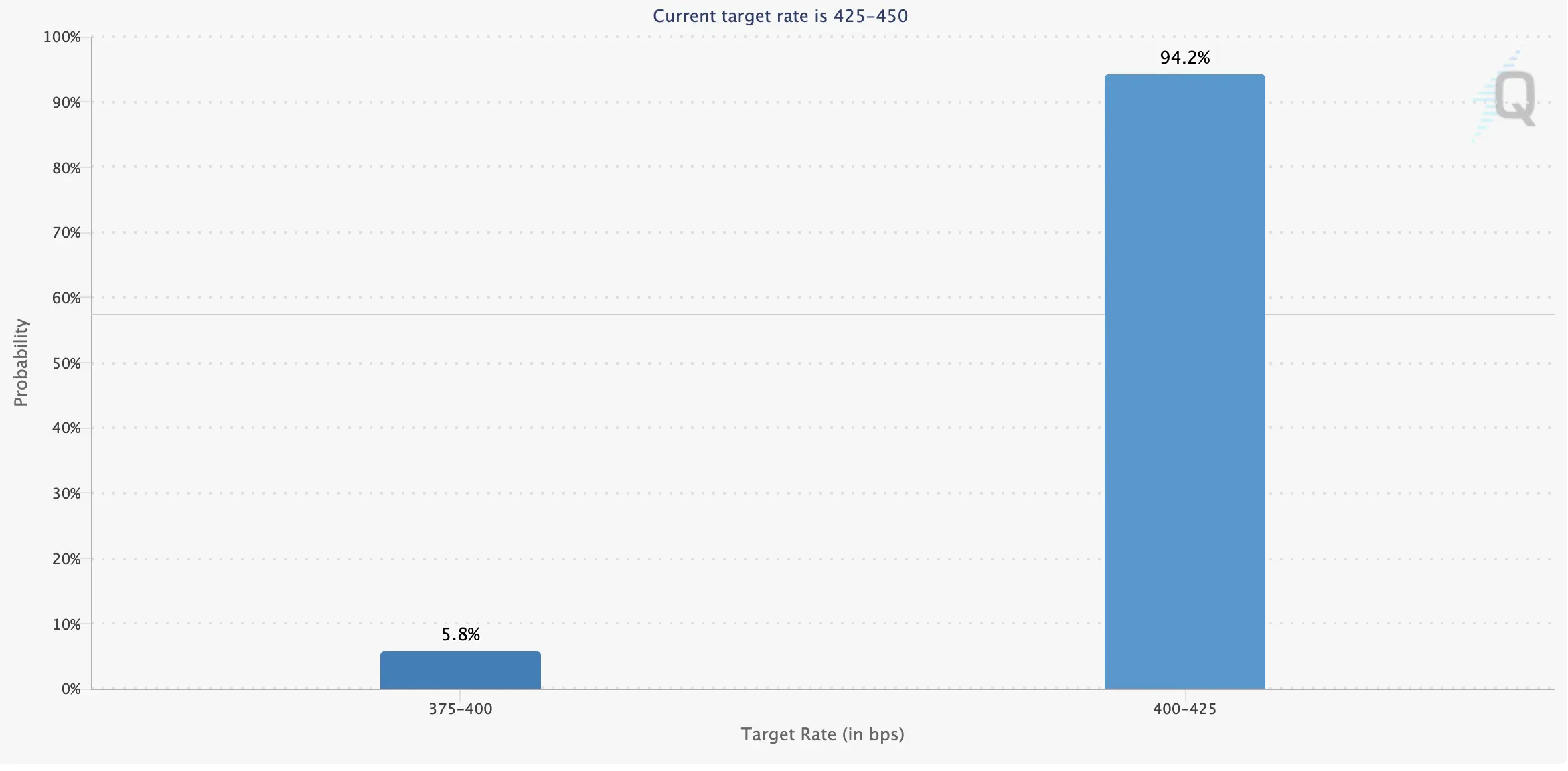

At 20:10 (GMT+2) today, European Central Bank (ECB) President Christine Lagarde is scheduled to speak and may comment on the region’s economic outlook. Markets see, at most, one additional 25-basis-point rate cut by the ECB before year-end. Friday’s data from Germany showed August CPI at 2.2% year-over-year and 0.1% month-over-month, while the harmonized index rose 2.1% YoY and 0.1% MoM, in line with ECB targets. Final August eurozone inflation figures are due Wednesday at 11:00 (GMT+2) and are not expected to deviate meaningfully from 2.1% YoY and 0.2% MoM. Also on Wednesday at 20:00 (GMT+2), the Federal Reserve will conclude its two-day meeting. Investors are now largely convinced the Fed will cut rates by 25 basis points amid a notably cooling labor market. In August, nonfarm payrolls rose by just 22,000, and subsequent benchmark revisions showed employment over the 12 months through March running 911,000 below initial estimates. Fed Chair Jerome Powell may also signal further policy easing into year-end, which could weigh on the dollar across the board.

