Against this backdrop, investors and Forex traders are bracing for a wave of macroeconomic releases, primarily labor market data. For now, they have to rely on the employment report from Automatic Data Processing (ADP): as expected, the indicator fell by 11.25K after a previous increase of 14.25K. In the eurozone, September industrial production data will be published today at 12:00 (GMT+2). Forecasts suggest that annual growth may accelerate from 1.1% to 2.1%, driven by a sharp rise in military and infrastructure spending in Germany, while output adjusted for seasonality could add 0.7% in September after a 1.2% decline the month before. Yesterday, the market received fresh inflation data from Germany, but traders remain confident that consumer prices in the region are under control, so minor fluctuations are unlikely to prompt the European Central Bank (ECB) to adjust its current monetary policy settings. In any case, the harmonized consumer price index for October rose by another 0.3% month-on-month and 2.3% year-on-year.

GBP/USD

The pound is trading flat in the GBP/USD pair as investors digest today’s batch of UK macroeconomic data. In particular, third-quarter gross domestic product (GDP) figures showed a slowdown from 0.3% to 0.1% q/q versus expectations of 0.2%, and from 1.4% to 1.3% y/y. Industrial production for September also deteriorated sharply: in annual terms the indicator fell from –0.7% to –2.5% versus a forecast of –1.2%, and in monthly terms from 0.3% (revised from 0.4%) to –2.0%, while analysts had expected just –0.2%. The drop was largely driven by new EU tariffs on steel and aluminum imports. It is also worth noting that pressure on the pound persists after Tuesday’s wage data: including bonuses, pay growth slowed from 5.0% to 4.8% compared with preliminary estimates of 4.9%, and excluding bonuses from 4.7% to 4.6%. Traders and Forex market participants also focused on the unemployment rate, which rose from 4.8% to 5.0%. Combined with planned tax hikes in the UK’s autumn budget, this is likely to become a strong argument in favor of further rate cuts by the Bank of England: there is a real chance that policymakers could trim borrowing costs by 25 basis points as early as December.

AUD/USD

The Australian dollar is gaining ground in the AUD/USD pair, extending a strong short-term bullish trend. The instrument is testing the 0.6555 level to the upside as traders focus on Australia’s October labor market report. Seasonally adjusted employment rose by 42.2K after a 12.8K increase the previous month, well above expectations of 20.0K. Full-time employment surged by 55.3K after 6.5K previously, while part-time employment fell by 13.1K after a 6.3K gain in September. The unemployment rate dropped from 4.5% to 4.3%, beating forecasts of 4.4%. A strong labor market will provide the Reserve Bank of Australia (RBA) with a solid argument in any future decisions on monetary policy. The regulator is in no hurry to cut rates further, fearing an acceleration in inflation.

U.S. investors, meanwhile, are tracking inflation statistics, which may be released today following the end of the record 43-day shutdown. After Congress approved a bill to temporarily fund the federal government through the end of January 2026, it passed the House of Representatives and was later signed by President Donald Trump. Now a large volume of delayed macroeconomic data will hit the market, with the main focus on labor market conditions.

USD/JPY

The U.S. dollar continues to move higher in the USD/JPY pair, testing the 154.80 level to the upside during the Asian session. The yen is once again updating nine-month lows and remains under pressure even after the release of October producer inflation data: on an annual basis, the indicator slowed from 2.8% to 2.7%, while analysts had expected 2.5%, and in monthly terms from 0.5% to 0.4%. External trade uncertainty is intensifying following the election of Sanae Takaichi as Japan’s new prime minister. She advocates a looser monetary policy, in contrast to the Bank of Japan, which has only just begun a hawkish cycle. Another rate hike could stabilize the national currency but carries multiple risks, including the threat of deflation. If the authorities avoid tightening, the yen may continue its downward trend, forcing the regulator to intervene in the FX market, as it has done in the past.

Some support for the yen yesterday came from machinery orders data: in October, orders jumped 16.8% after an 11.0% increase the previous month, while analysts had expected 9.9%. At the same time, investors are awaiting the formal end of the U.S. shutdown, which will trigger the release of numerous macroeconomic reports that were postponed while the federal government was closed. Labor market data will be in the spotlight, as they are critical for the U.S. Federal Reserve in determining its policy path. Previously, Fed Chair Jerome Powell once again stressed that a December rate cut is far from guaranteed. Moreover, he called such a move “risky,” clearly hinting at a lack of sufficient data.

XAU/USD

The XAU/USD pair is consolidating near the new local highs set on October 21. Market sentiment remains cautious as investors prepare for a flood of U.S. data in the wake of the shutdown’s end. President Donald Trump signed a bill to temporarily fund the federal budget through the end of January 2026, allowing federal agencies to resume operations, while previously furloughed employees will be reinstated. Against this backdrop, investors may once again raise the probability of monetary easing by the U.S. Federal Reserve at its December 9–10 meeting.

