The escalation of geopolitical tensions in the Middle East remains the key pressure factor for the Australian stock market. The sharp rise in crude oil prices has increased costs for an economy that, despite its strong commodity sector, remains heavily dependent on energy imports. A significant portion of supplies passes through strategic routes in the Persian Gulf, including the Strait of Hormuz, which has been blocked by Iran’s Islamic Revolutionary Guard Corps (IRGC). Around 20–25% of global oil supplies are transported through this corridor, making it a crucial element of the global energy system.

IRGC officials have already warned that any vessel passing through the route could become a target. Earlier this year, traffic fell to only several dozen tankers per day, and in the first week of March it dropped to just four. Against this backdrop of geopolitical risks, global Brent crude oil prices have exceeded $115.00 per barrel, significantly increasing production costs and inflationary pressures in the Australian economy.

Market participants are also focusing on macroeconomic statistics. The total value of new housing mortgage loans issued in the fourth quarter rose to AUD 161.8B, up 5.3% from the previous period. Meanwhile, the total volume of long-term asset-backed securities issued domestically increased by $10.1B to $197.8B, representing a 5.4% rise.

According to the latest report from the Australian Bureau of Statistics (ABS), the total number of jobs in the economy increased by 0.3% in the fourth quarter to 16.4M, while filled positions rose by 0.4% to 16.1M. The share of unfilled vacancies remained at 2.0%, and total hours worked increased by 0.7% to 6.1B hours. These figures indicate that labor demand remains resilient despite external economic risks and rising geopolitical uncertainty.

Tomorrow at 01:30 (GMT+2), investors will focus on the release of the Westpac Consumer Sentiment Index, which measures confidence in economic conditions based on a survey of about 1,200 respondents. Preliminary estimates suggest the indicator may decline from 90.5 points to 89.5, which could weigh on the national currency. However, the change is unlikely to be sufficient for the Reserve Bank of Australia (RBA) to abandon its tightening stance in the medium term.

Meanwhile, yields on key government bonds have been correcting during the active corporate earnings reporting phase. One-year bonds are trading at 4.299% compared with 4.227% at the end of last week. Ten-year bonds are yielding 4.845% versus 4.778%, while 20-year and 30-year bonds stand at 5.254% and 5.297%, respectively.

Top gainers in the index include WiseTech Global Ltd. (+10.83%), DroneShield Ltd. (+10.00%), Magellan Financial Group Ltd. (+9.27%), Pro Medicus Ltd. (+9.23%), and Domino's Pizza Enterprises Ltd. (+7.20%).

Among the biggest decliners are Sandfire Resources Ltd. (–9.58%), Westgold Resources Ltd. (–8.17%), Northern Star Resources Ltd. (–8.11%), Genesis Minerals Ltd. (–7.17%), and Regis Resources Ltd. (–6.40%).

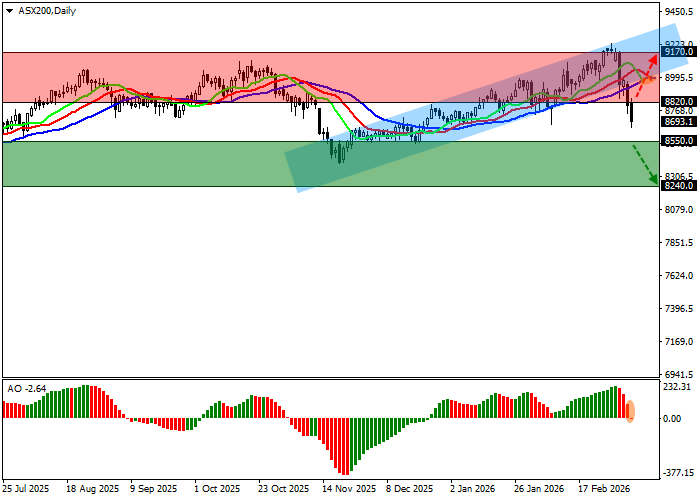

Support and resistance levels

On the daily chart, the instrument is moving away from the support line of a local ascending channel with dynamic boundaries at 9300.0–8950.0, targeting a test of last year’s low.

Technical indicators are close to reversing and preparing to generate a stable sell signal. The fast EMAs of the Alligator indicator are moving away from the signal line, while the Awesome Oscillator histogram is forming corrective bars while remaining below the transition level.

Support levels: 8550.0, 8240.0.

Resistance levels: 8820.0, 9170.0.

Trading scenarios and ASX 200 forecast

Short positions may be opened after a breakout below 8550.0 with a target at 8240.0. Stop-loss — 8700.0. Implementation period: 7 days or more.

Long positions may be opened after the price consolidates above 8820.0 with a target at 9170.0 and a stop-loss at 8700.0.