Tomorrow at 08:00 (GMT+2), Germany will release September inflation data, which could clarify prospects for another European Central Bank (ECB) rate cut. Forecasts suggest no change from the previous 0.2% month-over-month and 2.4% year-over-year. At 11:00 (GMT+2), the ZEW Economic Sentiment Index for October will follow — analysts expect the German reading to rise from 37.3 to 39.5, and the eurozone figure from 26.1 to 30.2. Meanwhile, wholesale prices in Germany rose by 0.2% in September after a –0.6% drop in August, accelerating from 0.7% to 1.2% year-on-year. Political tensions in France also weigh on sentiment: on October 10, President Emmanuel Macron reappointed Sébastien Lecornu as Prime Minister, only hours after his resignation, amid a struggle to secure parliamentary cooperation for the 2026 budget. Opposition leader Marine Le Pen announced plans to submit a motion of no confidence, likely supported by left-wing parties, which could further complicate the government’s work. U.S. markets are closed today for Columbus Day, though investors continue to monitor the ongoing government shutdown after the Trump administration confirmed the dismissal of more than 4,000 federal employees — a move strongly opposed by labor unions.

GBP/USD

The pound is advancing against the U.S. dollar, extending Friday’s upward move after rebounding from August lows, with the pair testing the 1.3350 level. In the U.S., Democrats and Republicans have yet to agree on a short-term funding bill to prevent a prolonged shutdown, while broader budget negotiations remain stalled. The White House began large-scale layoffs of federal workers last week, some of whom have already been reinstated, adding further uncertainty. Meanwhile, the University of Michigan’s consumer sentiment index slipped marginally in October to 55.0 from 55.1, while inflation expectations eased slightly — one-year outlook fell from 4.7% to 4.6%, and the five-year view held at 3.7%. In the U.K., August GDP and industrial production data are due Thursday at 08:00 (GMT+2), with growth expected at +0.2% after July’s flat reading, and industrial output seen rising 0.2% after –0.9%.

NZD/USD

The New Zealand dollar is trading sideways near 0.5740 amid mixed sentiment and steady macro data. The Business NZ Services Index rose from 47.6 to 48.3 in September, while tourist arrivals increased from 6.6% to 7.5% in August. Chinese trade data also supported the kiwi, showing stronger export and import growth that eased concerns about U.S. tariffs. Over the weekend, U.S. President Donald Trump reiterated plans to impose 100% tariffs on Chinese imports, in addition to existing 50% duties on steel, aluminum, and copper, after Beijing restricted access to rare earth metals — which accounted for about 70% of global production in 2024. China’s September exports rose 8.3% vs. 4.4% previously (forecast 6.0%), and imports jumped 7.4% vs. 1.3% (forecast 1.5%), bringing the trade surplus down to $90.45B from $102.33B. The NZD remains under pressure after the Reserve Bank of New Zealand cut its policy rate by 50 bps to 2.50%, signaling readiness for further easing to stabilize inflation around 2%.

