GMT+2), could significantly influence the direction of US monetary policy. Federal Reserve officials currently project only one rate cut, while market participants continue to price in two adjustments, citing rapidly easing inflation risks.

Last week, the Fed cut interest rates by 25 basis points to 3.75% and maintained its projections for 2026 and 2027 unchanged, while improving its outlook for inflation and economic growth.

The AUD/USD pair is also supported by expectations that the Reserve Bank of Australia (RBA) will not rush into another rate cut in early 2026.

In early December, the RBA kept its policy rate unchanged at 3.60% in a unanimous decision. In its accompanying statement, officials noted that economic activity continues to recover amid looser financial conditions, although the labor market remains underutilized and shows concerning trends. RBA Governor Michele Bullock stated that the board does not rule out the possibility of a rate hike if economic conditions require it.

USD/JPY

The US dollar is weakening against the Japanese yen, with the USD/JPY pair testing the 155.15 level to the downside. However, investors remain cautious ahead of the key US labor market report for November, scheduled for tomorrow at 15:30 (GMT+2).

October data was not released at all, while the upcoming figures are delayed due to the government shutdown. Strong data could shift expectations around future Fed easing, while weaker results may force the central bank to reassess its rate outlook, which currently implies only one rate cut in 2026.

Investors and FX traders, however, are still pricing in two rate moves. Much will depend on labor market conditions and potential leadership changes at the Fed. Jerome Powell’s second four-year term expires in May 2026, and White House economic adviser Kevin Hassett is seen as one of the leading candidates to succeed him.

The Bank of Japan will hold its policy meeting on December 19. Analysts do not rule out a 25 basis point rate hike to 0.75%, which could intensify tensions between BoJ Governor Kazuo Ueda and the country’s political leadership. Inflation has accelerated to 3.0%, well above the 2.0% target, while labor market challenges and a sharp rise in 10-year government bond yields to their highest levels since 2007 complicate the outlook.

Prime Minister Sanae Takaichi opposes tighter policy, favoring a more accommodative economic approach aimed at boosting consumption through wage indexation and the restoration of social benefits. In the third quarter, GDP contracted by 2.3%, while real wages fell by 1.4% in September, extending a nine-month downward trend.

Investor attention today is also focused on fourth-quarter business sentiment data. The Tankan index for large manufacturers rose from 14.0 to 15.0 points, while the services index remained unchanged at 34.0 points, missing expectations of 35.0. Meanwhile, the outlook index for large manufacturers increased from 12.0 to 15.0 points versus a forecast of 13.0, and the services activity index accelerated from 0.1% (revised from 0.3%) to 0.9% in October.

XAU/USD

Gold is strengthening against the US dollar, extending last week’s bullish momentum. The XAU/USD pair is testing the 4,340.00 level to the upside and is preparing to set new local highs last seen on October 21.

Demand for gold continues to rise amid easing monetary policy by major central banks. Last week, the Federal Reserve cut interest rates by 25 basis points and maintained its rate projections for 2026, while improving its outlook for economic growth and inflation.

Markets also expect the Bank of England to continue its dovish stance this week, despite ongoing efforts to curb elevated inflation. In addition, investors and FX traders anticipate that global central banks will continue increasing gold purchases in the near term.

According to a recent report from the World Gold Council (WGC), global central banks purchased approximately 53.0 tonnes of gold in October, marking the highest monthly total so far this year.

On Thursday at 15:30 (GMT+2), US inflation data will be released and could significantly impact sentiment toward the US dollar. Forecasts do not rule out an acceleration in both headline and core consumer price inflation in November, from 3.0% to 3.2%.