President Donald Trump has sent a formal statement to Congress declaring an end to military hostilities against Iran and the effective conclusion of the US-Iran conflict. He noted that no clashes between the parties have been recorded since April 7, and that the campaign launched on February 28 is now over — meaning the 60-day deadline under the War Powers Resolution has expired, after which the President must either obtain congressional approval to continue operations or bring them to a close. At the same time, Trump made clear that troops are not being withdrawn from the region: independent sources estimate that 30,000 to 40,000 US military personnel are currently deployed across the Persian Gulf area, including contingents in neighboring countries and naval forces. The Republican administration cites the need to deter Tehran, protect allies, and maintain control of strategic routes — including oil shipments through the Strait of Hormuz. The situation is therefore politically contentious: legally speaking, the conflict is over and no additional congressional authorization is required for the ongoing presence, yet in practice US forces remain in the region under a stabilization mission. This has drawn criticism from the Democratic Party, with experts describing the move as an attempt by the executive branch to circumvent legislative oversight.

Earnings season is underway. On Friday, Exxon Mobil Corp. reported revenue of $85.14 billion against an expected $81.24 billion, with earnings per share of $1.16 versus the $1.03 forecast. Fellow oil major Chevron Corp. posted revenue of $48.61 billion, falling short of the $51.39 billion estimate, but EPS of $1.41 beat the $0.97 projection. Colgate-Palmolive Co. recorded revenue of $5.32 billion and EPS of $0.970, ahead of the expected $5.22 billion and $0.940, while industrial gas and engineering firm Linde Plc. reported $8.78 billion in revenue and EPS of $4.33, topping forecasts of $8.60 billion and $4.27 respectively.

Bond markets responded to the fundamental backdrop: yields on the widely watched 12-month notes pulled back from 3.749% to 3.718% since Friday, 10-year Treasury yields fell from 4.418% to 4.387%, and 20-year bonds eased from 4.984% to 4.954%. 30-year yields also declined, moving from 4.988% to 4.961%.

Top gainers included Cboe Global Markets Inc. (+8.95%), Paramount Skydance Corp. (+8.30%), Seagate Technology Holdings Plc. (+7.91%), Oracle Corp. (+6.47%), and Eastman Chemical Co. (+6.07%).

Leading decliners were LKQ Corp. (–9.72%), The Clorox Co. (–9.67%), Stryker Corp. (–6.47%), Mohawk Industries Inc. (–6.42%), and Amgen Inc. (–4.75%).

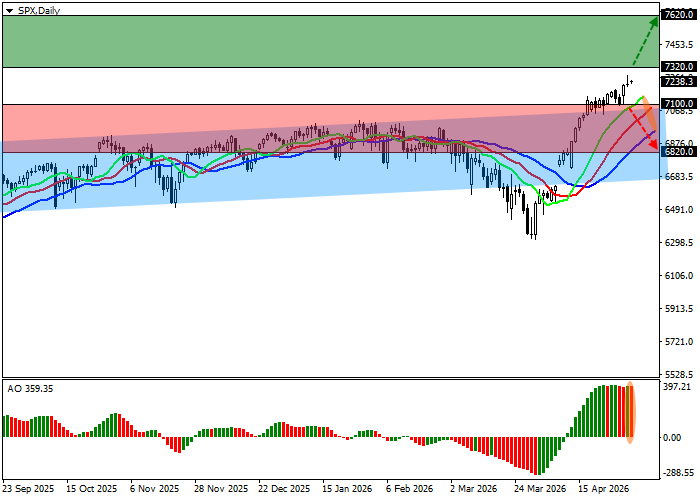

Support and Resistance Levels

On the daily chart, the index is moving in a corrective trend, attempting to pull back from the upper boundary of an ascending channel with boundaries at 7100.0–6700.0.

Technical indicators are reinforcing the buy signal: the fast EMAs on the Alligator indicator are moving away from the signal line, while the AO histogram is forming corrective bars in positive territory.

Resistance levels: 7320.0, 7620.0.

Support levels: 7100.0, 6820.0.

S&P 500 Trading Scenarios and Forecast

Long positions may be opened after a rally and consolidation above 7320.0, targeting 7620.0. Stop-loss: 7220.0. Time horizon: 7 days or more.

Short positions may be opened after a decline and consolidation below 7100.0, targeting 6820.0. Stop-loss: 7200.0.

Scenario

| Timeframe | Weekly |

| Recommendation | BUY STOP |

| Entry Point | 7320.5 |

| Take Profit | 7620.0 |

| Stop Loss | 7220.0 |

| Key Levels | 6820.0, 7100.0, 7320.0, 7620.0 |

Alternative Scenario

| Recommendation | SELL STOP |

| Entry Point | 7099.5 |

| Take Profit | 6820.0 |

| Stop Loss | 7200.0 |

| Key Levels | 6820.0, 7100.0, 7320.0, 7620.0 |