Market participants continue to analyze the US November labor market report, which was released nearly two weeks late due to the effects of the government shutdown. As a result, the Federal Reserve made its interest rate decision without access to the full set of statistical data. In October, nonfarm payrolls declined by 105.0 thousand after rising by 108.0 thousand in the previous month, while November saw an increase of 64.0 thousand jobs versus expectations of 50.0 thousand.

Meanwhile, average hourly earnings slowed on a monthly basis from 0.4% to 0.1%, below preliminary estimates of 0.3%, and eased year-on-year from 3.7% to 3.5%. This may indirectly point to a further easing of inflationary pressures, which the Federal Reserve continues to view as the main argument for maintaining its current monetary policy stance. In addition, the unemployment rate jumped sharply from 4.4% to 4.6%, signaling cooling conditions in the labor market.

Among Australian data released this week, investors noted mixed business activity indicators. The S&P Global Manufacturing PMI for December rose from 51.6 to 52.2 points, while the Services PMI declined from 52.8 to 51.0 points. Attention was also drawn to a sharp drop in the Westpac Consumer Confidence Index in December, from 12.8% to –9.0%. Slowing economic activity is increasing pressure on the Reserve Bank of Australia (RBA) regarding further monetary easing. It is worth recalling that at its December 9 meeting, policymakers unanimously voted to keep the interest rate unchanged.

At the same time, Westpac Banking Corp. adjusted its fixed mortgage rates upward by 0.35 percentage points following the RBA’s warning of a possible rate hike next year, with the lowest fixed rate now standing at 5.49%. Over the past week, 12 financial institutions — including St George, Bank of Melbourne, BankSA, ING Groep, HSBC, Suncorp, and Australian Mutual Bank — raised at least one fixed-rate product. National Australia Bank (NAB) and Australia and New Zealand Banking Group (ANZ) are expected to follow with increases in February.

Westpac Banking Corp. continues to forecast two rate cuts in May and August 2026, although the probability of a hike has also increased. According to estimates by Canstar, an average borrower with a mortgage of AUD 600,000 and a remaining term of 25 years would pay an additional AUD 1,920 in interest over the next two years by switching from the lowest variable rate to the lowest two-year fixed rate, assuming two rate cuts in May and August.

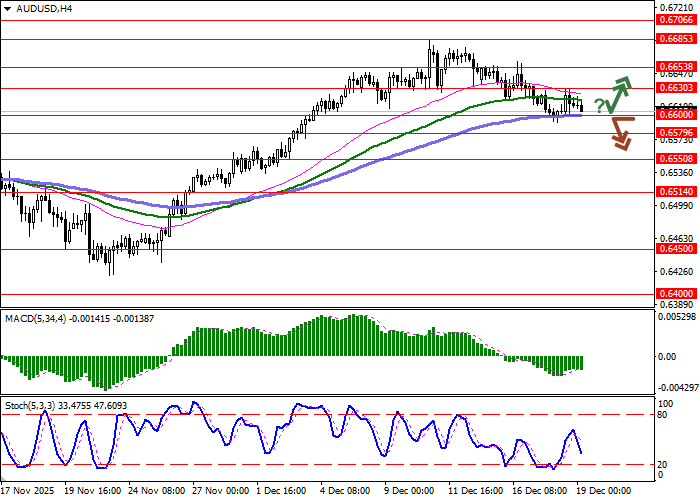

Support and Resistance Levels

On the daily chart, Bollinger Bands show a fairly confident upward bias, while the price range is narrowing, reflecting the emergence of short-term corrective pressure. The MACD has turned lower, forming a strong sell signal as the histogram remains firmly below the signal line. The Stochastic oscillator, having settled below the 20 level, has moved into a sideways pattern, indicating growing risks of short-term oversold conditions for the Australian dollar.

Resistance levels: 0.6630, 0.6653, 0.6685, 0.6706.

Support levels: 0.6600, 0.6579, 0.6550, 0.6514.

Trading Scenarios and AUD/USD Forecast

Short positions may be considered after a confirmed downside breakout below the 0.6600 level, with a target at 0.6550 and a stop-loss at 0.6630. Time horizon: 1–2 days.

A rebound from the 0.6600 support level followed by a breakout above 0.6630 could signal an opportunity to open new long positions targeting 0.6685, with a stop-loss at 0.6600.