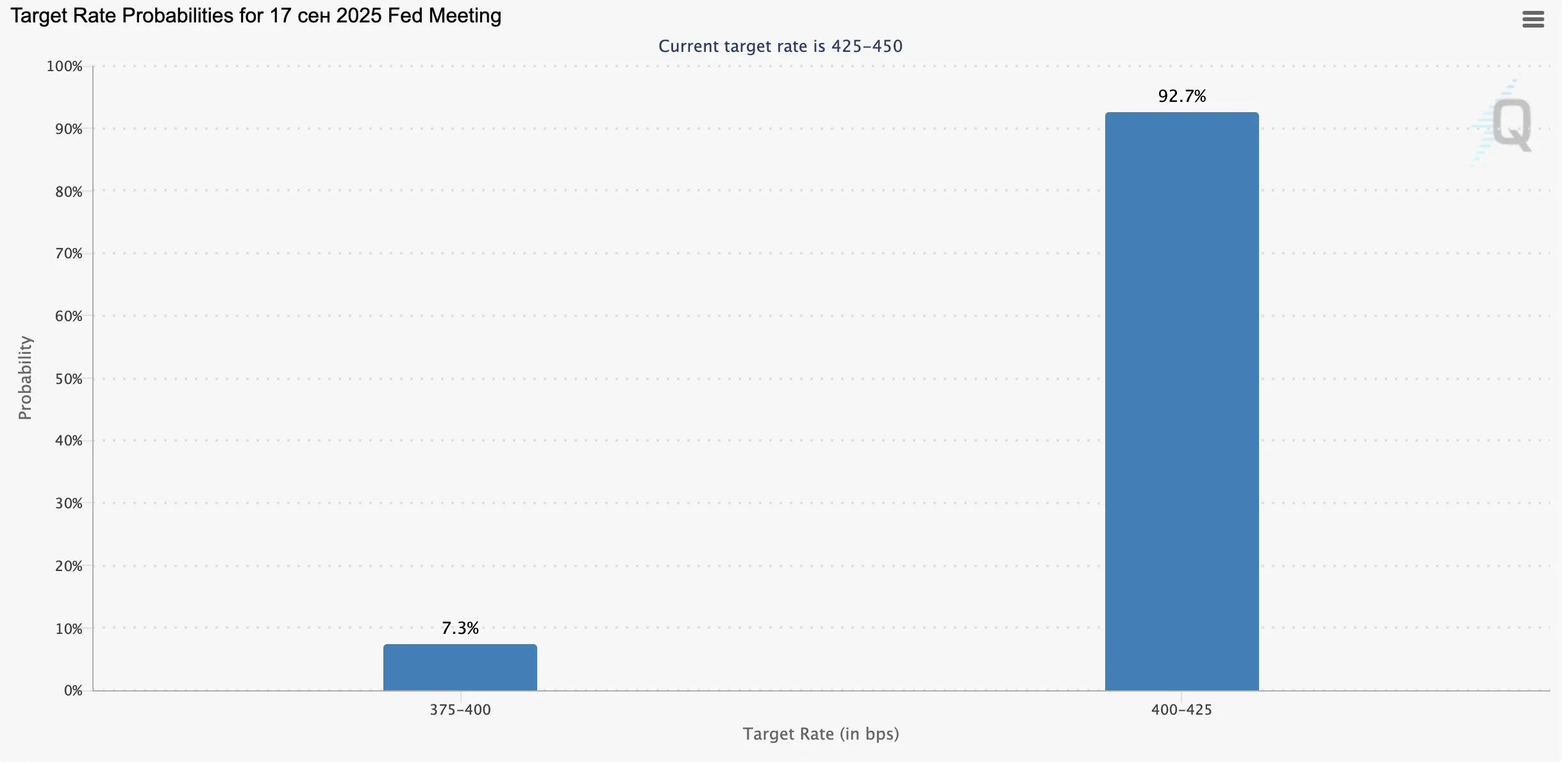

Forex investors are assessing macroeconomic statistics: in August, the consumer price index increased from 2.7% to 2.9%, below the 3.0% target range, which relieves the Federal Reserve of the need to tighten monetary policy in response to inflation accelerated by the tariff policies of the White House Republican administration, and reduces the probability of a 50-basis-point rate cut to 7.5%, according to the Chicago Mercantile Exchange (CME) FedWatch Tool. On the other hand, the labor market continues to cool: after weak employment data, jobless claims rose from 236,000 to 263,000, the highest in four years, requiring economic stimulus through a 25-basis-point rate adjustment.

Eurozone

The euro is strengthening against the pound and the yen but shows mixed performance against the U.S. dollar.

