The regulator is also expected to release updated macroeconomic forecasts for the near term. Some analysts do not rule out the possibility of a more aggressive easing during the September meeting, although the probability of such an outcome is currently estimated at only 5.0–6.0%.

On Monday, US President Donald Trump again urged Fed Chair Jerome Powell to act more decisively, citing concerns over the housing market. Recently published macro data provided moderate support for the dollar: retail sales in August rose 0.6% versus expectations of –0.2%, while the ex-auto figure accelerated from 0.4% to 0.7%. Industrial production increased 0.1% in August after –0.4% the previous month. Meanwhile, the German ZEW economic sentiment index rose from 34.7 to 37.3 points in September, beating forecasts of 27.3. The eurozone-wide index improved from 25.1 to 26.1 against expectations of 20.3. Industrial production in the region jumped from 0.7% to 1.8% in July, above the 1.7% forecast, largely due to higher defense spending amid ongoing challenges in Eastern Europe.

GBP/USD

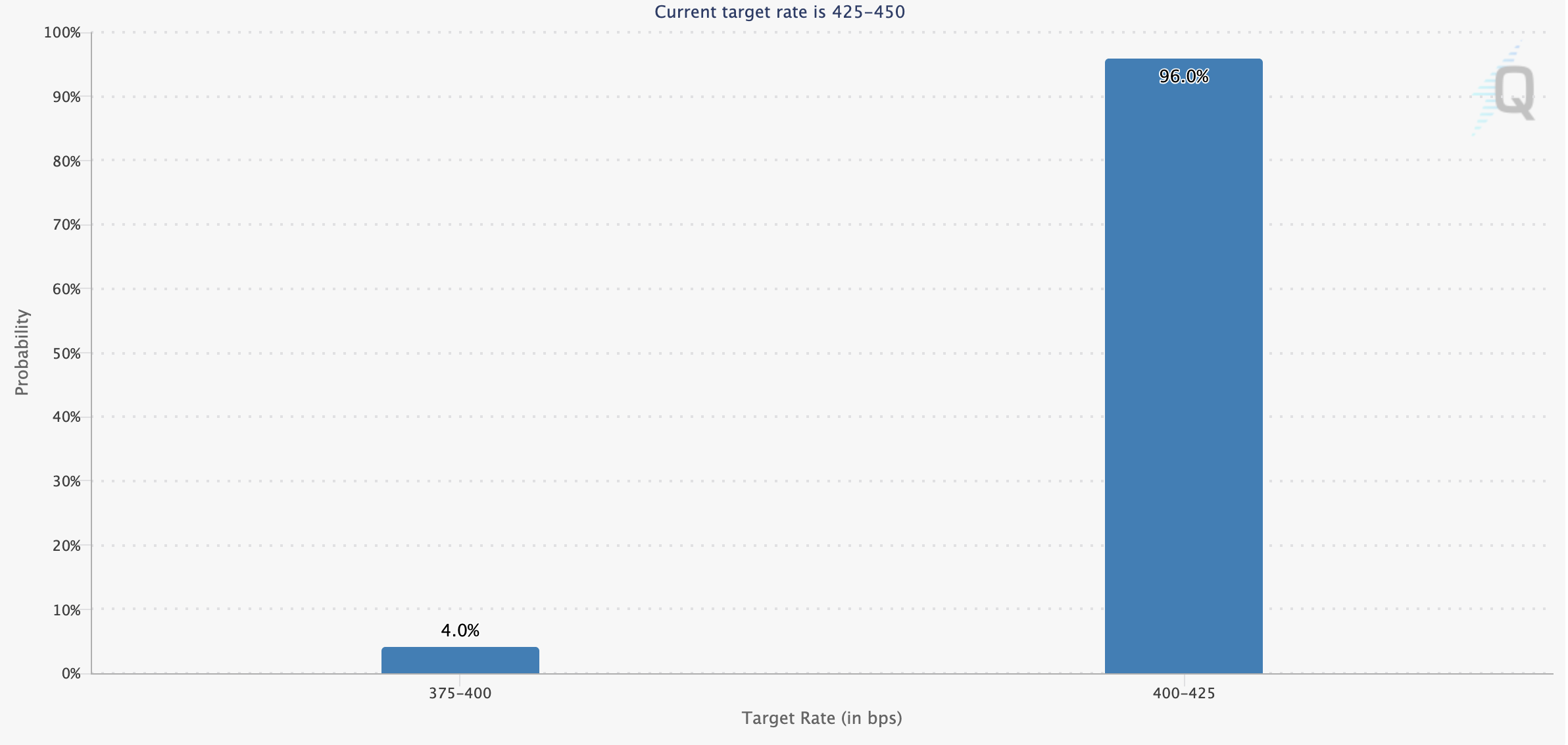

The pound shows mixed dynamics against the dollar during the morning session, holding near 1.3650, where it set a local high on July 4. Market activity remains subdued ahead of today’s Fed decision at 20:00 (GMT+2), where a 25 basis point rate cut to 4.25% is expected. Officials will also present new macro forecasts and inflation expectations. Fed Chair Jerome Powell remains under pressure as President Trump continues to call for more aggressive easing. Tomorrow at 13:00 (GMT+2) the Bank of England meets, though no policy changes are expected given high inflation and ongoing uncertainty. Data released earlier showed core CPI slowing from 3.8% to 3.6% y/y, while the broader figure held at 3.8% versus 3.9% expected. Monthly inflation rose from 0.1% to 0.3%. Retail prices slipped from 4.8% to 4.6% y/y, while monthly growth held at 0.4% instead of rising to 0.5% as anticipated.

AUD/USD

The Australian dollar is weakening against the US dollar, pulling back from November highs and testing support at 0.6675 during the Asian session. Traders await the Fed’s decision at 20:00 (GMT+2). Markets mostly expect a 25 basis point cut to 4.25%, which is already priced in. Updated macro forecasts and inflation outlooks will also be released. Previous projections suggested 3.6% inflation over the next year, 3.4% over two years, and 3.1% over three. Pressure on the Fed