Later today at 11:00 (GMT+2), investors and forex traders will focus on Germany’s IFO business sentiment data. Forecasts suggest a slight improvement in the Business Climate Index in December from 88.1 to 88.2 points, while the Expectations Index may ease marginally from 90.6 to 90.5 points, and the Current Assessment Index is expected to edge up from 85.6 to 85.7 points.

Earlier, Germany released business activity data from S&P Global and Hamburg Commercial Bank (HCOB), showing that the manufacturing PMI fell from 48.2 to 47.7 points, missing expectations of 48.5, while the services PMI declined from 53.1 to 52.6 points against preliminary estimates of 52.8.

Hopes that increased defense spending would support corporate sentiment have not materialized. The German economy remains vulnerable, facing an ongoing crisis in the automotive sector amid rising energy prices, aggressive U.S. import tariffs, and intensifying competition from Chinese manufacturers.

Meanwhile, sentiment data from the ZEW Institute were mixed: the index assessing current economic conditions in December dropped sharply from –78.7 to –81.0 points, compared with expectations of –80.0, while the Economic Sentiment Index rose from 38.5 to 45.8 points. Across the euro area, the indicator also climbed from 25.0 to 33.7 points, exceeding forecasts of 26.3.

At the same time, the U.S. dollar came under pressure following labor market data. In October, nonfarm payrolls declined by 105.0 thousand after a gain of 108.0 thousand a month earlier, while November saw an increase of 64.0 thousand, above expectations of 50.0 thousand.

Average hourly earnings slowed in November from 0.4% to 0.1%, below forecasts of 0.3%, and eased year-on-year from 3.7% to 3.5%. The deceleration in wage growth may signal further easing of inflationary risks, which the Federal Reserve continues to cite as a key reason for maintaining its current monetary policy stance. The most negative aspect of the report was the sharp rise in the unemployment rate from 4.4% to 4.6%.

GBP/USD

The British pound is losing ground against the U.S. dollar, with GBP/USD testing the 1.3400 level for a downside break, although the pair remains close to its local highs recorded on October 17. Investors and forex traders are assessing key UK inflation data for November released today. The annual CPI fell from 3.6% to 3.2% versus expectations of 3.5%, while the monthly figure dropped from 0.4% to –0.2% against forecasts of 0.0%. Core CPI also eased from 3.4% to 3.2%.

Meanwhile, the Producer Price Index rose by 0.3% after 0.0% (revised from –0.3%) a month earlier. These figures precede the Bank of England meeting, the outcome of which will be announced tomorrow at 14:00 (GMT+2).

Analysts largely expect the BoE to cut interest rates by 25 basis points to 3.75%. Officials have previously stated that inflation remains elevated, but there is little time left to wait for prices to stabilize at target levels. The UK economy is showing zero growth and could return to stagnation at any moment, as analysts’ forecasts remain pessimistic.

Against this backdrop, the government has approved a budget featuring aggressive tax hikes alongside cuts in social spending. Some support for the pound came from business activity data released earlier, showing the S&P Global manufacturing PMI rising from 50.2 to 51.2 points in December, while the services PMI increased from 51.3 to 52.1 points, exceeding expectations of 51.5.

Meanwhile, similar data from the U.S. showed the manufacturing PMI slipping from 52.2 to 51.8 points against forecasts of 52.0, while the services PMI fell from 54.1 to 52.9 points. The main negative factor for the dollar remained the mixed November labor market report, as unemployment rose from 4.4% to 4.6% despite a gain of 64.0 thousand jobs.

AUD/USD

The Australian dollar shows mixed dynamics in the AUD/USD pair, consolidating near the 0.6630 level. The instrument displayed fairly active price action in the previous session, but neither bulls nor bears managed to gain a decisive advantage.

As a reminder, the U.S. dollar came under pressure after labor market data showed that nonfarm payrolls fell by 105.0 thousand in October after rising by 108.0 thousand previously, while November payrolls increased by 64.0 thousand versus expectations of 50.0 thousand. Average hourly earnings slowed from 0.4% to 0.1% month-on-month and from 3.7% to 3.5% year-on-year.