GBP/USD

The pound is advancing against the U.S. dollar in the morning session, rebounding after a tentative pullback late last week. The pair is testing 1.3565 to the upside as traders remain cautious ahead of Wednesday’s 20:00 (GMT+2) Fed decision, where analysts widely expect the start of a new easing cycle amid disappointing labor data and political pressure from the White House. The dollar softened after University of Michigan data showed September consumer expectations down to 51.8 from 55.9 (consensus 54.9) and consumer sentiment at 55.4 from 58.2 (consensus 58.0). Notably, one-year inflation expectations held at 4.8%, while five-year expectations rose to 3.9% from 3.5%.

U.K. data had only a modest impact: Rightmove’s September house price index rose 0.4% after -1.3% in August, while the annual rate dipped 0.1% after +0.3%. On Tuesday at 08:00 (GMT+2), jobs data for July and August are due: forecasts look for a slight slowdown in job gains from 239,000 to 200,000, average total pay for July easing from 5.0% to 4.8%, and unemployment steady at 4.7%.

NZD/USD

The New Zealand dollar is rising against the U.S. dollar in the morning session, recovering Friday’s losses. The pair is testing 0.5960 to the upside, near the August 14 local highs. Macro data are exerting some pressure on NZD: New Zealand’s BusinessNZ services PSI fell to 47.5 in August from 48.9 (analysts had looked for a rebound above 49.0). Activity continues to slow amid sticky inflation and high rates, though policy is gradually easing. In August, the Reserve Bank of New Zealand (RBNZ) cut rates by 25 bps to 3.00%. Governor Christian Hawkesby noted elevated concern among both firms and consumers, which can be read as a signal for further easing in the near term.

Chinese data are also weighing on the outlook for New Zealand trade: industrial production slowed to 5.2% from 5.7% YoY (consensus 5.8%), retail sales eased to 3.4% from 3.7% (consensus 3.8%), and year-to-date fixed-asset investment cooled to 0.5% from 1.6% (consensus 1.4%). The Fed’s two-day meeting concludes Wednesday at 20:00 (GMT+2). Analysts overwhelmingly expect a 25-basis-point rate cut as the U.S. labor market cools faster than initially forecast. Chair Jerome Powell may also hint at further easing by year-end.

USD/JPY

The U.S. dollar is edging lower against the yen in Asian trading, with the pair broadly rangebound in the very near term as traders avoid new positions ahead of Wednesday’s 20:00 (GMT+2) Fed decision. Markets expect a 25-basis-point rate cut in September, likely marking the beginning of a rate-cut cycle. Last week’s U.S. benchmark revision showing employment 911,000 below prior estimates for the 12 months through March reinforced the case for easing. Even so, Chair Powell remains wary of inflation risks, making a more aggressive move unlikely for now.

The yen’s backdrop remains fragile amid potential political turmoil: last week Prime Minister Shigeru Ishiba resigned after the ruling Liberal Democratic Party lost July’s parliamentary elections. Having served less than a year, his departure has raised concerns about frequent leadership changes. The situation is compounded by the Bank of Japan’s gradual tightening efforts even as Tokyo negotiates tariff issues with Washington while heavily reliant on auto exports. The BOJ’s policy decision is due Friday; for now, consensus is for no change amid the broader domestic instability.

XAU/USD

Gold is trading mixed this morning, consolidating near 3640.00 and holding close to last week’s record highs. Position-taking is muted as the Fed’s two-day meeting begins tomorrow; a 25-basis-point cut is widely expected, which would kick off a new easing cycle. For 2025 as a whole, analysts see two to three 25-bp cuts, though Chair Powell may proceed more cautiously if the labor market stabilizes.

Rate-cut expectations surged after the August jobs report showed just 22,000 new nonfarm payrolls and unemployment rising to 4.3%. A subsequent Department of Labor benchmark revision indicated employment over the 12 months through March was 911,000 below earlier estimates. Traders also noted last week’s uptick in monthly CPI to 0.4%, with the annual rate holding at 2.9%