Today at 11:30 (GMT+2), traders will focus on the November investor confidence index from Sentix, while on Tuesday at 12:00 (GMT+2) Germany and the Eurozone will release the ZEW economic sentiment indices. Forecasts suggest that Germany’s index will rise from 39.3 to 42.5 points, likely due to growing business activity supported by large-scale EU and Bundestag infrastructure projects and increased defense investments.

In the Eurozone, the corresponding index is expected to rise from 22.7 to 23.5 points. On Wednesday at 09:00 (GMT+2), Germany will release October inflation data. Analysts expect little change, with the annual CPI at 2.3% and the monthly figure at 0.3%. Inflation in the Eurozone remains a secondary issue for now, as the European Central Bank (ECB) has nearly completed its dovish cycle. Traders anticipate at most one more rate cut of 25 basis points either late this year or early next year. The US dollar, in turn, received another boost last week after comments from Fed Chair Jerome Powell, who described further monetary easing as “risky.” Investors also focused on private-sector employment data since the official Nonfarm Payrolls report was again delayed due to the federal government shutdown. ADP reported an increase of 42,000 jobs in October after a 29,000 decline in September, exceeding the expected 25,000. Later, Challenger, Grey & Christmas reported that announced corporate layoffs surged from 54,060 to 153,070 in October, reflecting a worrying trend of mass layoffs linked both to the shutdown and to the rise of artificial intelligence technologies.

Forex: GBP/USD

The British pound is losing ground against the US dollar, holding near 1.3150 and early November highs. Bullish activity remains moderate as traders are reluctant to open new positions ahead of Tuesday’s (09:00 GMT+2) UK labor market report. Forecasts point to another rise in jobless claims by 20.3 thousand following a 25.8 thousand increase in September. The unemployment rate is expected to edge up from 4.8% to 4.9%, adding pressure on the Bank of England to ease monetary policy. Wage growth excluding bonuses may slow from 4.7% to 4.6%, while including bonuses — from 5.0% to 4.9%.

On Thursday at 09:00 (GMT+2), GDP data for Q3 will be published. Preliminary estimates point to a slowdown in quarterly growth from 0.3% to 0.2% and in annual growth from 1.4% to 1.3%. Another key factor remains industrial output, pressured by global trade difficulties and protectionist measures from the US and EU. The European Commission recently imposed higher tariffs on steel imports above quota limits, which hit the UK steel industry particularly hard — over 70% of British steel exports go to the EU, where competition with cheaper Chinese products remains tough. Traders are also assessing last week’s Bank of England meeting: the regulator narrowly voted (5–4) to keep the rate unchanged at 4.00%. Persistent inflation expectations — with annual CPI holding at 3.8% for three months — were a decisive factor. The next BoE meeting is set for December 18, and markets currently price in a 25 basis point rate cut. Meanwhile, the US dollar remains supported by expectations that the Fed will not rush into policy adjustments.