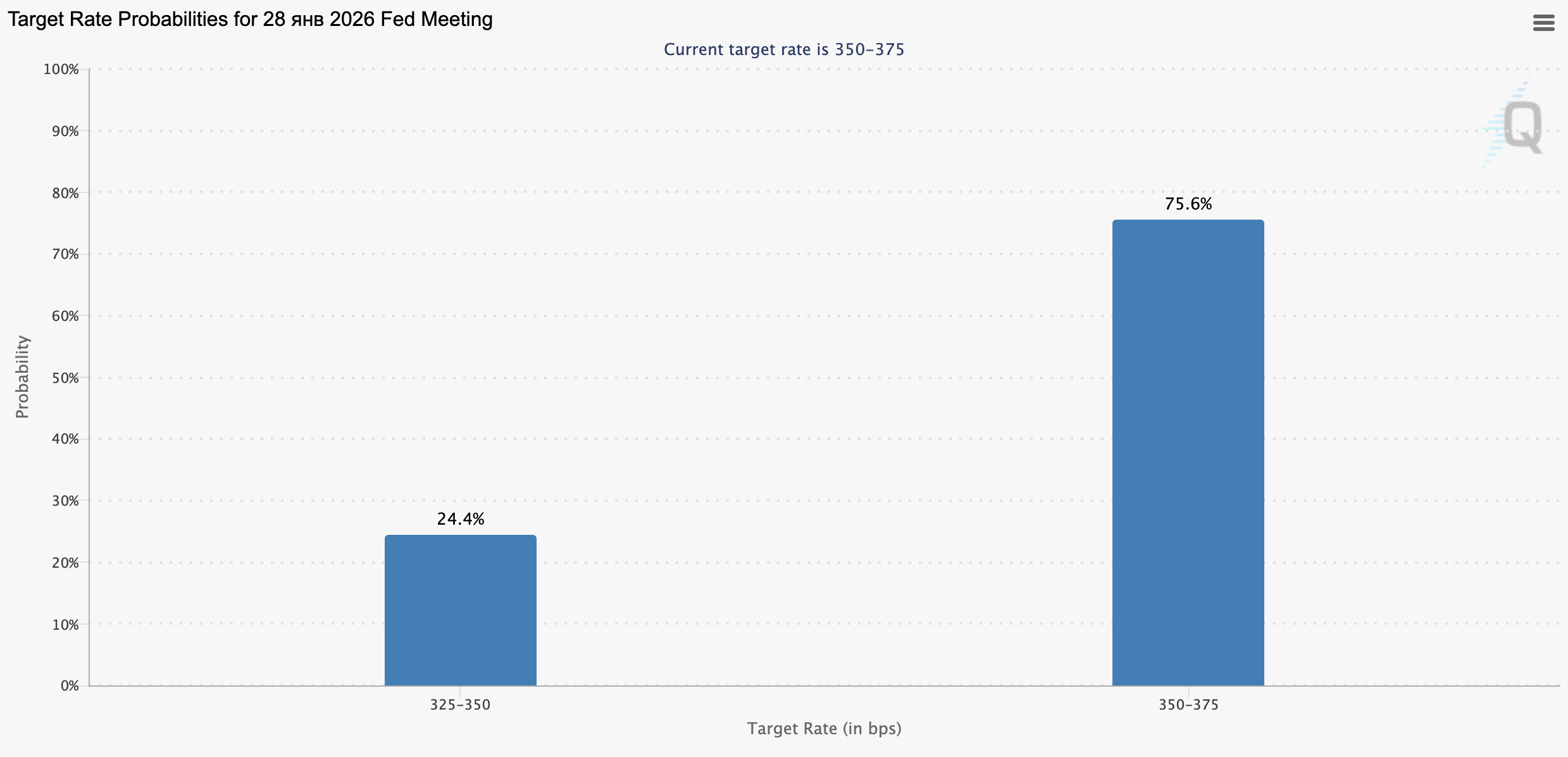

Overall, the report did not materially change expectations for the Federal Reserve’s January meeting, with the probability of rates remaining unchanged still around 75.6%. Support for the Australian dollar came from business activity data, with the S&P Global manufacturing PMI rising from 51.6 to 52.2 points in December, while the services PMI declined from 52.8 to 51.0 points. Meanwhile, the Melbourne Institute Consumer Confidence Index dropped sharply from 12.8% to –9.0%.

USD/JPY

The U.S. dollar is gaining against the Japanese yen, correcting after the bearish impulse formed last week when the pair retreated from its November 25 highs. USD/JPY is currently testing the 154.90 level for an upside break as traders assess Japan’s foreign trade data.

Exports rose by 6.1% in November after a 3.6% increase in the previous month, beating expectations of 4.8%, while imports accelerated from 0.7% to 1.3%, missing forecasts of 2.6%.

As a result, the trade balance posted a surplus of 322.2 billion yen, significantly above expectations of 71.2 billion yen, compared with a deficit of –231.8 billion yen in October.

Market participants are also cautious ahead of the Bank of Japan meeting scheduled for Friday at 05:00 (GMT+2). Current market expectations lean toward a 25 basis point rate hike to 0.75%, although officials are likely to signal the need to assess the impact of previous measures. Tighter monetary policy could also spark political tensions, as Prime Minister Sanae Takaichi is known for her dovish stance.

Japan’s supplementary budget предусматривает higher social spending and a sharp increase in defense and military expenditures, raising concerns about a rapid expansion of public debt. Analysts note that higher borrowing costs may have only a limited impact on the yen, as such a move has largely been priced in.

Meanwhile, the yen received support from business activity data: the Jibun Bank manufacturing PMI rose from 48.7 to 49.7 points in December, well above forecasts of 48.8, while the services PMI slipped from 53.2 to 52.5 points but remained comfortably above the 50.0 threshold separating expansion from contraction.

Pressure on the dollar also came from weak December business activity data and the mixed labor market report, particularly the rise in unemployment from 4.4% to 4.6%, which strengthened expectations of another rate cut in early 2026. Manufacturing PMI fell from 52.5 to 51.8 points, while services PMI declined from 54.1 to 52.9 points.

XAU/USD

The XAU/USD pair is showing mixed dynamics, consolidating near the 4325.00 level, as market activity remains subdued amid a lack of fresh U.S. catalysts. Gold could receive an additional upside impulse tomorrow at 14:00 (GMT+2) when the Bank of England announces its policy decision, as analysts expect a 25 basis point rate cut to 3.75%.

At 15:15 (GMT+2), the European Central Bank (ECB) will hold its meeting. Officials are likely to signal the end of the current dovish cycle and point to the potential for policy tightening should macroeconomic data improve and inflationary risks intensify.

Meanwhile, investors continue to focus on the latest U.S. labor market report. Nonfarm payrolls fell by 105.0 thousand in October after a 108.0 thousand increase previously, while November payrolls rose by 64.0 thousand versus expectations of 50.0 thousand.

Average hourly earnings slowed from 0.4% to 0.1% month-on-month and from 3.7% to 3.5% year-on-year. The slowdown in wage growth may indicate further easing of inflationary pressures, which the Federal Reserve continues to view as a key argument for keeping monetary policy unchanged. The sharp rise in the unemployment rate from 4.4% to 4.6% was the most negative aspect of the report.