At this point, there is virtually no doubt that the interest rate will be cut by 25 basis points to 3.75%, and this expectation is already largely priced into many assets. Nevertheless, Fed Chair Jerome Powell continues to strike a cautious tone: in his latest speech, he again stressed that it is still too early to count on a full-fledged monetary easing cycle, given that inflation risks remain elevated.

Even so, data released on Friday by the University of Michigan showed a slowdown in one-year inflation expectations from 4.5% to 4.1%, and in five-year expectations from 3.4% to 3.2%. At the same time, the euro received some support on Friday from euro area labour market figures: employment in the eurozone as a whole rose from 0.5% to 0.6% year-on-year and from 0.1% to 0.2% quarter-on-quarter. Seasonally adjusted GDP in Q3 was unchanged at 1.4% year-on-year, while the quarterly figure was revised up from 0.2% to 0.3%, reflecting a sharp increase in defence spending and the launch of infrastructure modernisation programmes in Germany. Today, investors and forex traders are assessing Germany’s October industrial production data: the indicator rose 1.8% m/m after 1.1% (revised from 1.3%) a month earlier, while analysts had expected a decline of 0.4%.

GBP/USD

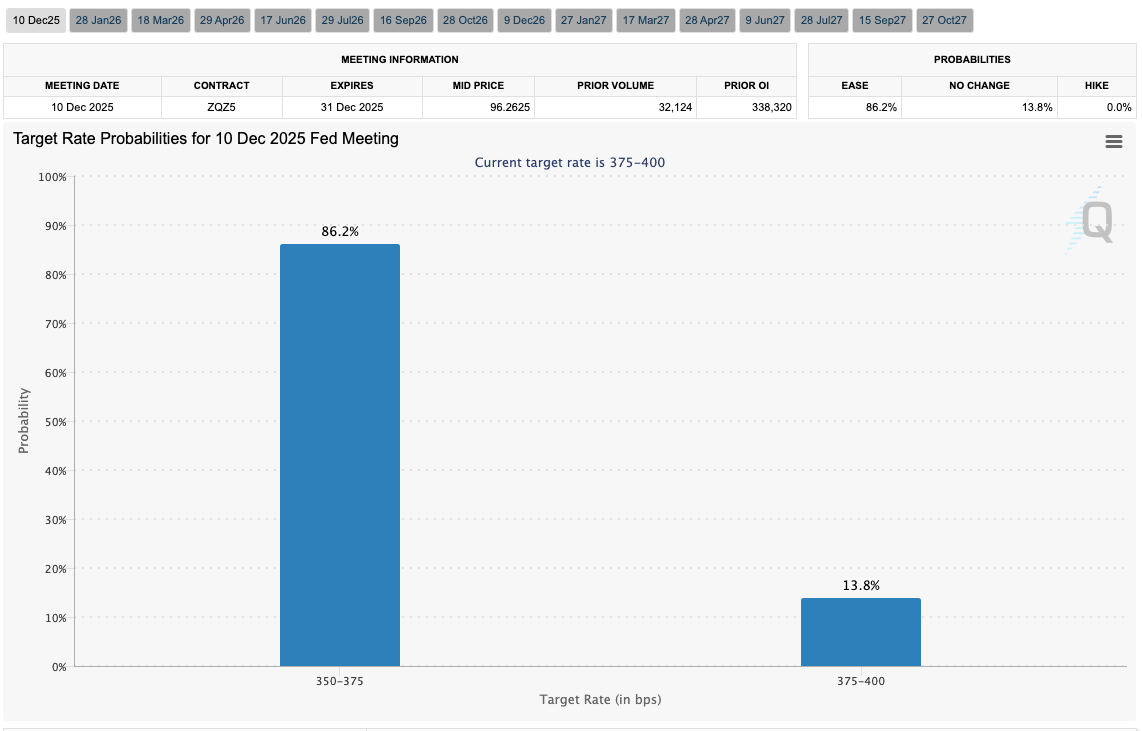

The pound is strengthening against the U.S. dollar in the GBP/USD pair, recovering the positions lost late last week when quotes retreated from the local highs of October 22. The instrument is testing the 1.3340 level for an upside breakout, while market participants are in no hurry to open new positions, preferring to wait for the outcome of the Fed meeting, which will be announced on December 10. Analysts broadly expect a 25-basis-point rate cut to 3.75%, but Powell’s comments on the future path of monetary policy will remain crucial. It is worth noting that his second four-year term as Fed Chair expires in May 2026.

U.K. investors, in turn, will focus today on speeches by Bank of England representatives Alan Taylor (at 16:30 (GMT+2)) and Clare Lombardelli (at 20:30 (GMT+2)). It is possible that officials will signal support for a rate cut at the Bank of England’s December 18 meeting.

Later this week, the U.K. will publish a batch of October macroeconomic data. On Friday at 09:00 (GMT+2), the market will receive updates on GDP and industrial production. The national economy is expected to grow 0.1% after a 0.1% contraction in the previous month, while industrial production is forecast to rise 0.8% after a 2.0% decline.

USD/JPY

The U.S. dollar is trading sideways against the Japanese yen in the USD/JPY pair, consolidating around the 155.00 mark. Market participants are reluctant to open new positions as the Fed’s two-day policy meeting starts tomorrow, an event that could have a strong impact on the U.S. currency. Currently, more than 90.0% of analysts expect the regulator to cut rates by 25 basis points to 3.75%. Powell continues to take a cautious stance, warning against a resurgence of inflation while speaking positively about the pace of the U.S. economic recovery.

It is important to note that the labour market outlook is still constrained by a lack of up-to-date macro data: the October jobs report was not released due to the government shutdown, and November figures will not be available before the rate decision. Meanwhile, the core PCE price index for September slowed from 2.9% to 2.8% year-on-year and remained at 0.2% month-on-month, while the broader indicator accelerated from 2.7% to 2.8%, matching forecasts. Monday’s data from Japan were generally weak: Q3 GDP fell 0.6% q/q after a 0.4% contraction previously (preliminary estimate: –0.5%), and in annualised terms the economy shrank from –1.8% to –2.3% versus expectations of –2.0%. The Eco Watchers current conditions index also declined in November from 49.1 to 48.7 points (forecast: 49.5). These weak figures will likely make it harder for the Bank of Japan to move ahead with further monetary tightening.

XAU/USD

The XAU/USD pair is consolidating, trading just below the 4,200.00 mark as market participants await the outcome of the Fed meeting on December 10. There is little doubt that the regulator will cut rates by 25 basis points to the 3.50–3.75% range. Updated macroeconomic projections to be released alongside the decision could significantly influence broader market sentiment.

Not all members of the Federal Open Market Committee (FOMC) are taking a dovish stance in support of Powell, who has repeatedly warned markets against overly optimistic expectations regarding the pace of monetary easing. Nevertheless, inflation is slowing, while political pressure from the White House on the Fed remains strong. On Friday, the University of Michigan published updated December forecasts: one-year inflation expectations slowed from 4.5% to 4.1%, and five-year expectations from 3.4% to 3.2%.

The latest U.S. household income and spending figures were mixed: incomes rose another 0.4% versus an initial estimate of 0.3%, while spending was revised down from 0.5% to 0.3%, which could further support the easing of price pressures. The Bank of England may also announce a rate cut at its December 18 meeting, which would provide additional support for gold. Geopolitical risks remain in focus as well: the Russia–Ukraine conflict continues, although in recent weeks U.S. officials have once again attempted to broker a peace agreement that could significantly reduce tensions in the region. Analysts, however, believe that after that, U.S. President Donald Trump may shift focus to South America, where the risk of military operations persists.