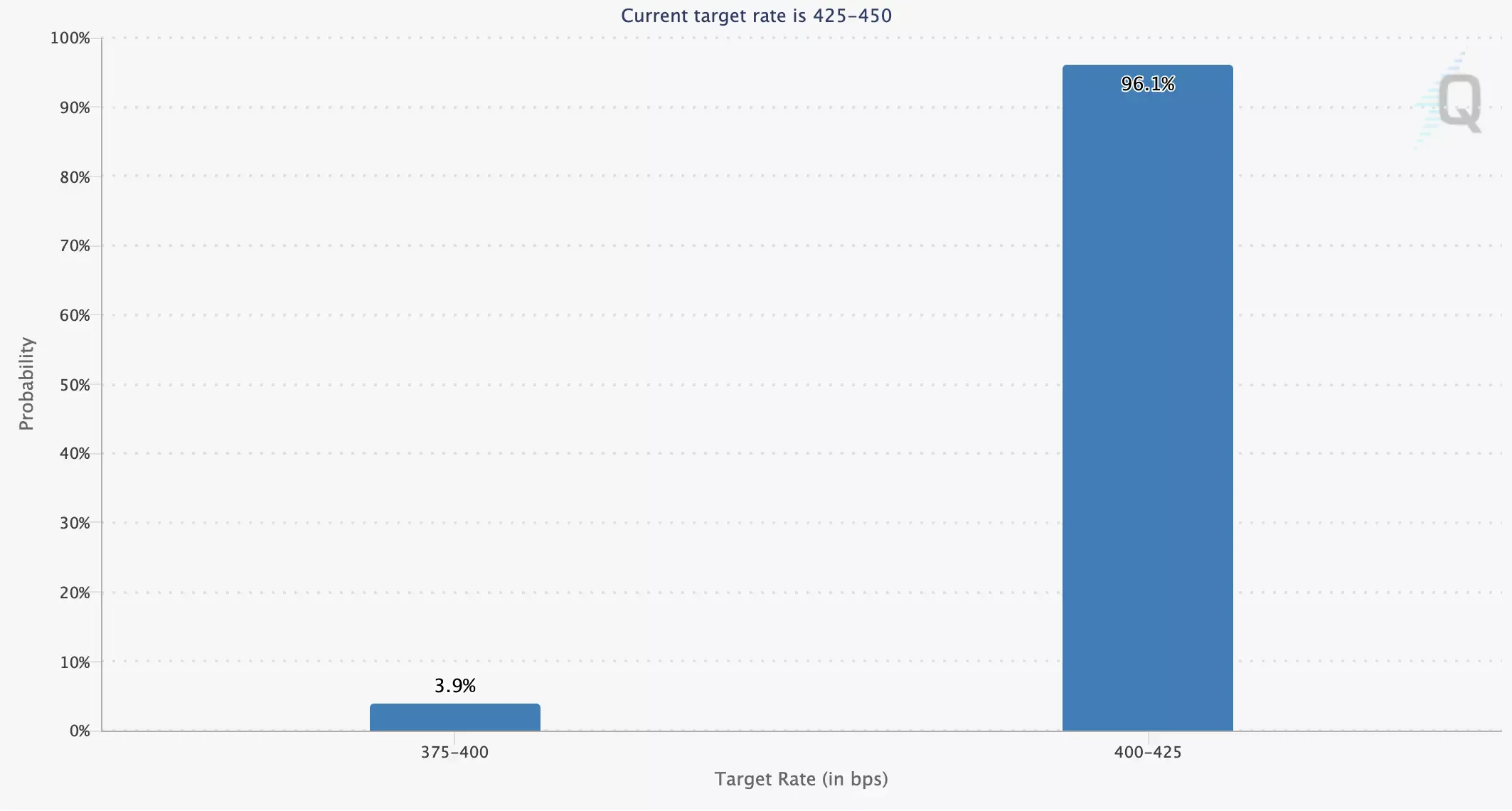

At the moment, according to the Chicago Mercantile Exchange (CME Group) FedWatch Tool, 96.1% of analysts forecast a 25 basis point rate cut to 4.25%.

