Stablecoins are becoming a digital alternative to the dollar

Today, stablecoins are drawing increasing attention from major financial market participants. Banks and payment companies see them as a tool for:

- faster settlements;

- new payment models;

- the expansion of cross-border financial services;

- the creation of new digital products.

In the White House report, stablecoins are described as digital dollars that can be redeemed at a 1:1 ratio and are typically backed by reserves such as cash or short-term government bonds.

Their role is especially important outside the United States, where they are often used in countries with unstable national currencies as a more reliable digital equivalent of the dollar.

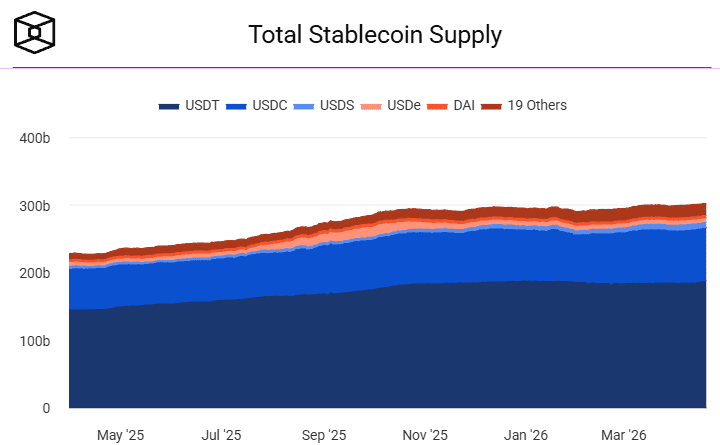

The stablecoin market keeps expanding

The market continues to grow, although its structure remains highly concentrated. The bulk of it is still controlled by two dominant players:

- Tether (USDT) — around $185 billion

- USDC — around $75 billion

The total market is now estimated at approximately $300 billion.

From an infrastructure perspective, Ethereum remains the leading network, although Tron is also strengthening its position, especially in global payments and USDT usage outside Ethereum.

The key question: are stablecoins displacing bank deposits?

The central issue of the analysis is whether stablecoins are truly pulling money out of the banking system and thereby weakening lending activity.

The critics’ logic looks like this:

- customers withdraw money from banks;

- move it into stablecoins;

- stablecoin reserves are not used for lending;

- therefore, banks have fewer resources available for loans.

At first glance, that scenario seems logical. But the White House analysis shows that in practice the situation is more complex.

White House view: the money does not disappear from the system, it changes form

According to the report, most stablecoin reserves do not leave the financial system permanently. These funds often return to it in a different form.

For example:

- reserves are invested in short-term US Treasuries;

- the proceeds then flow back into the banking system;

- as a result, what changes first and foremost is the structure of deposits, not their overall volume.

That is why the effect on bank lending appears significantly weaker than many critics had assumed.

How much do stablecoins actually interfere with lending?

According to the report, only around 12% of stablecoin reserves can truly be considered funds directly removed from the part of the banking base that matters for lending.

This refers to the share of reserves held in the form of traditional bank deposits and therefore subject to banking regulations such as:

- reserve requirements;

- liquidity rules;

- other constraints tied to bank regulation.

Most reserves, however, are not kept in deposits but instead in:

- short-term Treasury securities;

- highly liquid instruments;

- money market assets.

That means that even as the stablecoin market grows, what is happening is only a partial redistribution of liquidity rather than a large-scale blow to bank lending.

