EUR/USD. The euro is trading sideways near 1.1560 as market activity remains subdued while traders await confirmation of the U.S. government reopening.

Yesterday, it was reported that the U.S. Senate had successfully reached an agreement on a new temporary funding bill for the federal government through the end of January 2026. According to available information, Democratic and Republican lawmakers agreed to hold an additional vote in December regarding healthcare subsidies under the Affordable Care Act (ACA). The bill now moves to the House of Representatives and will then be signed by President Donald Trump, officially ending the shutdown that has lasted over 40 days.

At 12:00 (GMT+2), traders await Germany’s ZEW Economic Sentiment Index for November. Forecasts suggest a modest rise from 39.3 to 40.0 points, reflecting gradual improvement in business conditions driven by government support for industrial recovery and growth. The current situation index is expected to rise from –80.0 to –77.5 points, while the Eurozone-wide index could increase from 22.7 to 23.5 points. Meanwhile, the Sentix Investor Confidence Index for November fell from –5.4 to –7.4 points, contrary to expectations for –3.9. On Wednesday, at 09:00 (GMT+2), Germany will release October inflation data — analysts expect the monthly CPI at 0.3% and the annual rate at 2.3%. The European Central Bank’s policy outlook, however, appears largely predetermined.

GBP/USD

The British pound continues to strengthen against the U.S. dollar, extending last week’s bullish momentum and testing the 1.3200 level near early-month highs. The pound remains supported by the latest Bank of England meeting, where policymakers voted narrowly (5–4) to keep the interest rate unchanged at 4.00%. The close vote highlights the growing split within the Monetary Policy Committee, as several members pushed for an additional 25 basis point rate cut.

