The market remains focused on the outcome of the Federal Reserve meeting, where the policy rate was cut by 25 basis points to 4.25%. The move had little impact on the dollar because it was already fully priced in.

The Fed’s updated GDP projections came in stronger than analysts expected, helping the dollar extend its upward momentum. Officials now see 1.6% growth in 2025 (0.2 pp above the prior estimate) and 1.8% in 2026 (previously 1.6%). The greenback was also supported by last week’s labor data: initial jobless claims for the week ended September 12 fell to 231,000 from 264,000 (consensus 240,000), while continuing claims dipped to 1.920 million from 1.927 million (vs. 1.950 million expected). The Philadelphia Fed Manufacturing Index surprised to the upside as well, jumping to 23.2 in September from –0.3.

Eurozone traders now look to Tuesday’s September PMI prints from S&P Global and Hamburg Commercial Bank (HCOB) at 10:00 (GMT+2). Forecasts call for the services PMI to edge down to 50.2 from 50.5, and manufacturing to tick up to 50.8 from 50.7. In Germany, the composite picture is seen improving slightly, with the manufacturing PMI expected at 50.0 from 49.8.

GBP/USD

Sterling is weakening against the U.S. dollar in morning trading, hovering near 1.3470 and the September 5 local lows amid subdued market activity.

Today at 14:30 (GMT+2) Bank of England Chief Economist Huw Pill speaks, followed by Governor Andrew Bailey at 20:00 (GMT+2). Last week, the BoE held rates at 4.00%, with seven of nine MPC members voting to keep policy unchanged and two (Swati Dhingra and Alan Taylor) favoring a 50 bps cut. The statement noted significant progress on inflation, though price growth remains above desired levels. The annual CPI stayed at 3.8% in August, the highest since January 2024.

The BoE does not rule out a temporary re-acceleration of inflation in September, before a renewed move toward the 2.0% target. Investors also digested August retail sales: ex-fuel, the annual rate accelerated to 1.2% from 1.0% (vs. 0.8% expected) and the monthly reading rose to 0.8% from 0.4% (vs. 0.3% expected). The broader measure eased to 0.7% from 0.8% year over year and printed 0.5% month over month.