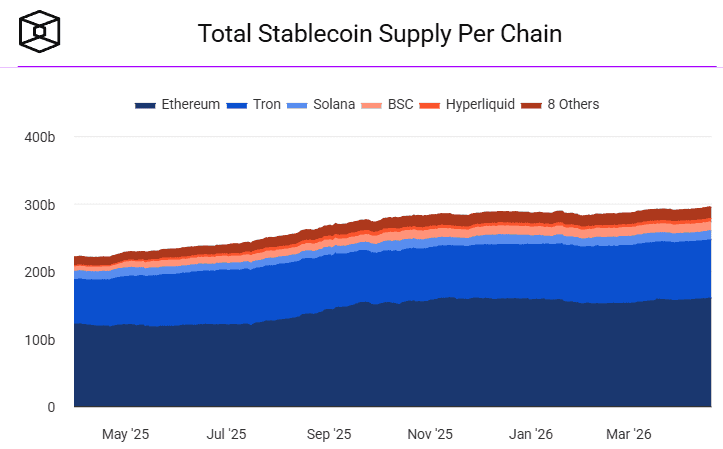

Which blockchains benefit most from stablecoin growth

According to CoinShares analyst Luke Nolan, the growth of the stablecoin market is not evenly distributed. The main beneficiaries are a handful of dominant networks.

Ethereum remains the main settlement infrastructure:

- around 52% of all stablecoins circulate on this network;

- that equals roughly $180 billion;

- around two-thirds of USDC supply is also on Ethereum.

Tron is especially strong in international transfers and payments:

- the network is widely used for USDT outside Ethereum;

- its advantages are near-zero fees and strong popularity in global transactions.

Solana is showing the fastest percentage growth:

- in February 2026, about $650 billion in stablecoin volume was processed through the network;

- that allowed it to surpass Ethereum for the first time on this metric.

In Nolan’s view, Ethereum and Solana increasingly look less like direct rivals and more like complementary ecosystems:

- Ethereum — for large-scale settlements and deep liquidity;

- Solana — for high speed and large transaction throughput.

Why liquidity matters more than the technology itself

The key long-term factor behind stablecoin success is not only speed or transaction cost, but also liquidity.

The deeper a stablecoin is integrated into:

- exchanges,

- DeFi protocols,

- payment services,

- trading infrastructure,

the stronger its network becomes and the more likely it is to attract new capital.

This effect reinforces existing market leaders. Large capital flows tend to concentrate where liquidity already exists, because it is easier and cheaper to execute large transactions there.

Issuers continue to play an outsized role as well — above all Circle and Tether. They are still the main forces deciding which blockchains receive new issuance and liquidity.

Regulation is becoming increasingly important

The next major factor is the legal framework. Initiatives such as the GENIUS Act could create conditions that favor more regulation-compliant stablecoins such as USDC.

At the same time, risks remain. One example is the Drift protocol exploit in early April, when around $230 million in USDC was withdrawn.

Although this incident caused no direct damage to Circle, repeated events of this kind could increase regulatory pressure on the industry.

Another open question remains:

whether institutional players will ultimately favor public blockchains or move toward private networks. The answer will shape the long-term structure of the market.

How investors can benefit from the stablecoin boom

In Nolan’s view, investors have several ways to participate in this trend.

1. Direct exposure — Circle

The company’s business model is directly tied to the growth of USDC. Its main revenue comes from interest income on reserves, which are largely held in short-term bonds and repo transactions. The larger the USDC supply, the greater the potential revenue.

2. Indirect exposure — Coinbase

The company receives part of the income generated by USDC reserves and also benefits from rising trading and transaction activity.

3. Crypto infrastructure exposure — ETH and SOL

For investors comfortable with direct crypto risk, Ethereum and Solana can be viewed as infrastructure plays. Rising stablecoin transaction volumes support demand for:

- gas fees,

- staking assets,

- core network infrastructure.

Stablecoins are moving into the mainstream

Stablecoins are increasingly becoming a full-fledged part of the global financial system. Their use has long gone beyond a narrow crypto niche.

The new US analysis points to an important conclusion:

many of the risks to the banking system that were previously discussed most loudly may be significantly smaller than assumed.

Stablecoins are not so much “draining” capital from banks as they are changing the structure of liquidity within the existing system.

Conclusion

If the question of possible yield on stablecoins is eventually resolved, market growth could accelerate even further. Against this backdrop:

- Ethereum and Solana stand to benefit as infrastructure networks;

- Circle and Tether remain at the center of the market’s economic model;

- the traditional financial system is becoming ever more closely connected with the digital economy.

All of this suggests that in the coming years, stablecoins will play an increasingly important role as a bridge between traditional finance and the blockchain economy.