Hyperliquid and Phantom Call on the US to Revise DeFi Rules

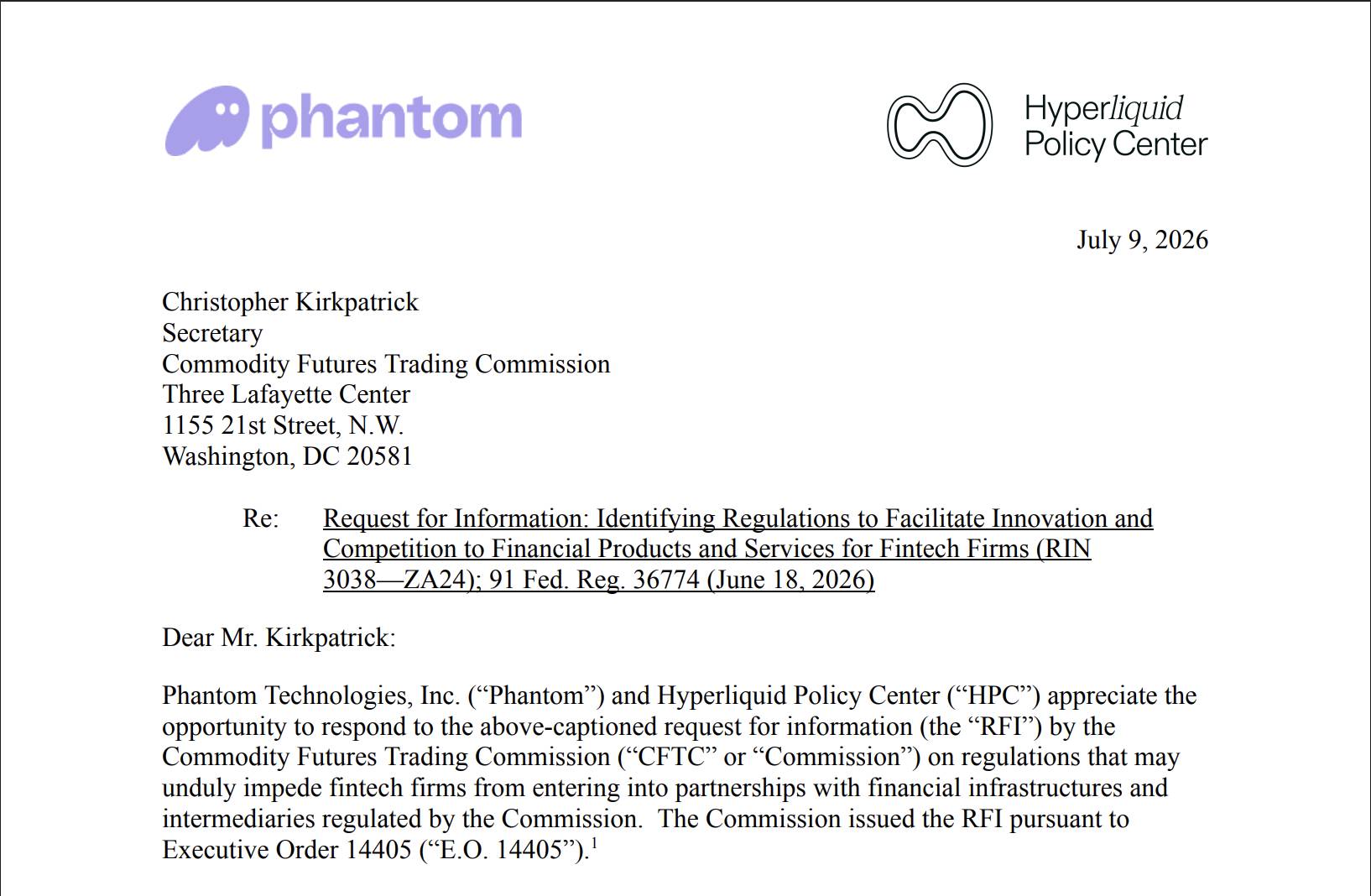

On July 9, two major crypto industry players, the Hyperliquid Policy Center, or HPC, and Phantom, submitted a letter to the US Commodity Futures Trading Commission, or CFTC, urging the agency to modernize its regulatory framework to better accommodate the development of on-chain trading protocols.

The move came in response to a Request for Information launched by the CFTC and the SEC in mid-June under Executive Order 14405. The initiative is intended to review regulations that may be preventing fintech companies from working with financial institutions overseen by the CFTC.

In the letter, the Hyperliquid Policy Center and Phantom made three main recommendations to the CFTC:

- The CFTC should clarify that developing source code for on-chain protocols does not automatically amount to operating an exchange or clearinghouse. Developers who do not hold customer assets, receive orders or control user transactions should not necessarily be required to register.

- The CFTC should issue guidance allowing derivatives exchanges, clearing organizations and futures commission merchants, or FCMs, to use blockchain infrastructure for functions such as order matching, clearing, settlement, margin management and recordkeeping, provided they continue to comply with the Commodity Exchange Act, or CEA.

- The CFTC should formalize the position previously communicated to Phantom that non-custodial wallets and blockchain interfaces should not be treated as intermediaries merely because they provide users with tools to access regulated markets.

Existing Rules Were Written for Wall Street, Not DeFi

Most of the arguments presented by Hyperliquid and Phantom focus on the differences between traditional finance and DeFi.

According to the two organizations, the current legal framework was built for a model in which customers hand over their money and trading instructions to several layers of intermediaries, including brokers, exchanges and clearinghouses. These intermediaries hold assets, execute trades and assume responsibility for settlement.

On-chain markets operate in a fundamentally different way. Users retain their own private keys, control their own assets and transact directly with one another through smart contracts. No intermediary holds customer funds or stands between the parties during the transaction process.

For this reason, Hyperliquid and Phantom argue that DeFi regulation should focus on entities that actually hold assets or execute transactions on behalf of customers, rather than software developers who only create open-source code.

One of the letter’s central arguments is that software development is not the same as operating an exchange.

The two parties argue that blockchain source code is not a legal entity. It cannot enter into contracts, hold customer assets or assume legal responsibility in the same way as a company. Merely developing or publishing code should therefore not be treated as operating an exchange or clearinghouse that requires a license.

The Hyperliquid Policy Center and Phantom also argue that modern blockchain infrastructure can meet, and in some cases exceed, many existing regulatory standards.

Functions such as order matching, margin management, clearing, settlement and position liquidation can be automated through smart contracts. At the same time, transaction data can be recorded publicly on-chain, improving transparency and reducing the risk of manipulation, front-running or misuse of customer assets.

Hyperliquid and Phantom therefore believe the CFTC should formally recognize that blockchain infrastructure can be used to satisfy requirements related to recordkeeping, margin management and customer asset protection under the current legal framework, rather than continuing to apply rules designed for traditional financial systems.

The letter was published as debate over the regulation of on-chain derivatives continues to intensify in the United States.

CME Group previously lobbied the CFTC to increase its oversight of Hyperliquid and later sued the agency over its decision to approve perpetual futures products.

conclusion: The proposal highlights the growing mismatch between traditional financial regulation and decentralized market infrastructure. Clearer rules separating software development from regulated financial intermediation could reduce legal uncertainty while preserving oversight of entities that actually control customer assets or execute trades.