According to the Financial Times, European countries have initiated preliminary contacts with Iran to restore oil and gas exports through the Strait of Hormuz, with France and Italy currently among the main participants. Sources indicate that shipping companies are considering naval escorts for tankers by Western forces, although there are no guarantees of progress or readiness from Iranian authorities to engage in dialogue. Previously, Italy, France, and Greece deployed vessels in the Red Sea as part of the EU’s Aspides naval mission, but no fleet is currently prepared to assume responsibility for escorting shipments under the high risk of attacks from Iran’s Islamic Revolutionary Guard Corps (IRGC). Bloomberg also reports active involvement from France in seeking a resolution, while Saudi Arabia, Oman, and Turkey are acting as mediators. The lack of tangible progress remains a key driver of volatility in global energy markets, putting additional pressure on macroeconomic stability in importing countries.

At the end of last week, market participants focused on inflation data. Consumer prices in France rose by 0.6%, slightly below January’s 0.7%, while the annual figure stood at 0.9%, down from 1.0%. The EU-harmonized index increased by 0.7% after a previous –0.4% reading, with the annual rate rising from 0.4% to 1.1%. These figures may represent the lowest levels for the first half of the year, as March data will likely reflect the impact of geopolitical tensions and rising oil prices.

In the bond market, recent auctions showed rising yields. Three- and six-month securities were placed at 2.108% and 2.199% versus 2.097% and 2.212% previously, while twelve-month yields climbed to 2.353% from 2.339%. After reaching a local peak of 2.330%, yields have entered a consolidation phase. This morning, one-year bonds are trading at 2.442%, slightly below Friday’s 2.459%, while 10-year yields stand at 3.616% versus 3.664%, and 20- and 30-year yields at 4.190% and 4.495%, respectively, both slightly lower than previous levels.

Top gainers in the index include STMicroelectronics N.V (+2.69%), Unibail-Rodamco-Westfield SE (+2.58%), Societe Generale SA (+1.37%), Danone SA (+1.25%), and Carrefour SA (+1.26%).

Among the main decliners are Capgemini SE (–2.55%), Bureau Veritas SA (–1.77%), Thales SA (–1.58%), Pernod Ricard SA (–1.34%), and Renault SA (–0.91%).

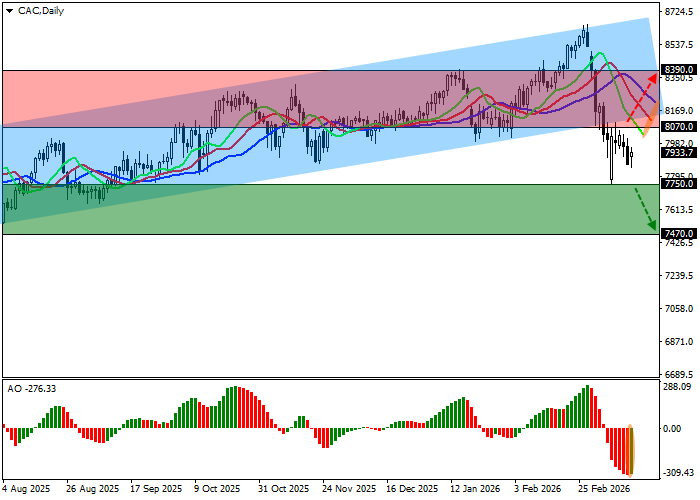

Support and resistance levels

On the daily chart, the index continues its local correction, remaining below the support line of the ascending channel with dynamic boundaries at 8,700.0–8,070.0.

Technical indicators maintain a bearish signal established earlier this month: fast EMAs on the Alligator indicator are widening their range, while the AO histogram is forming corrective bars below the zero line.

Support levels: 7,750.0, 7,470.0.

Resistance levels: 8,070.0, 8,390.0.

Trading scenarios and CAC 40 forecast

Short positions may be considered after consolidation below 7,750.0 with a target at 7,470.0. Stop-loss: 7,860.0. Timeframe: 7 days or more.

Long positions may be considered after consolidation above 8,070.0 with a target at 8,390.0. Stop-loss: 7,990.0.

Scenario

| Timeframe | Weekly |

| Recommendation | SELL STOP |

| Entry point | 7749.5 |

| Take Profit | 7470.0 |

| Stop Loss | 7860.0 |

| Key levels | 7470.0, 7750.0, 8070.0, 8390.0 |

Alternative scenario

| Recommendation | BUY STOP |

| Entry point | 8070.5 |

| Take Profit | 8390.0 |

| Stop Loss | 7990.0 |

| Key levels | 7470.0, 7750.0, 8070.0, 8390.0 |