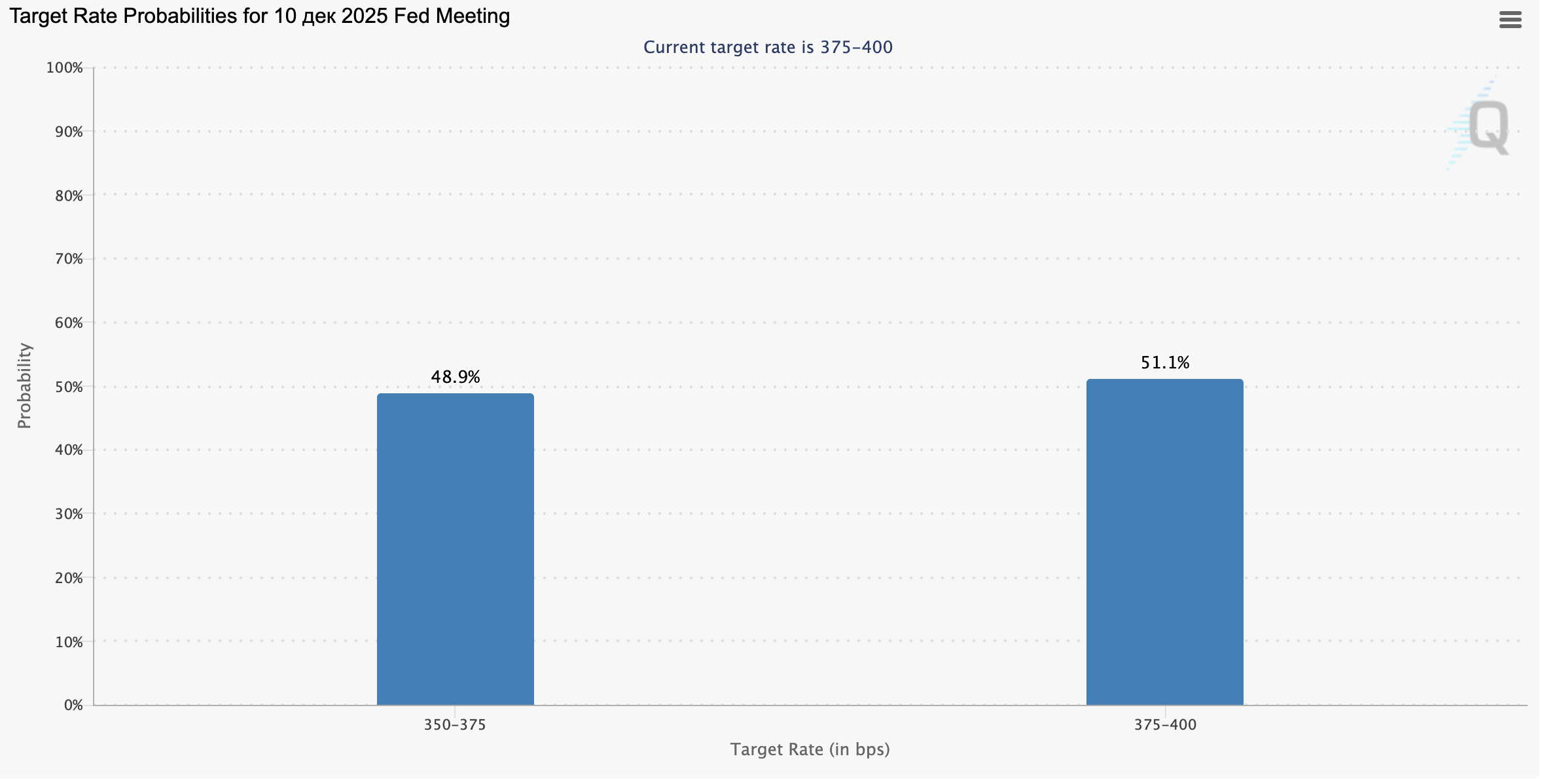

Consensus forecasts suggest that core CPI for October will hold at 2.4%, while the headline index is expected to edge up by 2.1%. However, these readings are unlikely to materially change expectations around the European Central Bank’s monetary policy path. The ECB has effectively brought its dovish cycle to a close and is now more focused on growth dynamics and labour market conditions. At the same time, the outlook for further policy easing by the US Federal Reserve remains a key driver for traders. According to the CME Group FedWatch Tool, the probability of a 25 bp rate cut in December has fallen to around 42.0% and could decline further once the October meeting minutes and fresh US labour-market data — due later this week — are fully digested.

The US federal government only recently resumed full operations after President Donald Trump signed a stopgap funding bill extending the budget through 30 January 2026. The core political dispute between Republicans and Democrats that triggered the shutdown, however, remains unresolved. In December, Congress is expected to vote on extending subsidies under the Affordable Care Act (Obamacare), which are due to expire at year-end. On Thursday at 15:30 (GMT+2), markets will receive the delayed September nonfarm payrolls report. Economists anticipate a gain of 50.0K jobs after an increase of 22.0K in the prior month, with the unemployment rate likely holding at 4.3%. Average hourly earnings are forecast to remain at 0.3% m/m and 3.7% y/y. A print broadly in line with expectations would strengthen the case for the Fed to keep policy unchanged in December.

