Earlier today, business activity data from Germany were released. The manufacturing PMI compiled by S&P Global and Hamburg Commercial Bank (HCOB) declined from 48.2 to 47.7, below the forecast of 48.5. The services PMI also eased from 53.1 to 52.6, compared with expectations of 52.8. At the same time, markets remain concerned about the ongoing crisis in Germany’s automotive sector, which is struggling to compete with Chinese manufacturers amid high energy costs and elevated U.S. import tariffs.

Across the euro area as a whole, PMI data showed manufacturing activity slipping from 49.6 to 49.2 versus preliminary estimates of 49.9. The services index fell from 53.6 to 52.6, missing expectations of 53.9.

Later today at 6:00 a.m. ET, traders will focus on December sentiment data from the ZEW Institute. The eurozone expectations index is projected to rise from 25.0 to 26.3, while Germany’s index is expected to remain unchanged at 38.5. In the U.S., the delayed November labor market report will be released at 8:30 a.m. ET. The report was not published last week and therefore did not factor into the Federal Reserve’s latest rate decision.

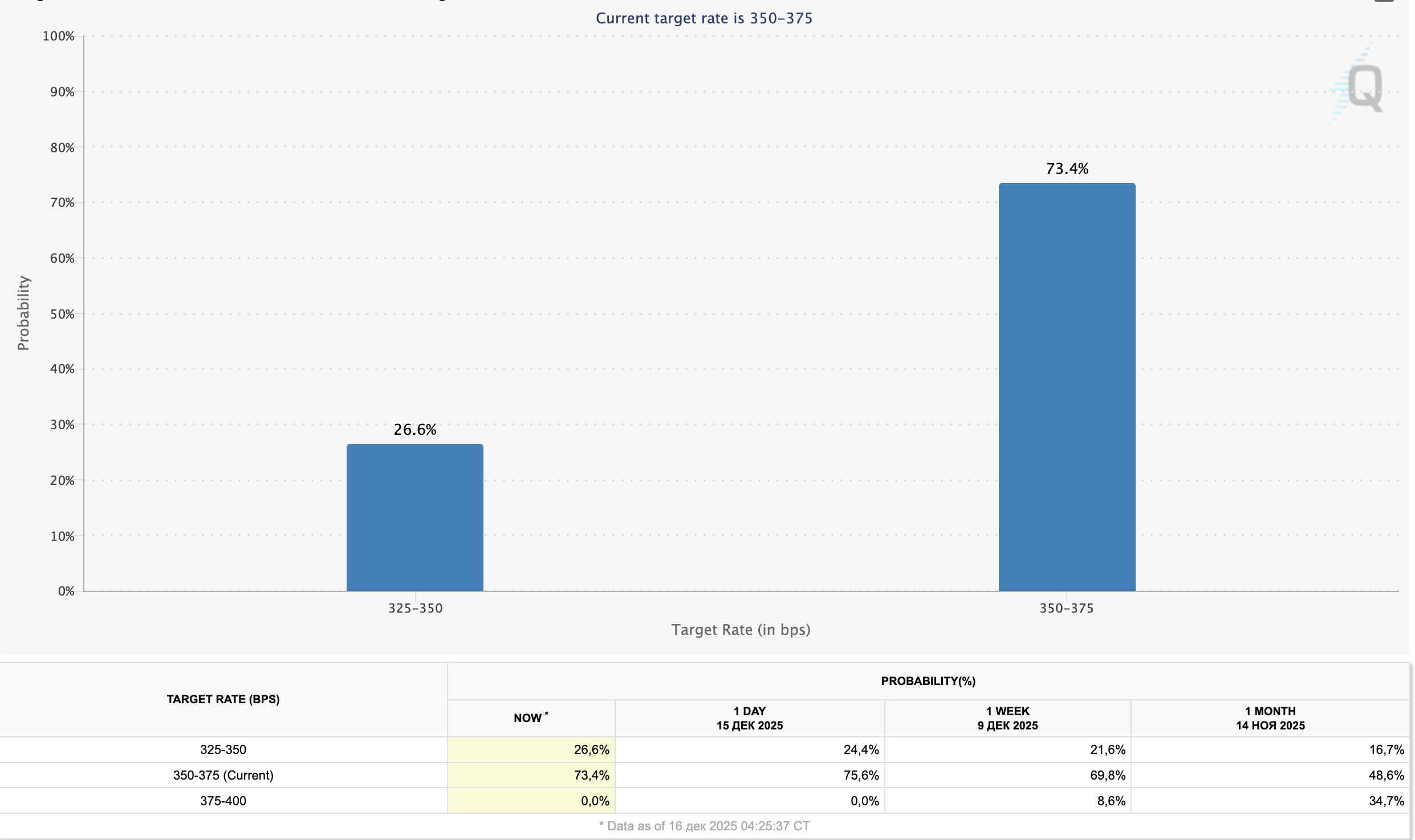

As a reminder, the Fed cut its policy rate by 25 basis points to 3.75% while leaving its forward guidance unchanged, with officials still projecting only one additional rate cut in 2026.

