Today’s September inflation figures from Italy are unlikely to shift market sentiment: the annual CPI held at 1.6%, while the monthly reading fell by 0.2%, as expected. Meanwhile, the European Central Bank (ECB) is not expected to move toward further aggressive easing, though another small rate cut before year-end remains possible.

Investor concern is focused more on political developments in parts of Europe, especially France. President Emmanuel Macron reappointed Sébastien Lecornu as prime minister after his resignation, and Lecornu has now proposed pausing the pension reform championed by Macron to secure support from the left in parliament. This has helped centrists win backing from the socialists, which could strengthen Lecornu’s position and stave off further no-confidence votes that still remain a risk.

Right-wing parties continue to call for the dissolution of parliament and urge Macron himself to resign. Some pressure on the single currency also stems from eurozone data showing that industrial production slowed from 1.8% to 1.1% y/y in August, while the seasonally adjusted monthly figure dropped from 0.3% to –1.2% versus –1.6% expected. At the same time, the U.S. dollar remains under pressure amid rising uncertainty from the government shutdown, now in its third week. The Senate recently rejected—for the ninth time—a stopgap funding bill due to ongoing disagreements, raising the risk of further federal layoffs and intensifying tensions.

GBP/USD

The pound is firmer against the U.S. dollar in GBP/USD, holding near the October 7 local highs as FX traders focus on UK data. As expected, GDP rose 0.1% m/m in August after –0.1% previously; industrial production increased 0.4% m/m after –0.4%, and fell –0.7% y/y after –0.1%, while the services activity index printed at 0.4%.