After the decision of the European Central Bank (ECB) to keep the key rate at 2.15%, the deposit rate at 2.00%, and the marginal lending rate at 2.40%, ECB President Christine Lagarde noted that the current state of the economy is in line with forecasts. Over the past month, pressure from two key negative factors has eased significantly: the likelihood of retaliatory tariffs on U.S. goods has decreased, while their rate has stabilized at 15.0%, with consultations on possible adjustments still ongoing.

United Kingdom

The pound is declining against the U.S. dollar and the euro but strengthening against the yen.

Contrary to analysts’ expectations, performance in key sectors of the economy has weakened significantly. As a result, in July, gross domestic product (GDP) fell from 0.4% to 0.0% month-over-month and remained at 1.4% year-over-year, below the forecast of 1.5%. Real estate slowed from 0.3% to 0.2%, industrial output dropped from 0.7% to –0.9%, and manufacturing fell from 0.5% to –1.3%.

Japan

The yen is weakening against the U.S. dollar, the pound, and the euro.

Investors are assessing the August corporate goods price index and July industrial production, which fell from 0.3% to –0.2% and from 2.1% to –1.2% respectively. As a result, the Bank of Japan will likely delay tightening monetary policy for another month. Officials estimate that although the economy has slowed, it is withstanding U.S. tariff pressure, allowing room for another rate hike later this year. The Fed’s rhetoric at its September 17 meeting will likely influence the BoJ’s decision.

Australia

The Australian dollar is strengthening against the yen but weakening against the U.S. dollar, the pound, and the euro.

The positive trend is supported by data on the national economy: in the second quarter, employment in the tourism sector fell by 0.6% or 3,900 to 702,800 quarter-over-quarter but grew by 4.6% or 30,900 year-over-year. At the same time, full-time employment increased by 13,000 to 348,900, and part-time employment rose by 17,900 to 353,900.

Oil

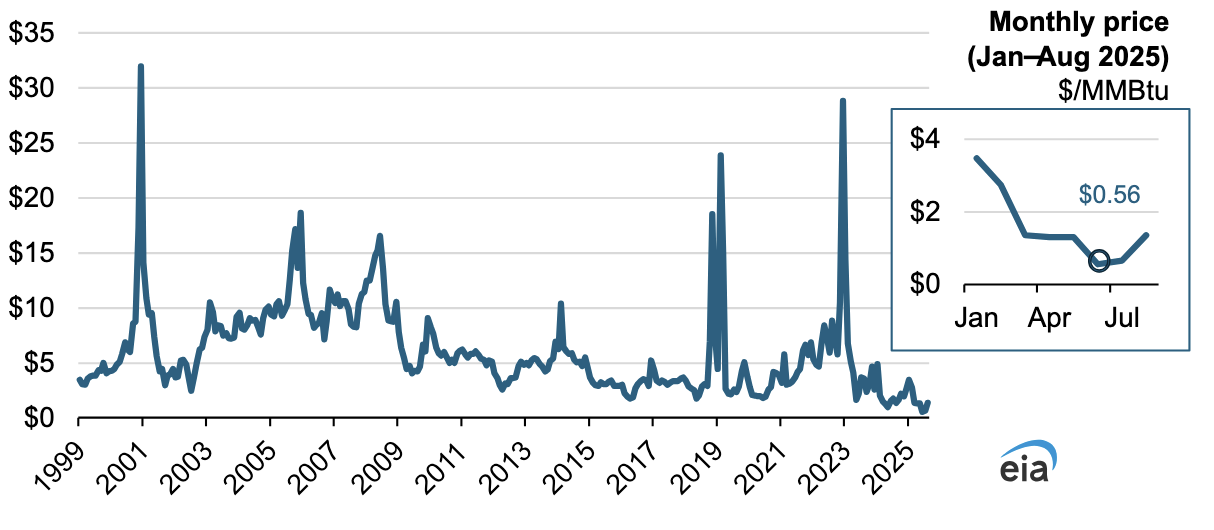

Oil prices are approaching the key monthly level of 67.00: crude production is falling, in line with U.S. Energy Information Administration (EIA) forecasts. The main driver of this dynamic is not high supply but inflation accelerating to 2.9%, which is slowing production.

Meanwhile, the White House plans to reduce the supply of cheap Russian energy to the market, putting pressure on the two largest importers — India and China. A G7 finance ministers’ videoconference is scheduled for today, where Washington will push for its plan to impose 50.0–100.0% tariffs on these countries if they do not halt Russian oil purchases. Although most alliance members oppose further escalation, a sanctions decision could still be made.