The U.S. dollar is gaining support as the conflict between the United States and Iran intensifies. According to the latest Pentagon forecasts, the confrontation could last at least 100 days, increasing the risk of sustained growth in hydrocarbon prices and a slowdown in the global economy. In such conditions, investors tend to turn to the dollar as a traditional safe-haven asset. Traders believe the crisis may have a smaller impact on the U.S. economy compared with other regions, as the country has large domestic energy reserves and imports most of its oil from Canada and Mexico. By contrast, the United Kingdom previously relied more heavily on energy supplies from the Middle East.

Nevertheless, inflation in the United States may continue to rise in the medium term while the labor market shows signs of weakening. Consumer inflation reached 2.4% in January, while producer prices increased to 2.9%. At the same time, unemployment rose to 4.4% in February and employment declined by 92,000. These developments could deepen divisions within the Federal Reserve between hawkish policymakers focused on combating inflation and dovish members concerned about labor market weakness. At present, most officials favor maintaining current monetary policy for an extended period. Cleveland Federal Reserve Bank President Beth Hammack has also suggested that interest rates could rise further if inflation fails to reach the 2.0% target by the end of the year.

In contrast, macroeconomic data in the United Kingdom may allow the Bank of England to begin easing monetary policy in the near future. Preliminary figures show that GDP growth in the fourth quarter reached only 0.1% quarter-on-quarter compared with expectations of 0.2%, and 1.0% year-on-year versus forecasts of 1.2%. Unemployment increased from 5.1% to 5.2% in December. Meanwhile, consumer inflation slowed in January from 3.4% to 3.0% in headline terms and from 3.1% to 2.9% in core terms, although it remains relatively elevated. Earlier, Bank of England Governor Andrew Bailey indicated that borrowing costs could be adjusted as early as the March meeting.

Overall, fundamental factors continue to support the likelihood of further downside pressure on the GBP/USD pair.

Support and resistance levels

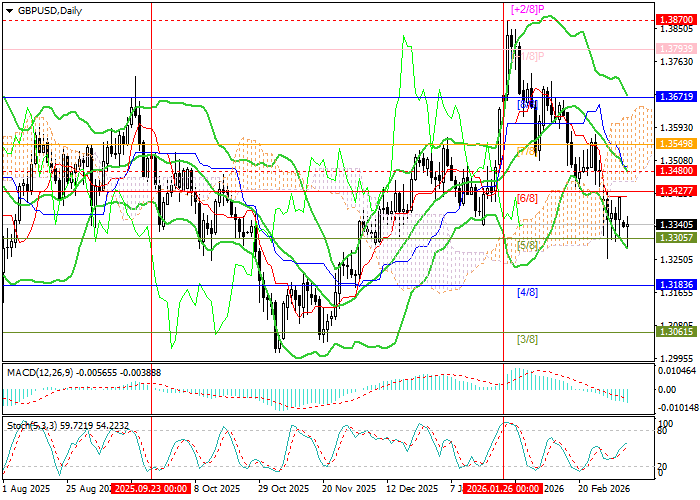

The instrument has been declining for the second consecutive month and is currently testing the 1.3305 level (Murray level [5/8]). A breakout below this mark could open the way toward 1.3183 (Murray level [4/8]) and 1.3061 (Murray level [3/8]). However, if the price breaks above the middle line of the Bollinger Bands at 1.3480, upward movement could develop toward 1.3671 (Murray level [8/8]) and 1.3870 (the January high).

Technical indicators provide mixed signals. Bollinger Bands are turning downward, the MACD histogram continues to expand in negative territory, while the Stochastic oscillator has turned upward, leaving room for a potential corrective rebound.

Resistance levels: 1.3480, 1.3671, 1.3870.

Support levels: 1.3305, 1.3183, 1.3061.

Trading scenarios and GBP/USD forecast

Short positions may be opened below 1.3305 with targets at 1.3183 and 1.3061, with a stop-loss at 1.3390. Implementation period: 5–7 days.

Long positions may be opened above 1.3480 with targets at 1.3671 and 1.3870, with a stop-loss at 1.3340.