continues from the White House, as Trump again urged Powell to cut rates by more than 25 bps, citing cooling growth and housing weakness. Additional pressure on the aussie comes from August leading indicators, which fell 0.1% after a 0.14% gain previously. On Thursday at 03:30 (GMT+2), labor market data will be released: forecasts point to a 22,000 gain in employment after a 24,500 rise previously, with unemployment steady at 4.2%.

USD/JPY

The dollar is trading flat against the yen, consolidating near 146.40 and revisiting lows last seen on August 14. Investors are waiting for the Fed’s decision today at 20:00 (GMT+2). The regulator is widely expected to cut rates by 25 bps to 4.25%. Powell earlier signaled that labor market weakness should offset the inflationary effects of Trump’s import tariffs. This September rate cut was made possible largely due to weak labor data released earlier in the week. Revised figures showed employment growth over the past year was 911,000 lower than initially reported, pointing to a deeper slowdown. The Bank of Japan meets on Friday, but no policy changes are expected. Officials will likely stick to a wait-and-see stance despite CPI above 3.0%. Political developments also weigh in, as Agriculture Minister Shinjiro Koizumi and former LDP Secretary General Toshimitsu Motegi entered the race for prime minister. The official campaign begins September 22, with voting on October 4. Data from Japan showed August exports fell 0.1% after –2.6% previously, while imports declined 5.2% after –7.4%, leaving a trade deficit of –¥242.5 billion versus expectations of –¥513.6 billion.

XAU/USD

Gold is consolidating near record highs around 3676.00 ahead of the Fed’s decision today at 20:00 (GMT+2). A 25 bps cut is expected, but since this is already priced in, volatility may instead come from updated forecasts and Powell’s tone. A focus on inflation risks would imply caution, while an emphasis on labor and housing weakness could suggest a more dovish path. Either way, lower rates increase gold’s appeal, as it yields no interest. Markets also watch today’s Bank of Canada meeting at 15:45 (GMT+2), where a cut from 2.75% to 2.50% is expected. Later this week, the Bank of England (Thursday) and Bank of Japan (Friday) also meet, with no changes anticipated, though commentary remains key. At 14:30 (GMT+2) US housing data is due: housing starts are seen falling from 1.428M to 1.37M, while building permits may rise slightly from 1.362M to 1.370M.