It is also expected that Fed Chair Jerome Powell will point to the possibility of further monetary policy easing by the end of this year, especially after the release of weak labor market data. In addition, officials will present updated macroeconomic forecasts. The European Central Bank (ECB), meanwhile, has almost completed its cycle of lowering borrowing costs, although current investor expectations still allow for the possibility of another 25 basis point cut before the end of 2025. More concern in the EU is caused by the state of the economy and the growing political uncertainty due to the crisis in France and rapidly rising defense spending: the country recently saw another change of government. The new Prime Minister, appointed by Emmanuel Macron, is Defense Minister Sébastien Lecornu. Observers note that Lecornu takes office with extremely low ratings. Only 16.0% of respondents approve of his candidacy, while 40.0% strongly oppose it. The new French head of government faces a difficult task — to reach a budget compromise for 2026 with opposition parties, something his predecessor failed to achieve. Today at 11:00 (GMT+2) the market focus will be on July industrial production data in the eurozone: forecasts suggest a significant rise in the annual figure from 0.2% to 1.7% and in the monthly figure from –1.3% to 0.4%. At the same time, the overall Economic Sentiment Index from the ZEW Institute in September is likely to drop from 25.1 points to 20.3 points, which could pose a serious obstacle to the euro’s upward trend.

GBP/USD

The British pound is gaining value in the GBP/USD pair during the Asian session, consolidating above 1.3600 and updating local highs from July 8 after the release of national labor market statistics. In July, employment rose by 232.0K, only 7.0K fewer than in the previous month, while jobless claims in August increased by 17.4K after –33.3K, compared with a forecast of 20.3K. Average hourly earnings excluding bonuses slowed from 5.0% to 4.8%, and the unemployment rate stabilized around 4.7%. Traders are also awaiting the outcome of the two-day Fed meeting, which will end on Wednesday at 20:00 (GMT+2): markets are confident the regulator will start a new easing cycle by cutting rates by the standard 25 basis points. Jerome Powell will also publish updated macroeconomic forecasts, providing insight into further easing prospects through the end of 2025. The Bank of England will meet on September 18 at 13:00 (GMT+2): unlike the Fed, analysts expect policy to remain unchanged, giving officials more time to fully assess the situation. Today at 14:30 (GMT+2), US retail sales data for August will be released, followed at 15:15 (GMT+2) by industrial production data. Monthly retail sales are expected to slow from 0.5% to 0.3%, while the annual rate should remain at 3.9%. Excluding autos, sales could rise from 0.3% to 0.4%. Industrial production is likely to contract further by 0.1%.

AUD/USD

The Australian dollar is strengthening in the AUD/USD pair during the Asian session, extending a strong bullish trend in both short-term and ultra-short-term outlooks. Traders are reluctant to open new positions ahead of the Fed’s two-day meeting results and updated forecasts, which will help assess Jerome Powell’s readiness for further policy adjustments this year. Meanwhile, weaker data from China is limiting the aussie’s growth: August industrial production slowed from 5.7% to 5.2% against expectations of 5.8%, and retail sales fell from 3.7% to 3.4% versus forecasts of 3.8%. On Thursday at 03:30 (GMT+2), Australia will release its August labor market report: experts expect seasonally adjusted employment to rise by 21.2K after a 24.5K increase in the previous month, with the unemployment rate steady at 4.2%. At its August meeting, the Reserve Bank of Australia (RBA) cut rates by 25 basis points to 3.6%, the lowest since April. Officials also expressed hope that the national economy will continue to recover despite global uncertainty.

USD/JPY

The US dollar is losing ground in the USD/JPY pair, testing the 147.00 mark for a downward breakout as investors close part of their long positions ahead of the Fed’s two-day meeting, where a 25 basis point cut is expected. This probability rose sharply after disappointing labor market data: in August, only 22.0K new non-farm jobs were created, and revised figures for the past 12 months to early March showed 911.0K fewer jobs than previously estimated, pointing to greater sector weakness. On Wednesday at 01:50 (GMT+2), Japan will release August trade data: export decline is expected to continue but slow from –2.6% to –1.9%, partly due to high US import tariffs. Outgoing Prime Minister Shigeru Ishiba, however, managed to reach a trade deal with Washington. Imports are likely to contract by 4.2% after –7.5%, which could widen the trade deficit from –117.5 billion yen to –513.6 billion yen.

XAU/USD

The XAU/USD pair is little changed in the morning session, holding near the record high of 3685.00. Investors are refraining from opening new positions ahead of tomorrow’s Fed decision at 20:00 (GMT+2), which could bring a 25 basis point rate cut. Markets are also awaiting updated policy forecasts: current estimates suggest borrowing costs could fall to 3.60% in one year, 3.40% in two years, and 3.10% in three years. A more dovish stance would put pressure on the US dollar, though for now the evidence is limited. Jerome Powell remains concerned about inflation risks amid global uncertainty and President Donald Trump’s tariff policy. Today at 14:30 (GMT+2), August retail sales data will be released, with forecasts pointing to a slowdown from 0.5% to 0.3%. Excluding autos, sales could accelerate from 0.3% to 0.4%. At 15:15 (GMT+2), industrial production data will follow, with experts expecting the figure to remain at –0.1%.