Among other releases, at 11:00 (GMT+2) Germany’s IFO Institute will publish business expectations data. Forecasts suggest that the Business Climate Index may slightly accelerate in November from 88.4 to 88.5 points, supported by increased defense spending and ambitious infrastructure modernization plans by the German government. In addition, at 16:45 (GMT+2), European Central Bank President Christine Lagarde will appear and may comment on the region’s growth outlook.

At the same time, further monetary easing is currently not seen as a key priority for the regulator. Markets are pricing in at most one more rate cut of 25 basis points, as inflation remains under control. Still, business activity data released at the end of last week indicated a decline in Germany’s manufacturing PMI from S&P Global and Hamburg Commercial Bank (HCOB), which fell in November from 49.6 to 48.4 points against expectations of 49.8, while the services index dropped from 54.6 to 52.7 points versus a forecast of 53.9. Across the eurozone, the manufacturing figure declined from 50.0 to 49.7 points instead of the expected 50.2, while the services index rose slightly from 53.0 to 53.1 points thanks to strong growth in France, where the indicator jumped from 48.0 to 50.8 points.

Meanwhile, the US dollar is being supported by weakening expectations of possible monetary easing by the Federal Reserve in December. Recall that last week the US Department of Labor released the September labor report, showing a notable increase of 119.0 thousand in non-farm payrolls compared to expectations of 50.0 thousand, while the unemployment rate also rose from 4.3% to 4.4%. Overall, the real situation in the labor sector remains better than pessimistic forecasts, allowing the regulator not to rush any changes to borrowing costs.

GBP/USD

The British pound is also strengthening in the GBP/USD pair, trying once again to gain a foothold above the 1.3100 level. At the end of last week, the instrument managed to post a corrective rise despite mixed UK business activity data from S&P Global for November. The manufacturing index rose from 49.7 to 50.2 points versus expectations of 49.3, while the services index, on the contrary, showed a sharp decline from 52.3 to 50.5 points against a forecast of 52.1.

The composite index also slowed from 52.2 to 50.5 points, while analysts had expected 51.8. In addition, weak retail sales data reflected subdued consumption and purchasing activity: in October, sales fell by 1.1% after rising by 0.7%, while forecasts pointed to 0.0%. On an annual basis, sales dropped from 1.0% to 0.2% versus expectations of 1.5%. The GfK Consumer Confidence Index declined from –17.0 to –19.0 points, slightly worse than the expected –18.0. Falling business activity and extremely слабые retail data significantly increase the likelihood that the Bank of England will move quickly to reduce borrowing costs further. The next regulator meeting is scheduled for December 18. Meanwhile, expectations of a December rate cut by the Federal Reserve have declined sharply after the release of the labor market report last week: the US economy created about 120.0 thousand new jobs in September, well above expectations of 50.0 thousand, while unemployment accelerated from 4.3% to 4.4%, adding further pressure on Fed officials.

AUD/USD

The Australian dollar is strengthening in the AUD/USD pair, trading near 0.6463 and extending the corrective impulse from last Friday, when the instrument rebounded from the local lows of August 22. On Tuesday at 15:30 (GMT+2), the US will publish September producer price data. Forecasts suggest that the year-on-year PPI may accelerate from 2.6% to 2.7%, while the monthly figure may rise from –0.1% to 0.3%, which could become another argument for the Fed when considering future monetary policy decisions.

According to the CME Group FedWatch Tool, most analysts believe the regulator will leave interest rates unchanged despite pressure from the White House. The strong September labor market report released last week also supports this view, although the data still reflected a rise in unemployment to 4.4%. At the same time, November data will be released after the final meeting of the year and will therefore have little impact on the decision. In Australia, Wednesday at 02:30 (GMT+2) will bring CPI data, which currently stands at 3.5%. Analysts do not expect a significant slowdown. Confirmation of these expectations will serve as a signal for the Reserve Bank of Australia to keep borrowing costs unchanged, as officials are not inclined to rush further adjustments.

USD/JPY

The US dollar is trading with near-zero dynamics in the USD/JPY pair around 156.63. The instrument ended last week with moderate gains and also updated its record January highs. Among other factors, pressure on the US currency came from data on inflation expectations from the University of Michigan, which showed that the one-year forecast fell significantly from 4.7% to 4.5%, and the five-year outlook declined from 3.6% to 3.4%. This signals greater room for the Federal Reserve to potentially reduce borrowing costs.