Meanwhile, expectations for inflation and economic growth have been revised higher, reinforcing speculation about further monetary easing. It is also worth noting that the leadership of the Federal Reserve is set to change in 2026, which currently represents a key source of uncertainty when forecasting the future path of interest rates.

GBP/USD

The British pound is weakening against the U.S. dollar, extending a mild corrective move that began late last week after the pair retreated from its October 20 highs. GBP/USD is testing the 1.3360 level to the downside, though sellers remain cautious as investors digest fresh economic data ahead of the Bank of England’s policy decision on December 18.

Markets are currently pricing in a 25 basis point rate cut to 3.75%. October wage growth including bonuses slowed from 4.9% to 4.7%, above forecasts of 4.4%, while wage growth excluding bonuses eased from 4.7% to 4.6% versus expectations of 4.5%. The unemployment rate edged up from 5.0% to 5.1%, and employment losses moderated to –17,000 after a –22,000 decline in September.

Weak labor market data may encourage the BoE to ease policy further, even though inflation has yet to return to its 2.0% target. November CPI data will be released on Wednesday at 3:00 a.m. ET, with core inflation expected at 3.4% and headline CPI projected to slow to 0.0% month over month. In the U.S., comparable CPI figures are due Thursday at 8:30 a.m. ET, with core inflation expected to remain unchanged at 3.0%.

NZD/USD

The New Zealand dollar is under pressure against the U.S. dollar, extending its corrective decline after pulling back from October 7 highs. NZD/USD is testing the 0.5780 level as investors remain sidelined ahead of the U.S. November labor report due at 8:30 a.m. ET.

October U.S. employment data were never released, while November figures are arriving later than usual, preventing the Fed from reviewing a complete dataset before last week’s meeting. Nonetheless, the central bank cut rates by 25 basis points to 3.75% and upgraded its inflation and growth outlook, while keeping its longer-term rate projections unchanged amid uncertainty and the upcoming leadership transition in 2026.

Kevin Hassett, a senior White House economic adviser, is among the potential candidates to succeed the current Fed chair and is widely viewed as favoring a more accommodative monetary stance.

Preliminary expectations for the November labor report point to little improvement: unemployment is forecast to remain at 4.4%, payrolls are expected to rise by 55,000, and average hourly earnings are projected at 0.2% month over month and 3.8% year over year.

Additional pressure on the New Zealand dollar came from weak data out of China. November industrial production growth slowed to 4.8% from 4.9%, missing forecasts of 5.0 and well below September’s 6.5%. Retail sales growth fell sharply from 2.9% to 1.3%, highlighting continued weakness in domestic demand. Markets also reacted to a decline in New Zealand’s services PMI from Business NZ, which dropped from 48.4 to 46.9.

USD/JPY

The U.S. dollar is weakening against the Japanese yen, with USD/JPY testing the 154.80 level to the downside and posting fresh local lows since December 5. The greenback remains under pressure ahead of the U.S. labor market report due at 8:30 a.m. ET.

Analysts hold a cautious outlook, noting that widespread layoffs linked to the government shutdown—many of which were later reversed—likely weighed on payroll growth. Later today at 9:45 a.m. ET, S&P Global will release December PMI data for both manufacturing and services. October retail sales data are also due at 8:30 a.m. ET, with headline sales expected to rise 0.2% month over month.

In Japan, investors are reviewing December PMI data from Jibun Bank. Manufacturing activity improved from 48.7 to 49.7, beating expectations, while services activity slipped from 53.2 to 52.5. The Tankan index for large manufacturers rose from 14 to 15, while the services index remained at 34, below forecasts.

Market participants are closely watching incoming data ahead of the Bank of Japan’s policy meeting scheduled for Friday. A 25 basis point rate hike to 0.75% is widely expected, though officials may face resistance from the government.

XAU/USD

Gold prices are retreating, with XAU/USD forming a corrective move and testing the 2,280.00 level to the downside. Trading activity remains muted ahead of the U.S. November labor market report at 8:30 a.m. ET.

Although October labor data were never released and November figures arrived late, the Fed still proceeded with a 25 basis point rate cut to 3.75% and upgraded its near-term outlook for inflation and growth. Longer-term rate projections remain unchanged amid uncertainty and the upcoming leadership change in 2026.

Weak labor market momentum could add pressure on policymakers to ease further in 2026. While the Fed currently projects only one additional rate cut, markets are pricing in two. No policy changes are expected at the January meeting. Meanwhile, the Bank of England meets on Thursday, with investors anticipating continued dovish guidance.

Lower interest rates tend to support gold, a non-yielding safe-haven asset.