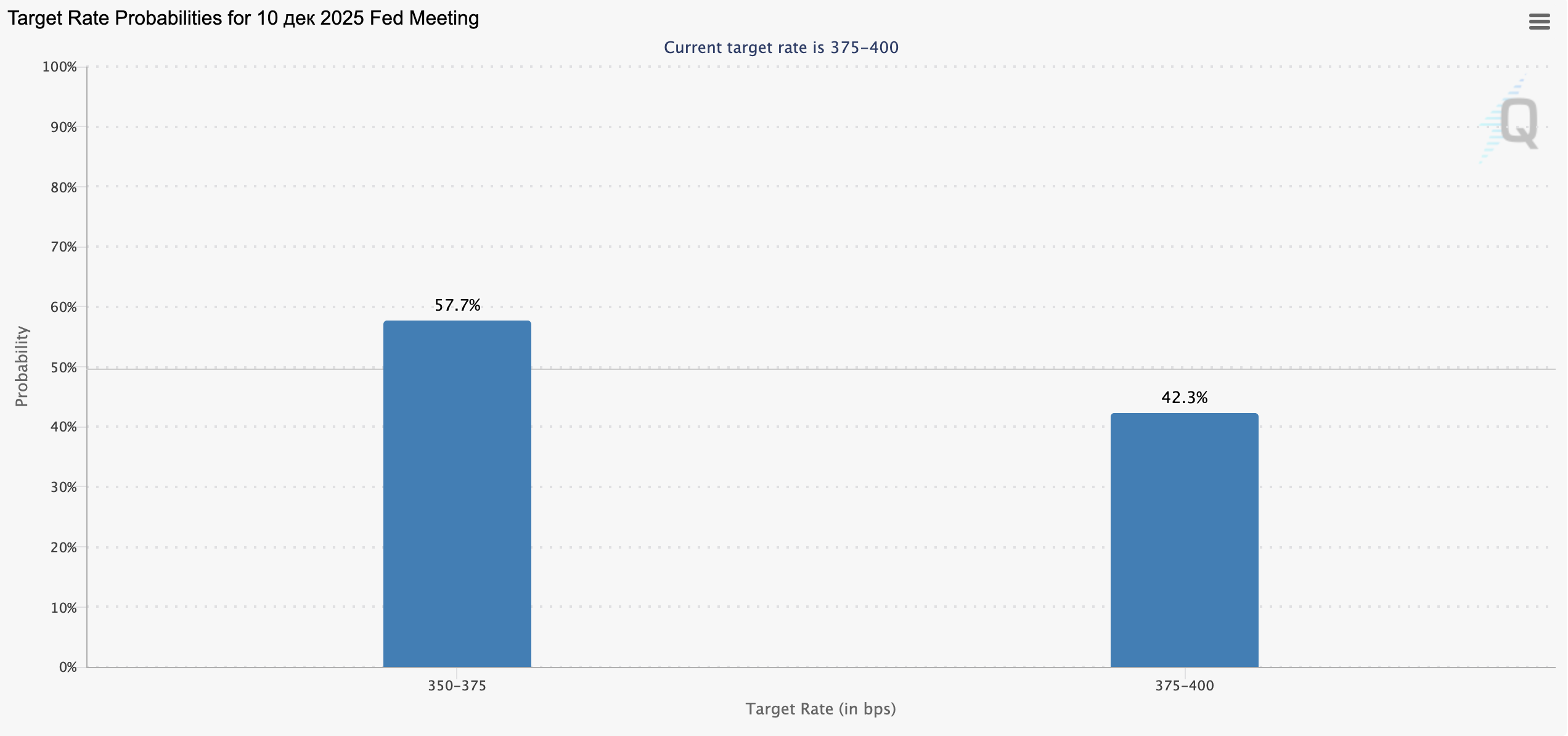

At the moment, according to the CME Group’s FedWatch Tool, roughly 57.0% of experts expect the regulator to cut the key rate by 25 basis points to 3.75%. The situation should become clearer once the first labor market reports are released, since employment data were previously the main argument in favor of starting the current dovish cycle. At the same time, some analysts fear that once the government funding issue is resolved, the White House may return to a more aggressive foreign policy stance.

In particular, U.S. armed forces remain positioned close to the coast of Venezuela, where experts do not rule out the possibility of limited military operations. Today, investors will be closely watching October inflation figures: the annual consumer price index is expected to print at 3.0%, while the monthly reading is forecast to slow from 0.3% to 0.2%. The core index, by contrast, is expected to accelerate from 0.2% to 0.3%.