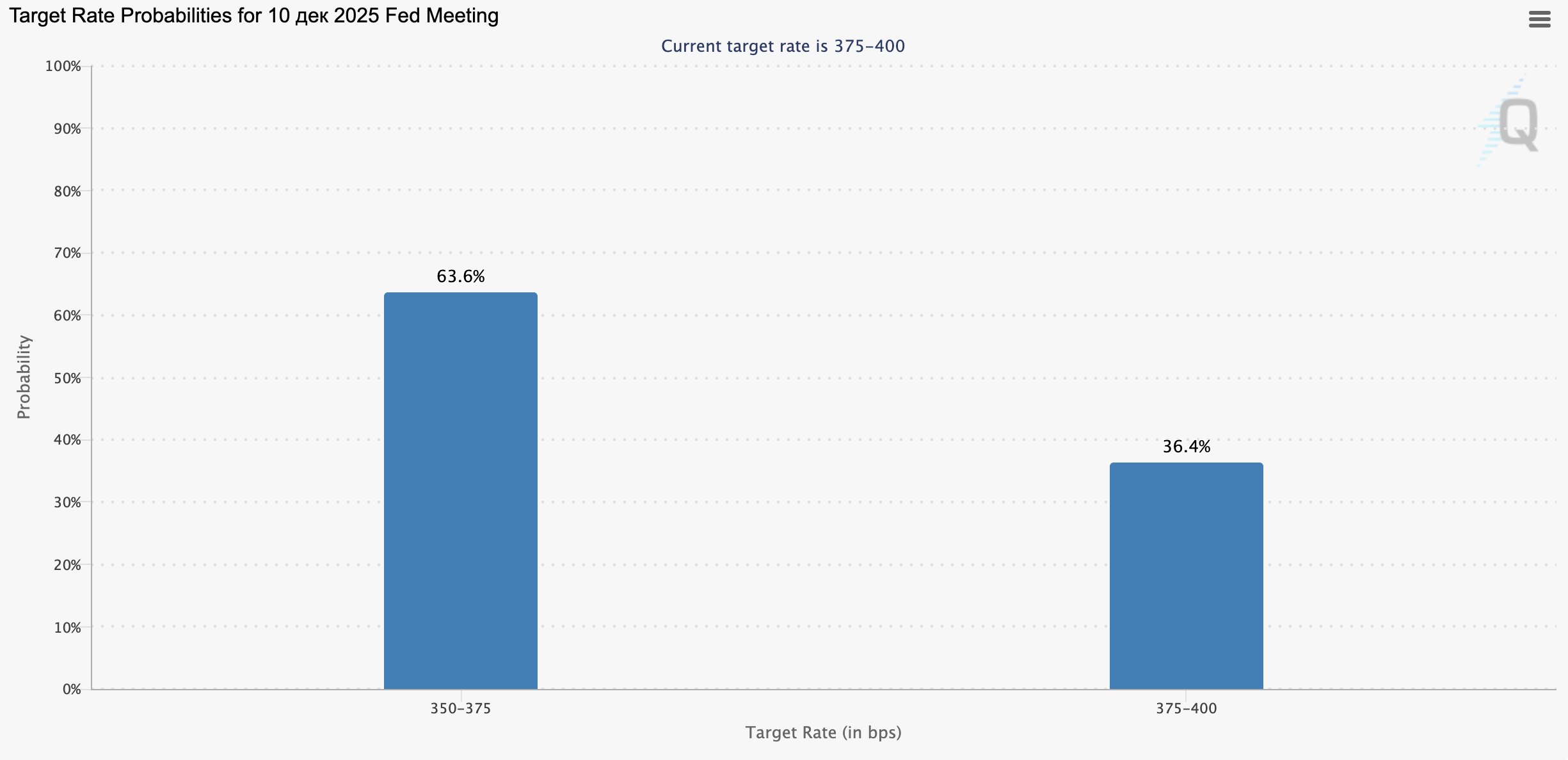

Impact of Fed Expectations on the Forex Market

The chart shows market expectations for changes in the Fed's key rate by the December 10, 2025 meeting (CME FedWatch Tool).

- 25 basis point rate cut to the 3.50–3.75% range — 63.6% probability.

- Rate unchanged at 3.75–4.00% — 36.4% probability.

Interpretation: Most investors still expect monetary policy easing by the end of 2025, which puts pressure on the U.S. dollar while supporting gold, stock indices, and cryptocurrencies.

However, hopes for a December rate cut are fading. Fed Chair Jerome Powell recently warned that maintaining a dovish tone is “risky,” noting that key labor market data has not been published for several weeks due to the shutdown. Still, the Senate’s approval of the temporary funding bill earlier this week could soon allow the resumption of federal operations and delayed data releases. Meanwhile, U.K. investors are watching labor market figures: October jobless claims rose by 29,000 (vs. 20,300 expected), pushing the unemployment rate from 4.8% to 5.0%. Wage growth, including bonuses, slowed from 5.0% to 4.8%. On Thursday, at 09:00 (GMT+2), updated GDP data for Q3 will be released, with estimates suggesting a revision from 0.3% to 0.2% growth.

AUD/USD

The Australian dollar is losing ground near 0.6520, retreating from local highs seen on November 3. The U.S. dollar remains under pressure following news of bipartisan progress in resolving the shutdown, which could allow the federal government to resume work as soon as November 15. The Senate has already passed a temporary funding bill through January 2026. The end of the shutdown would also allow the release of key U.S. labor data — crucial for the Fed’s next policy decisions.

In October, the Fed cut its key rate by 25 basis points, though Chair Jerome Powell warned against premature expectations of continued easing. Today’s Australian data had little market impact: the NAB Business Confidence Index fell from 7 to 6 points in October, while the Business Conditions Index rose from 8 to 9 points. The Westpac Consumer Confidence Index increased by 12.8% in November after a –3.5% drop the previous month. On Thursday, at 02:30 (GMT+2), Australia will publish October employment data: forecasts suggest job growth of 15,000 after 14,900 in September, while unemployment is expected to ease from 4.5% to 4.4%.

USD/JPY

The USD/JPY pair shows modest gains, consolidating above 154.00 and nearing new record highs. The Japanese yen remains pressured by expectations that the Bank of Japan will maintain its ultra-loose policy under new Prime Minister Sanae Takaichi, a known advocate of accommodative monetary measures. The BoJ continues to monitor slowing inflation momentum.

Recent Japanese data was moderately positive: bank lending rose from 3.8% to 4.1% in October, while the current account surplus widened from ¥3.70 trillion to ¥4.48 trillion. The Eco Watchers Current Index climbed from 47.1 to 49.1, and the Leading Index rose from 48.5 to 53.1. Meanwhile, the U.S. dollar’s strength slightly weakened following optimism about the Senate’s funding deal, which could finally end the record 40-day shutdown.

XAU/USD

Gold (XAU/USD) extends its bullish momentum, testing the 4135.00 level for a breakout. Trading volumes remain low as U.S. markets are closed for Veterans Day. Investors are focused on the potential resolution of the U.S. shutdown, which has lasted 41 days. The Senate’s temporary funding agreement through January 2026 raises hopes of a near-term resolution.

At the same time, the dollar receives moderate support amid weakening expectations for a December rate cut. Fed Chair Powell has called further easing “risky,” citing missing labor data due to the shutdown. This cautious tone continues to limit gold’s upside potential in the short term.