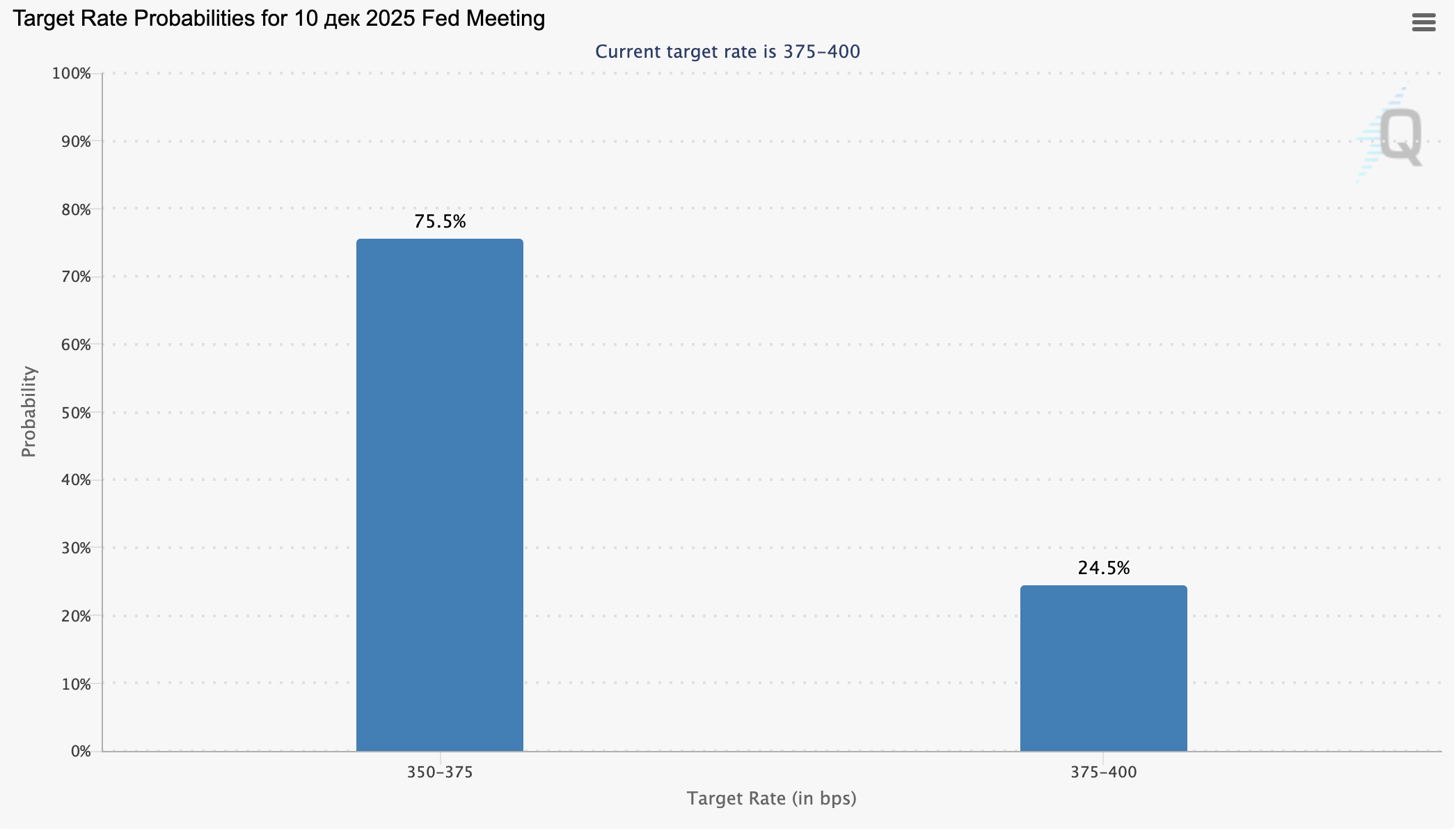

According to the CME Group FedWatch Tool, around 75.0% of surveyed analysts believe that the key rate will remain at the current level of 3.75–4.00%. However, much will depend on incoming macroeconomic data over the coming weeks. Meanwhile, the yen remains under pressure due to growing uncertainty surrounding the Bank of Japan’s monetary policy, continuing its strong downward trend since Sanae Takaichi’s appointment as prime minister.

As of today, the national currency is the worst performer among its peers in the G10, sharply increasing the risk of new interventions by the regulator, which has previously used this mechanism repeatedly to influence market conditions. Takaichi is known as a supporter of a dovish stance, as this is required for the intended fiscal reforms. On Friday at 01:30 (GMT+2), November CPI data for the Tokyo region will be released. Forecasts suggest that the annual figure may slow from 2.8% to 2.7%, weakening expectations of potential tightening at the December Bank of Japan meeting. In addition, at 01:50 (GMT+2), October industrial production and retail sales data will be published. On a monthly basis, industrial output is expected to decline by 0.6% after an increase of 2.6%, while retail sales may rise by 0.8% following a 0.5% increase the previous month.

XAU/USD

The XAU/USD pair is slightly declining, testing the 4045.00 level for a downside breakout while awaiting new market drivers. Overall, gold prices changed only marginally last week as investors assessed a series of macroeconomic releases related to the US labor market. Non-farm payrolls increased by 119.0 thousand compared to expectations of 50.0 thousand, while the unemployment rate adjusted upward from 4.3% to 4.4%.

At the same time, initial jobless claims fell by 8.0 thousand to 220.0 thousand, while continuing claims rose from 1.946 million to 1.974 million.

Additional support for the US dollar came from data on existing home sales, which accelerated by 1.2% in October after a 1.3% increase in September. In absolute terms, volumes rose from 4.05 million to 4.10 million, beating expectations of 4.08 million. Last Friday, November business activity data from S&P Global was also in focus. The manufacturing index declined from 52.5 to 51.9 points versus expectations of 52.0, while the services index rose from 54.8 to 55.0 points. Inflation expectations from the University of Michigan for the one-year horizon were adjusted downward from 4.7% to 4.5%, while the five-year forecast was lowered from 3.6% to 3.4%.

As a result, pressure on the Federal Reserve to further reduce borrowing costs has eased somewhat: the labor market remains resilient, while inflation risks are still significant. Meanwhile, demand for gold remains relatively high amid geopolitical risks stemming from conflicts in South America and Eastern Europe.