GBP/USD

The pound is trading close to flat against the US dollar near the 1.3150 mark, as investors and FX traders digest the latest UK macro data that could prove pivotal for the Bank of England’s next moves. In October, headline CPI slowed from 3.8% to 3.6% y/y, while monthly inflation accelerated by 0.4% after a flat reading in September. Core inflation eased from 3.5% to 3.4%, matching forecasts. Market participants also focused on retail price dynamics: the RPI fell from 4.5% to 4.3% y/y, while the monthly figure rebounded from –0.4% to 0.3%.

Stubbornly high inflation remains the main obstacle preventing the BoE from pushing more aggressively into a dovish cycle. The domestic economy is too fragile for policymakers to simply “wait and see” until price growth returns to the 2% target. Complicating matters further, the UK steel industry is under serious pressure following a sharp increase in EU tariffs. Last month, Brussels signalled plans to almost halve existing duty-free quotas on imported steel and to raise tariffs by a further 50% on volumes above those thresholds.

This is particularly negative for UK steel and aluminium producers, given that more than 70% of their exports go to EU countries. London has already warned it may consider retaliatory measures, raising the risk of an escalating trade dispute. Across the Atlantic, US investors will be focused on the minutes of the October FOMC meeting, due at 21:00 (GMT+2). At that meeting on 28–29 October, the Fed cut rates by 25 bps to 4.00%, prompting many participants to assume another reduction in December was all but guaranteed. Later, Chair Jerome Powell cautioned that further easing was neither pre-committed nor risk-free, especially in the context of limited fresh data.

AUD/USD

The Australian dollar is under pressure against the US dollar, sliding back toward Tuesday’s local lows. The AUD/USD pair is testing 0.6480 to the downside as markets brace for the release of the October FOMC minutes at 21:00 (GMT+2), which could further dampen expectations of another Fed rate cut before year-end. Powell has repeatedly warned markets not to overprice an extended easing cycle, and, as a result, the implied probability of a December cut in Fed funds has drifted down toward 42.0%, according to the CME FedWatch Tool.

Much will also depend on incoming US data, particularly labour-market releases that were delayed during the recent US government shutdown. Meanwhile, traders are still assessing the minutes from the November Reserve Bank of Australia meeting published earlier this week. As expected, they provided moderate support for the Australian dollar by signalling a more cautious approach to further easing. Policymakers indicated that the cash rate could remain unchanged for longer than previously anticipated. Last week’s October employment report helped temper expectations for additional cuts: the figures showed a solid labour market.

Fresh data released today pointed to steady wage growth, with the Q3 wage price index rising 0.8% q/q and 3.4% y/y. In addition, Westpac’s leading index rose 0.1% in October after a 0.03% decline, hinting at slightly improved forward-looking conditions for the Australian economy.

USD/JPY

The US dollar is posting a modest decline against the yen, consolidating just below the February highs that were updated on Tuesday. The USD/JPY pair is currently testing 155.30 to the downside as investors wait for fresh catalysts. The minutes of the October FOMC meeting, due at 21:00 (GMT+2), could clarify the likelihood of a December rate cut. On Thursday at 15:30 (GMT+2), markets will also receive long-delayed US labour data that were postponed due to the federal shutdown.

Following protracted negotiations, US lawmakers agreed on a temporary funding bill that keeps the government open until 30 January 2026, which President Trump signed last week. Forecasts point to a 50.0K gain in nonfarm payrolls after a 22.0K increase previously, with average hourly earnings expected to hold at 0.3% m/m and 3.7% y/y and unemployment at 4.3%. In Japan, traders will focus on Friday’s October inflation and trade figures due at 01:30 (GMT+2). The core national CPI excluding fresh food is projected to edge up from 2.9% to 3.0%, potentially providing the Bank of Japan with an additional argument in favour of further rate hikes. Later this week, markets also expect the first economic reform proposals from the new Prime Minister Sanae Takaichi, who has previously advocated a looser monetary stance.

XAU/USD

The XAU/USD pair is moving moderately higher, once again approaching resistance at 4100.00 with an eye on an upside breakout. Gold is benefitting from a brief lull in risk events, allowing buyers to regain some control. That said, the release of the October FOMC minutes at 21:00 (GMT+2) could have a tangible impact on precious metals if they reinforce Chair Powell’s cautious tone and his reluctance to pre-commit to another rate cut in December amid persistent inflation risks.

On Thursday at 15:30 (GMT+2), the long-delayed September nonfarm payrolls report will hit the wires. Economists expect a 50.0K rise in employment after a 22.0K gain in the prior month, with unemployment likely steady at 4.3% and average hourly earnings at 0.3% m/m and 3.7% y/y. A print in line with forecasts would strengthen the case for the Fed to leave policy unchanged, which could support the dollar and cap further gold gains. For now, traders have only partial labour-market indicators to rely on. Data from Automatic Data Processing (ADP) for the last four weeks showed employment falling by 2.5K after a prior decline of 11.25K. In addition, yesterday’s jobless-claims figures surprised to the upside: initial claims jumped from 219K to 232K, while continuing claims rose from 1.926M to 1.957M, indicating a gradual cooling of the US labour market.