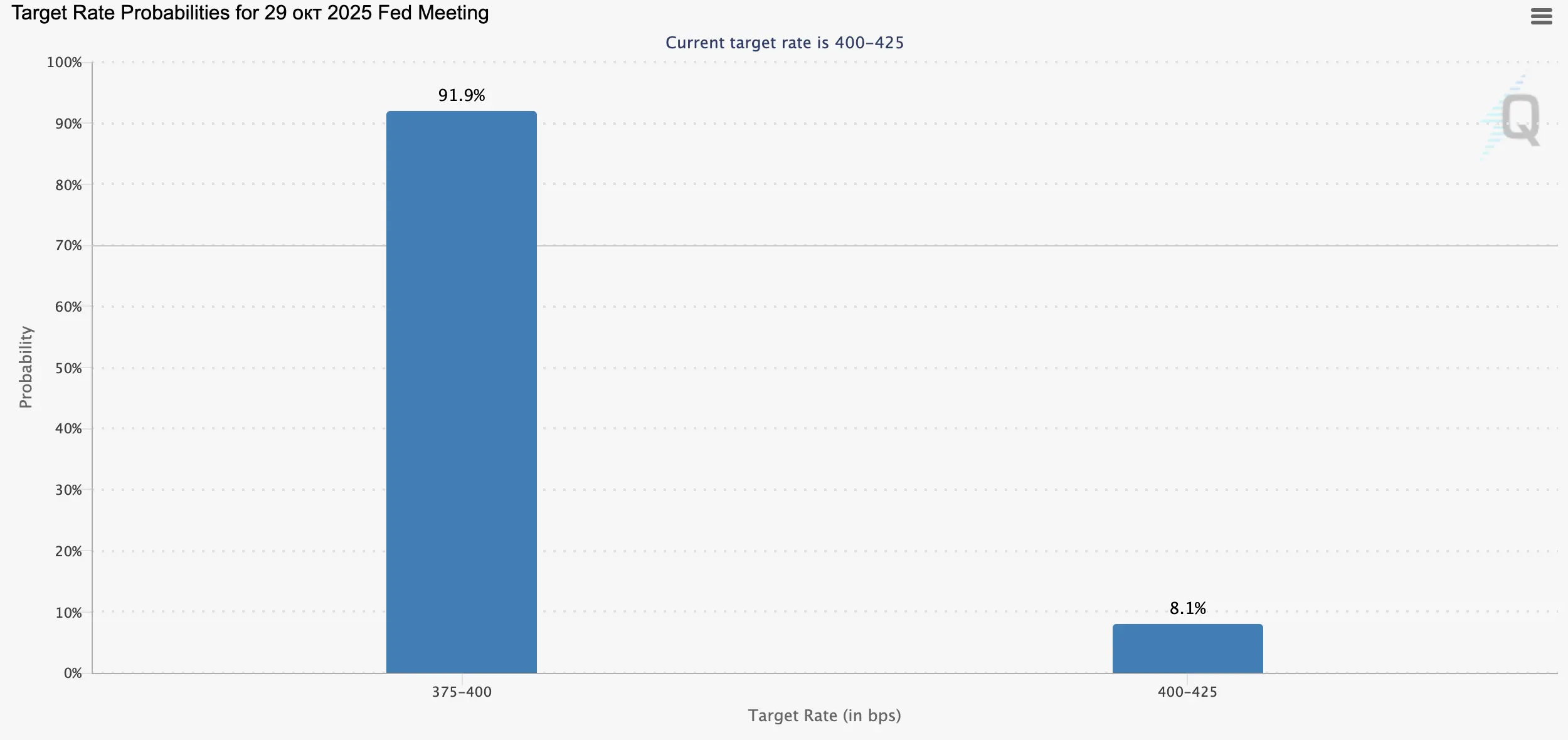

Meanwhile, the Fed’s 25 bps cut last week did not dent the dollar; instead, markets focused on improved U.S. growth projections, assuming the Fed may need less time to implement its policy path. Even so, markets still price in as many as two more 25 bps cuts this year.

NZD/USD

The New Zealand dollar is trading mixed against the U.S. dollar in the morning session, attempting to extend last week’s strong bearish trend and now testing the September 5 lows. On September 17, the Fed concluded its two-day meeting by cutting rates 25 bps to 4.25%. Officials signaled caution on further easing due to persistent uncertainty around inflation.

Fed Chair Jerome Powell warned that the administration’s aggressive tariff policy could trigger at least a short-lived rise in consumer prices. Even so, the Fed is optimistic on growth prospects: 2025 GDP is seen at 1.6% (revised up from 1.4%), and 2026 at 1.8% (from 1.6%). Unemployment is projected at 4.5% in 2025, easing to 4.4% in 2026—still relatively elevated.

NZD came under pressure Thursday after weaker macro data. Second-quarter GDP contracted 0.6% year over year (consensus 0.0%), while quarterly output fell 0.9% after a similar-sized rise previously (consensus –0.3%), weighed by soft manufacturing and export activity amid U.S. tariff headwinds. Trade figures also disappointed late last week: August exports fell to $5.94 billion from $6.56 billion, and imports to $7.12 billion from $7.27 billion. The monthly trade deficit widened to –$1.18 billion from –$716 million (vs. –$746 million expected), while the annual deficit narrowed to –$2.99 billion from –$4.12 billion.

USD/JPY

The U.S. dollar is edging higher against the Japanese yen in Asia, extending the very short-term uptrend that began last Wednesday after the Fed meeting. As expected, the Fed cut rates by 25 bps to 4.25% and upgraded its GDP outlook to 1.6% for 2025 (from 1.4%) and 1.8% for 2026 (from 1.6%). Powell was cautious on further easing but left the door open as inflation stabilizes.

The Bank of Japan also met last week, keeping its policy rate at 0.50%, with two MPC members proposing a hike to 0.75%. Officials additionally announced plans to sell ETF holdings worth ¥330 billion and J-REITs worth ¥5 billion. Markets still expect a 25 bps BoJ rate increase in October or December. Inflation data showed national CPI slowing to 2.7% from 3.1% year over year, with core ex-food and energy at 3.3% from 3.4%, complicating the BoJ’s tightening path. On Friday at 01:30 (GMT+2), Tokyo inflation prints are due; the ex-fresh-food gauge is seen rising to 2.8% in September from 2.5%.

XAU/USD

XAU/USD is posting modest gains in early trading, extending Friday’s bullish impulse. The pair is once again testing the psychological 3700.00 resistance to the upside as traders digest last week’s policy decisions from the Fed, Bank of Canada, Bank of England, and Bank of Japan. The U.S. and Canadian central banks both delivered expected 25 bps cuts amid cooling growth and softer labor conditions.

The slowdown was particularly evident in the U.S., where the annual benchmark revision (through March 2025) showed payrolls 911,000 lower than previously reported. By contrast, the BoE and BoJ left their policies unchanged. Analysts still expect the BoE to resume easing before long, despite elevated inflation, while the BoJ may attempt at least one more 25 bps hike before year-end.

Safe-haven demand for gold is also supported by ongoing geopolitical risks. Several EU countries last week issued statements recognizing Palestinian statehood, drawing sharp criticism from Israel amid its current military operation in Gaza. Tensions around Venezuela remain high, and U.S. President Donald Trump warned of consequences for Afghanistan if it does not return the Bagram airbase vacated by U.S. forces in 2021.