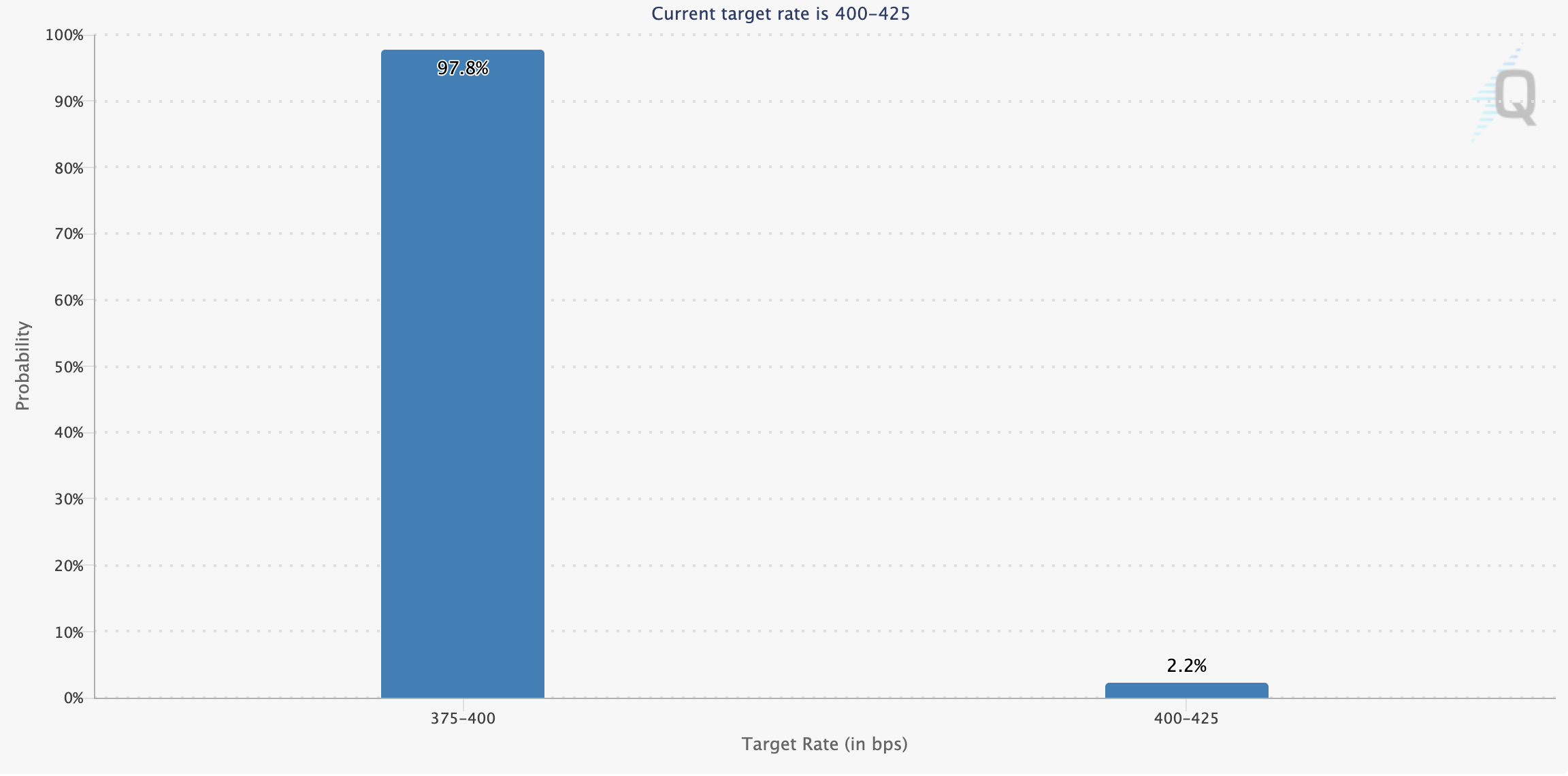

In the U.S., the ongoing shutdown continues to weigh on growth prospects. This week the Senate again rejected a temporary federal funding bill. Many analysts still believe passage is a matter of time, but for now uncertainty persists. Markets await the October 29 FOMC meeting, with consensus pointing to another 25 bp rate cut. More forceful action and dovish meeting notes are also possible given the limited flow of weak data lately. Traders are also monitoring escalating U.S.–China trade tensions, which could have negative global spillovers. UK investors are specifically concerned about EU steel import tariffs, as Britain remains a key supplier; higher duties could hurt the domestic steel industry’s competitiveness versus cheaper Chinese products.

NZD/USD

The New Zealand dollar is higher in NZD/USD, rebounding from last week’s drop as the pair tests 0.5745 for an upside break amid a lack of fresh catalysts. New Zealand’s food price index for September came in at 0.3%, pointing to inflation pressures holding roughly steady and unlikely to alter the Reserve Bank of New Zealand’s (RBNZ) near-term rate path. On October 8, the RBNZ cut rates by 50 bps versus 25 bps expected.

Officials also signaled they could ease further if the outlook warrants it: inflation is expected to hover near the top of the 1.0–3.0% target band in the near term, then ease toward the 2.0% midpoint in the first half of 2026. The RBNZ flagged political and economic uncertainty as a drag on business activity. Policy is also influenced by the aggressive tariff stance of U.S. President Donald Trump, particularly the flare-up in U.S.–China trade tensions. Trump announced additional 100% tariffs on Chinese goods starting November 1 in response to Beijing’s restrictions on rare earth exports. Reciprocal “port duties” took effect recently as well, potentially adding costs to global trade. Traders also noted China’s inflation data: the annual CPI for September fell 0.3% after –0.4% previously (vs –0.1% expected), while the monthly reading edged up 0.1% after flat, missing the 0.2% consensus.

USD/JPY

The U.S. dollar is flat in USD/JPY, consolidating near 151.00. Activity is subdued as the U.S. shutdown continues to limit the macro data flow. The Senate has now rejected—for the ninth time—a stopgap funding bill amid stalled negotiations between Democrats and Republicans. Markets look to the October 29 FOMC meeting, with an additional 25 bp cut widely expected. Investors are likewise tracking the U.S.–China trade backdrop.

Japan’s data today disappointed: core machinery orders slowed sharply to 1.6% y/y in August from 4.9% (4.8% expected) and fell 0.9% m/m after –4.6% (0.5% expected). The services activity index slipped 0.4% in August after +0.2% (–0.2% expected). Investors are also

XAU/USD

Gold (XAU/USD) is advancing, printing fresh record highs and testing 4222.60 on the upside as the U.S. dollar stays pressured by the prolonged government shutdown. Senators again failed to pass a stopgap bill to fund the federal government through November, with the weekly hit to the economy estimated at about $15.0 billion, exacerbating concerns around the trajectory of public debt. Reports suggest certain U.S. military activities off Venezuela’s coast have also been paused amid uncertainty over payroll disbursements to service members.

Demand for gold has also risen on intensifying U.S.–China trade tensions. President Donald Trump announced additional 100% tariffs on Chinese imports from November 1, citing Beijing’s export restrictions on rare earth elements. Around 70% of these minerals—vital for high-tech manufacturing—are supplied by China, amplifying worries about supply chains and costs.

Finally, the dollar is weighed down by growing expectations for a further 25 bp Fed rate cut in October, with at least one more easing move priced in before year-end. Yesterday’s data offered some support to the greenback: the New York Fed’s Empire State manufacturing index rose to 10.7 in October from –8.7, beating the –1.8 forecast.