The key factor preventing the pair from developing a sustained bullish impulse remains macroeconomic data, which have confirmed the Bank of Japan’s concerns about household spending dynamics. According to the latest report, monthly spending rose by 6.2% in November, far exceeding the 2.7% forecast by analysts, while the annual figure accelerated to 2.9% from 0.1%. These figures point to resilient domestic demand and strengthen the case for tighter monetary conditions. It is worth recalling that on December 19, the Bank of Japan raised its policy rate by 25 basis points to 0.75%, the highest level since 1995, marking a significant turning point away from decades of ultra-loose monetary policy. The impact of the regulator’s hawkish rhetoric on inflation remains limited so far, broadly in line with expectations.

At the same time, BOJ Governor Kazuo Ueda noted that management practices at Japanese companies have changed fundamentally in recent years, particularly with regard to wage indexation and pricing strategies, allowing inflation to move gradually toward the 2.0% target. He expressed optimism about the country’s economic trajectory, stressing that the likelihood of returning to a so-called “zero-rate environment” has fallen sharply. Currency interventions are also not being considered in the near term due to political uncertainty and the possibility of changes in national leadership, adding further pressure on the yen. Earlier this week, local media reported that Prime Minister Sanae Takaichi is expected to meet with the press on Friday and may announce the dissolution of the lower house of parliament at the start of the next session, paving the way for early general elections on February 8 or 15. This scenario increases short-term uncertainty and fuels volatility in the FX market. Toward the end of last year, the government held active discussions with the Bank of Japan on stabilizing the yen without adjusting borrowing costs, but current USD/JPY dynamics suggest these measures have had limited effectiveness.

As for the U.S. dollar, its upward momentum may persist in the near term amid expectations that interest rates will remain unchanged at the January 29 meeting. This view is indirectly supported by the escalating conflict between the Republican administration in the White House and the leadership of the Federal Reserve. Over the weekend, Fed Chair Jerome Powell and several other officials received subpoenas from the U.S. Department of Justice, signaling the launch of a criminal investigation into alleged misuse of funds allocated for the reconstruction of the Fed’s headquarters in Washington. While the project was initially budgeted at $2.5 billion, its final cost reportedly exceeded $3.0 billion. The investigation, which includes a review of public statements and financial records, was approved back in November by Washington, D.C. prosecutor Janine Pirro. Powell described the move as politically motivated pressure aimed at forcing rate cuts, emphasizing that the Fed is acting “based on its best assessment of what serves the public interest, not presidential preferences.” Markets interpreted this as a clear signal that a return to a dovish easing cycle is unlikely. According to the CME FedWatch Tool, the probability of rates remaining in the 3.50–3.75% range stands at 95.0%.

In the near term, a rate hike by the Bank of Japan combined with a pause in the Fed’s easing cycle could further narrow the interest-rate differential between the two central banks, providing a moderately positive effect for the Japanese economy. However, refraining from further tightening while simultaneously rolling out newly announced fiscal stimulus measures will continue to weigh on the yen. These fundamental factors underpin a high probability of further strengthening in the USD/JPY pair over the coming quarter.

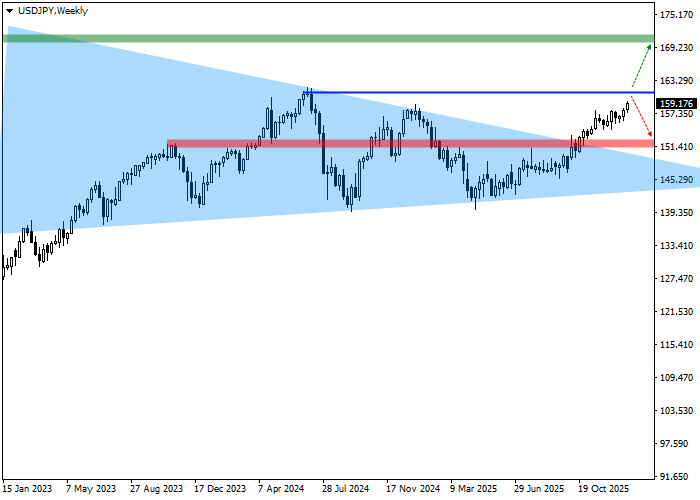

Technical indicators also point to a continuation of the current trend: on the weekly chart, price has rebounded from resistance and is moving higher as part of the breakout of a previously formed triangle pattern with dynamic boundaries at 154.00–142.00.

A decisive break above the 160.70 resistance level would signal an acceleration of the bullish move, with price potentially returning to this area toward the end of the month.

Key levels are best assessed on the daily chart.

As the chart shows, the current high near 161.00 represents a critical resistance level for the entire uptrend that began back in December 2020. A breakout above this level would open the way toward the 170.00 area.

The zone around the November 12, 2023 high at 152.00 serves as the invalidation area for the bullish scenario. If price returns to this level, the upward outlook would be canceled or significantly delayed, and long positions should be closed.

The 170.00 area marks a zone where profits on open positions should be taken.

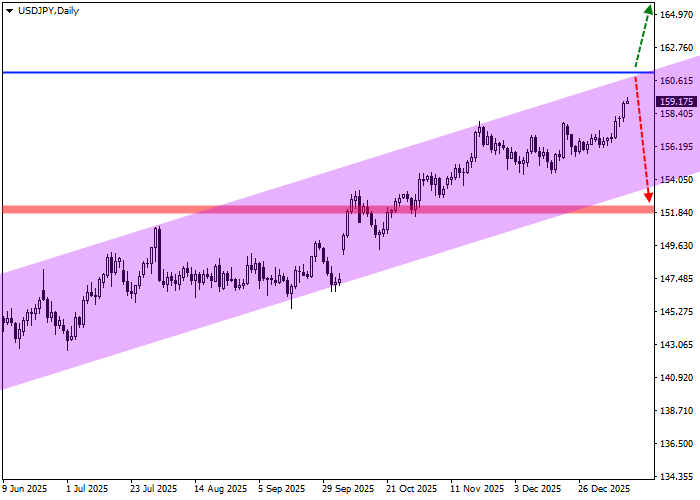

More detailed levels are illustrated on the four-hour timeframe.

The entry level is located at 160.70, corresponding to the peak recorded on June 30, 2024. A buy signal could emerge as early as this week if the current local high is broken. From a technical standpoint, this would confirm a breakout and open the door for market entry. Given the current average daily range of USD/JPY, which has stood at 66.5 points over the past month, a move toward the 170.00 target could take approximately 57 trading sessions. However, if volatility increases, this timeframe could shorten to around 48 days.