USD/JPY

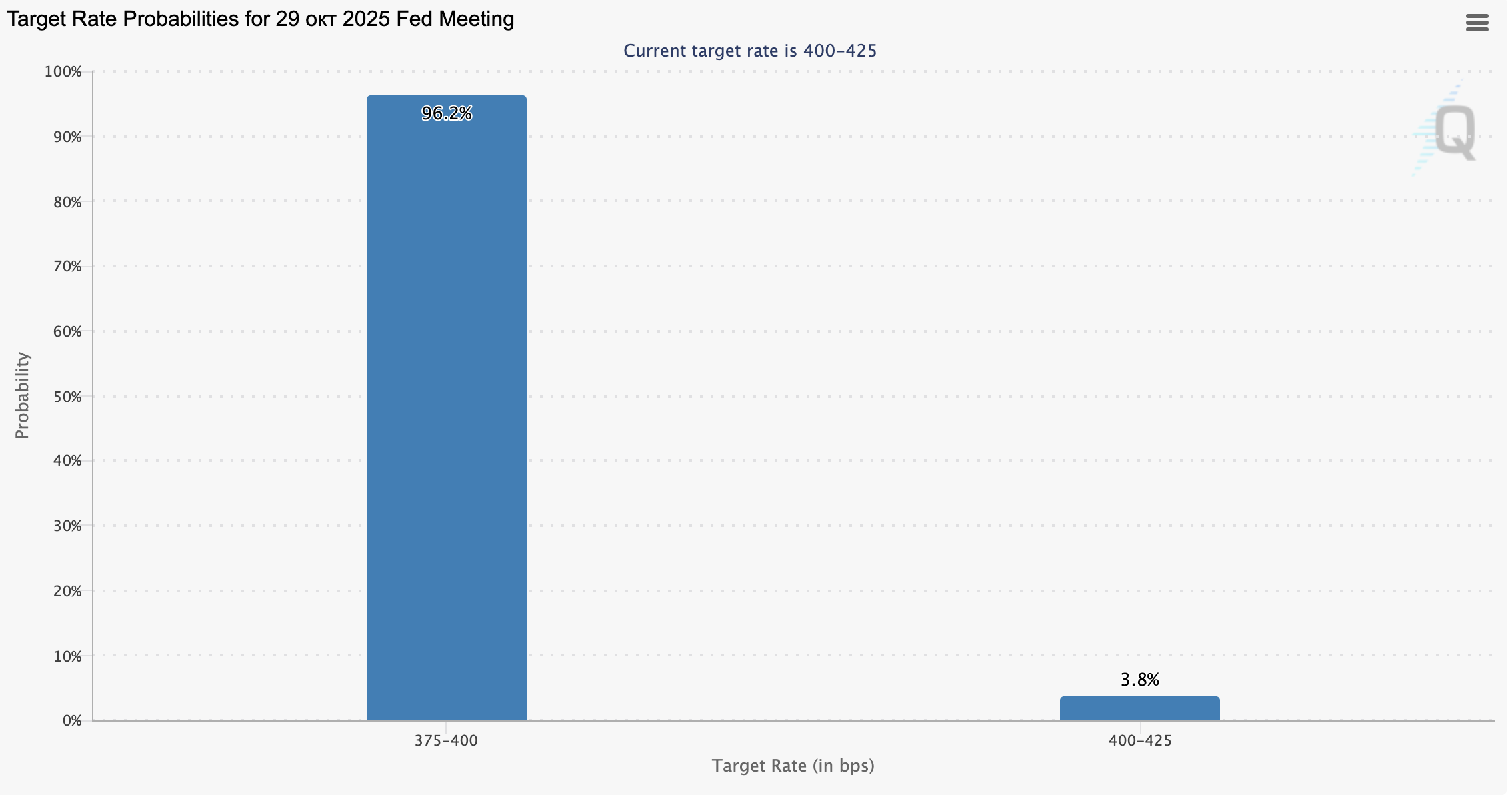

The U.S. dollar shows mixed dynamics against the yen, holding near 151.75 after falling sharply last Friday. Monday’s session opened with a modest upward gap, though the dollar struggles to recover amid thin trading caused by U.S. holidays and ongoing data disruptions due to the government shutdown. Labor market statistics remain delayed, but CME FedWatch Tool data now suggest a 95%+ probability of a Federal Reserve rate cut at the October meeting.

Meanwhile, Japan’s political developments are in focus after Sanae Takaichi won the leadership election of the ruling Liberal Democratic Party (LDP). The parliamentary vote for the new prime minister is scheduled for October 15 but may face delays after the long-standing coalition between the LDP and the Komeito Party collapsed — the first such split in 26 years. On Wednesday at 06:30 (GMT+2), Japan will release August industrial production data, expected to remain unchanged at –1.2% month-on-month.

XAU/USD

Gold prices continue to rise, reaching new record highs as XAU/USD tests the $4,070 level. The U.S. dollar remains under pressure amid the ongoing government shutdown and rising global political risks. The lack of progress in U.S. budget negotiations and renewed political turmoil in France — where President Macron reappointed Sébastien Lecornu as prime minister — have further fueled demand for safe-haven assets. The overall risk-averse sentiment supports gold’s uptrend, with investors awaiting clarity on U.S. fiscal policy and central bank actions in the coming weeks.