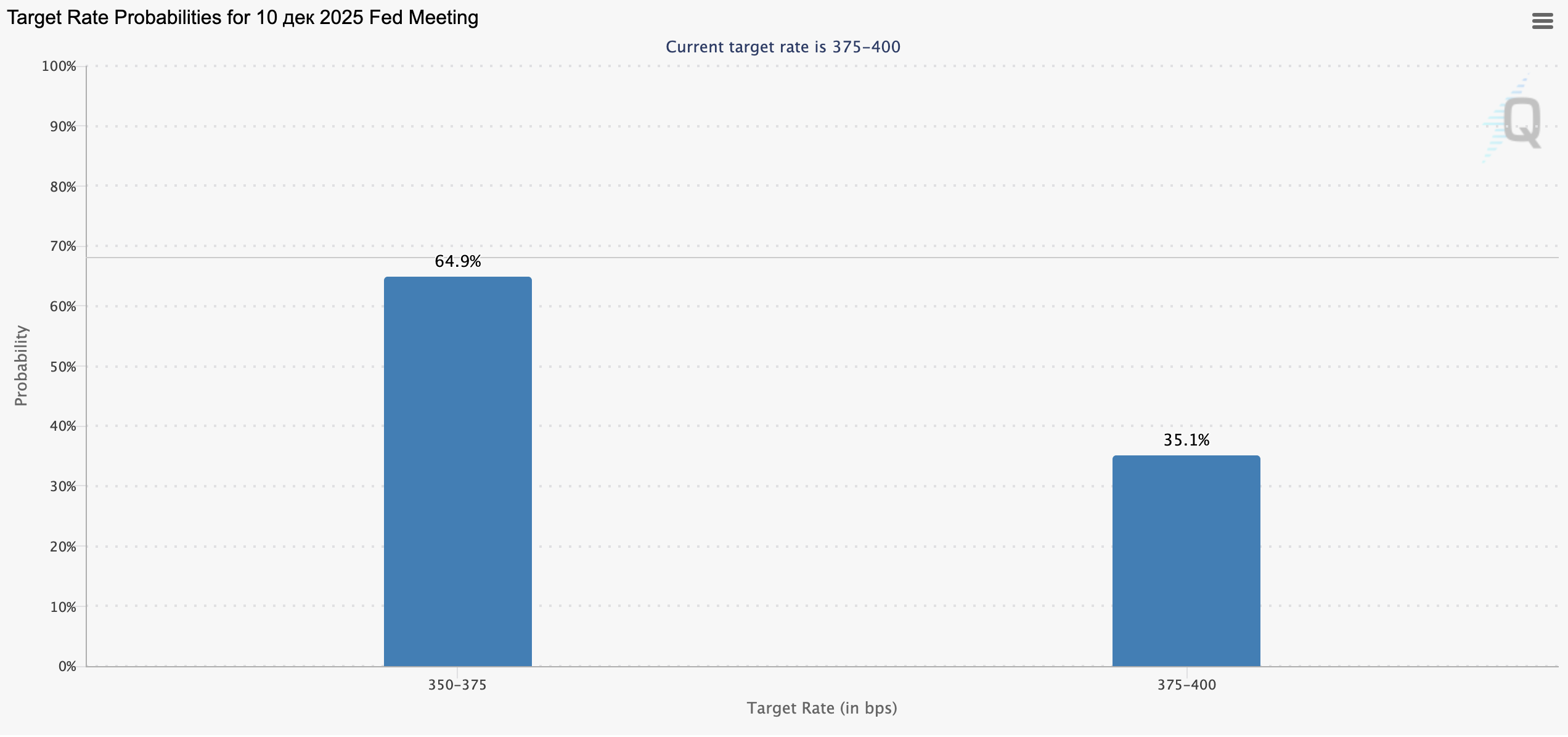

Market forecasts:

- Rate cut by 25 bps to the 3.50–3.75% range — probability 64.9%.

This is the main scenario, indicating market expectations for a dovish shift from the Fed.

- Rate unchanged at 3.75–4.00% — probability 35.1%.

This outcome is possible if inflation and the labor market remain resilient.

Interpretation: Most investors expect the first rate cut since the Fed paused its tightening cycle. This signals a possible transition to a more accommodative policy, traditionally putting pressure on the US dollar while supporting gold, stocks, and cryptocurrencies.

AUD/USD

The AUD/USD pair is gaining momentum, continuing last Friday’s bullish trend that helped recover earlier losses. The instrument is preparing to test the 0.6530 level for an upside breakout, supported by inflation data from China. The consumer price index rose from –0.3% to 0.2% year-on-year and from 0.1% to 0.2% month-on-month, prompting Chinese authorities to expand economic support measures. Inflation has not exceeded 1.0% since February 2023, and was even flat in June and September 2024. The situation remains affected by weakened export markets and US trade restrictions, though recent negotiations between Washington and Beijing helped prevent new tariff escalations. Meanwhile, strong Australian trade data also supported the Aussie: exports grew 7.9% in September after falling 8.7% a month earlier, while imports slowed from 3.3% to 1.1%, pushing the trade surplus to 3.94 billion AUD. On Thursday (02:30 GMT+2), October employment data may clarify the Reserve Bank of Australia’s rate outlook, with forecasts suggesting a 14.5 thousand job gain and unemployment edging down from 4.5% to 4.4%.

USD/JPY

The USD/JPY pair is showing restrained growth near 154.00, as expectations rise that the Bank of Japan will delay further tightening following the election of Prime Minister Sanae Takaichi — a supporter of accommodative policy. She plans to expand social spending and defense budgets amid geopolitical tensions. Takaichi recently stated that Japan is still halfway toward its inflation goals, while external risks such as US and EU trade restrictions and competition from China persist. Today’s macro data had little market impact: the leading indicators index rose from 107.0 to 108.0 points, and the coincident index climbed from 112.8 to 114.6. Meanwhile, the US faces a record-long government shutdown approaching 40 days. The Senate again failed to pass temporary funding, and President Donald Trump blamed the Democrats. The prolonged shutdown is weighing on GDP growth and could lead to more layoffs and delayed defense contracts, although reports indicate that the Senate and Republicans may soon finalize a compromise bill for the House vote.

Gold: XAU/USD

The XAU/USD pair is gaining value, once again attempting to consolidate above the key psychological level of 4000.00 and testing 4060.00 for a breakout. The metal was supported by improving US-China trade relations — both sides agreed to suspend new tariffs starting in November. Previously, President Donald Trump had threatened a 100% tariff on Chinese goods in response to rare-earth export restrictions. After APEC negotiations, the US reduced the planned tariff to 10%, while China postponed its export restrictions until November 10, 2026.

Meanwhile, US consumer sentiment data added pressure on the dollar: the University of Michigan index dropped from 53.6 to 50.3 in November, below forecasts. The expectations index also declined from 50.3 to 49.0. Additionally, Challenger, Grey & Christmas reported a surge in layoffs — from 54,060 to 153,070 in October — amid the shutdown and growing use of AI technologies. Fed Chair Jerome Powell reiterated that rate cuts in December would be “risky,” despite stable inflation trends. However, optimism emerged after news that the Senate reached a deal to extend government funding in exchange for future votes on healthcare subsidies expansion.